Can pricing deter adolescents and young adults from starting to drink: An analysis of the effect of alcohol taxation on drinking initiation among Thai adolescents and young adults

- DOI

- 10.1016/j.jegh.2015.05.004How to use a DOI?

- Keywords

- Alcohol; Drinking initiation; Middle-income countries; Prevention; Taxation; Thailand

- Abstract

The objective of this study is to assess the relationship between alcohol taxation changes and drinking initiation among adolescents and young adults (collectively “youth”) in Thailand (a middle-income country). Using a survey panel, this study undertook an age-period-cohort analysis using four large-scale national cross-sectional surveys of alcohol consumption performed in Thailand in 2001, 2004, 2007 and 2011 (n = 87,176 Thai youth, 15–24 years of age) to test the hypothesis that changes in the inflation-adjusted alcohol taxation rates are associated with drinking initiation. Regression analyses were used to examine the association between inflation-adjusted taxation increases and the prevalence of lifetime drinkers. After adjusting for potential confounders, clear cohort and age effects were observed. Furthermore, a 10% increase of the inflation-adjusted taxation rate of the total alcohol market was significantly associated with a 4.3% reduction in the prevalence of lifetime drinking among Thai youth. In conclusion, tax rate changes in Thailand from 2001 to 2011 were associated with drinking initiation among youth. Accordingly, increases in taxation may prevent drinking initiation among youth in countries with a high prevalence of abstainers and may reduce the harms caused by alcohol.

- Copyright

- © 2015 Ministry of Health, Saudi Arabia. Published by Elsevier Ltd.

- Open Access

- This is an open access article under the CC BY-NC-ND license (http://creativecommons.org/licenses/by-nc-nd/4.0/).

1. Introduction

Alcohol consumption is one of the most important risk factors for the burden of disease (measured as Disability-Adjusted Life Years [DALYs] lost, which combines years of life lost due to premature mortality with years lived with disability) [1,2]. In 2012, alcohol consumption accounted for 5.9% of the total deaths globally and for 5.1% of the total DALYs lost globally [3]. The consumption of alcohol also creates large economic costs in both high-income countries (HICs) and in low- and middle-income countries (LMICs) [2].

The health, social and economic impacts of alcohol led the World Health Organization (WHO) in its recently adopted global strategy to emphasize the need for better alcohol control efforts in LMICs [4]. As part of this strategy, the WHO recommends excise taxation of alcohol as a key preventative measure [4], as systematic reviews and meta-analyses have found that increasing alcohol excise taxes is one of the most effective ways of reducing alcohol-related harms [5–8]. For example, in low-income countries, the tax elasticity for total alcohol consumption was found to be −0.64 in a meta-analysis [5,7,8], which is comparable to elasticity observed in meta-analyses which included results primarily from studies of HICs (−0.77) [5,7,8].

1.1. Alcohol consumption and harms in Thailand

The harms caused by alcohol present a large problem in Thailand (a middle-income country). For instance, there were more than 18 car-crash deaths per 100,000 people per year from 2006 to 2010, of which 40–60% were attributable to drunk driving [9], which is higher than what would be expected given Thailand’s alcohol consumption profile [3]. Moreover, over the same time period, there was a fourfold increase in alcohol-related domestic violence, and 40% of crimes perpetrated by adolescents were related to alcohol [10]. These are typical results of alcohol drinking patterns in LMICs that are often more problematic compared with those in HICs [11], contributing to much greater relative harms associated with each liter of alcohol consumed per capita [12].

While the prevalence of lifetime abstention from alcohol is high in Thailand, especially among Thai adolescents (70% of male and 82% of female secondary school students [13]), the drinking habits of young Thai drinkers are problematic [13]. For example, 45% of Thai males aged 12–19 years engaged in very high-risk drinking in terms of intensity (>100 g of pure alcohol per drinking day), while very high-risk drinking was engaged in by 28%, 29% and 24% of Thai males aged 20–24, 25–44, and 45–65 years of age, respectively [14]. Another study found that 17.5% of male and 7.2% of female students in grade 11 at regular schools and in equivalent levels of vocational schools had at least one occasion of binge drinking in the 30 days prior to being interviewed [15]. Moreover, once Thai adolescents start to drink, they tend to become regular drinkers: two-thirds of male students and almost one-half of female students who have had at least one alcoholic drink in their lifetime have consumed alcohol within the past 30 days [13]. Because young lifetime abstainers are vulnerable to becoming drinkers, which can lead to frequent or problematic drinking causing alcohol-related harms in the long term [16]. Thailand, which has a high rate of drinking abstention among youth, has substantial current problems caused by alcohol consumption, as well as the risk of substantial problems in the future.

Similar to many other governments that increase alcohol excise taxation intermittently to either raise tax revenues or control alcohol consumption, the Thai government changed alcohol excise taxation in 2003, 2005, 2007, and 2009. Alcohol excise taxation and alcohol prices are associated with the reduction of alcohol consumption among youth (specifically binge drinking and overall consumption) and its related harms [5,6]; however, no research to date has examined the effects of excise taxation or price increases on drinking initiation rates among youth in LMICs (see Panel), where sizable portions of the population are lifetime abstainers [3]. National Thai surveys on alcohol consumption (that collected data on lifetime abstention among youth [15–24 years of age]) were performed in 2001, 2004, 2007, and 2011. These surveys represent an opportunity to measure the association between fluctuations in alcohol taxation rates and the prevalence of lifetime drinkers. Similar to the effect of excise taxation of cigarettes on the prevention of smoking initiation [17], it has been hypothesized that excise taxation of alcohol in LMICs can prevent harms in the long term by preventing drinking initiation; however, no study has empirically tested this hypothesis [16]. Thus, the aim of this study is to determine if changes in the inflation-adjusted alcohol excise taxation rates are associated with changes in the prevalence of lifetime drinkers among youth in Thailand.

Research in context.

Systematic review

We conducted a systematic review and meta-analysis of the effects of taxation on alcohol consumption, its related harms, and drinking initiation in LMIC using internationally standardized protocols [8]. Data were collected up to June 2011 by searching the peer-reviewed article databases MEDLINE, EMBASE, PsycINFO and EconLit, along with the WHO’s gray literature Database of Abstracts of Reviews of Effects, and by reference tracking. We identified, screened, checked against inclusion and exclusion criteria, and included eligible studies to perform both qualitative and quantitative analyses. We found ten studies that quantitatively examined the effects of taxation on alcohol consumption, and our meta-analysis showed that an increase in alcohol taxation resulted in a decrease in alcohol consumption. There was no published literature that examined the effects of taxation on alcohol-related harms and drinking initiation in LMIC.

Interpretation

Our study was the first to investigate the effects of alcohol taxation on drinking initiation in LMIC. Moreover, since this study used four large-scale nationally representative cross-sectional surveys performed in Thailand, with a combined sample size of 87,176 people, we were able to empirically test a potential relationship between alcohol taxation and drinking initiation. Our findings demonstrate that increases in alcohol taxation can prevent drinking initiation among youth (15–24 years of age); a 10% increase in the average tax rate of the total alcohol market was associated with a 4.3% reduction in the prevalence of lifetime drinking among youth. The effects of taxation contributed to a relatively stable prevalence of lifetime abstention in this age group in Thailand, even though a decrease in abstention was expected due to economic growth.

2. Materials and methods

2.1. Study design

Using a survey panel, this study undertook age-period-cohort analysis, and used survey data on the prevalence of lifetime drinking, as well as inflation-adjusted excise taxation data from 2001 to 2011.

2.1.1. Data sources

Drinking initiation data were obtained from four large-scale national cross-sectional surveys conducted by the National Statistics Office (NSO) of Thailand in 2001 (n = 31,849), 2004 (n = 8,629), 2007 (n = 25,493), and 2011 (n = 21,205) (“n” denotes the number of participants 15–24 years of age). The authors had access to all survey data collected due to the relationship between the Center for Alcohol Studies in Thailand (the first author’s primary affiliation) and the NSO. All surveys used a two-stage stratified probability sampling design. In the 2001, 2007, and 2011 surveys, Thailand was stratified into 76 provinces, and then further into urban and rural areas, while in the 2004 survey, Thailand was stratified into five regions (North, Northeast, Central, South, and Bangkok) and then into urban and rural areas. Within each stratum, the primary sampling unit was residential blocks for urban areas and villages for rural areas, and the secondary sampling unit was households. Every person 15 years of age and older in the household was interviewed by trained NSO field researchers using a standardized questionnaire. Response rates were 83%, 83%, 87%, and 85% for the 2001, 2004, 2007, and 2011 surveys, respectively. Details of the survey sampling are outlined in Table 1.

| Survey year | Total | ||||

|---|---|---|---|---|---|

| 2001 | 2004 | 2007 | 2011 | ||

| Study design | Cross-sectional survey | ||||

| Sampling scheme | Two-stage stratified random sampling with probabilities proportional to size: the primary sampling unit was a block or village; the secondary sampling unit was a household | ||||

| Samples were representative of | Provincial, regional, and national level | Regional, and national level | Provincial, regional, and national level | Provincial, regional, and national level | |

| Overall sample size (aged 15 years and over) | 168,141 | 51,330 | 168,285 | 142,235 | 529,991 |

| Sample size aged 15–24 years | 31,849 | 8,629 | 25,493 | 21,205 | 87,176 |

Details of survey sampling. Source: National Statistics Office of Thailand.

Drinking initiation, the dependent variable of interest, was measured using “lifetime drinking,” with respondents being classified as “lifetime drinkers” or “lifetime abstainers.” In the surveys examined, a person who answered “no” to the question: “Have you ever consumed at least one full alcoholic beverage?” was considered a “lifetime abstainer,” while a person who answered “yes” to this question was considered a “lifetime drinker.”

The independent variable of interest was the percentage change in inflation-adjusted taxation rates for the total alcohol market. Data on taxation rates and market share of all alcoholic beverages in 2003, 2005, 2007, and 2009 were obtained from the Thai Excise Department. The average taxation rate per liter of pure alcohol for the total alcohol market was calculated by summing all alcohol beverage category taxation rate changes which were weighted by each category’s market share (based on volume of pure alcohol) for that year. Taxation rates were adjusted for inflation (to the year 2001) by adjusting the tax per liter of alcohol to 2001 Thai baht using data from the World Bank [18]. Specific tax rates (based on alcohol volume) are constant by nature and ad valorem tax rates (based on price) in Thailand are also constant, since the latter are tied to beverage ex-factory prices (the price of an alcoholic beverage as purchased from the manufacturer); ex-factory prices are set during ad valorem taxation increases and are not updated between excise taxation changes. See Sornpaisarn et al. [16] for more detailed information on Thailand’s alcohol excise taxation system.

Table 2 outlines the percentage changes in actual excise taxation rates and in inflation-adjusted (using 2001 as the baseline year) excise taxation rates in 2003, 2005, 2007, and 2009 for eight beverage categories compared with the taxation rates in 2001. These taxation rate changes only impacted certain beverage categories (see Web Appendix 1). The total market inflation-adjusted taxation rates were calculated by a weighted sum of the individual beverage categories multiplied by their percentage market share. Average percentage changes of inflation-adjusted taxation rates of the total alcohol market were: 0.0% (baseline year), −13.6%, −0.2%, 1.7%, and 3.4% in the years 2001, 2003, 2005, 2007, and 2009, respectively.

| Types of alcoholic beverages | Actual taxation rate change (inflation-adjusted taxation rate change) and market share by year | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 2003 | 2005 | 2007 | 2009 | ||||||

| % increase | % market share | % increase* | % market share | % increase* | % market share | % increase* | % market share | % increase* | % market share | |

| White spirits | 0 | 50.2 | −30 (−32) | 41.5 | −30 (−36) | 37.5 | 10 (−7) | 36.0 | 20 (−3) | 31.4 |

| Mixed spirits | 0 | 6.0 | 0 (−2) | 1.4 | 0 (−9) | 1.4 | 17 (−1) | 7.7 | 25 (2) | 10.9 |

| Special blended spirits | 0 | 3.2 | 0 (−2) | 0.1 | 67 (51) | 0.7 | 67 (41) | 0.3 | 67 (35) | 0.3 |

| Whisky | ||||||||||

| Inexpensive | 0 | 9.5 | 0 (−2) | 23.3 | 67 (51) | 28.1 | 67 (41) | 18.8 | 67 (35) | 14.1 |

| Expensive | 0 | 1.0 | 25 (22) | 1.9 | 25 (13) | 2.3 | 25 (6) | 1.9 | 25 (1) | 1.4 |

| Brandy | 0 | 1.5 | 36 (32) | 1.3 | 100 (82) | 1.3 | 114 (81) | 1.7 | 144 (98) | 1.6 |

| Community fermented beverages | 0 | 0.1 | −30 (−32) | 0.1 | −30 (−36) | 0.01 | −30 (−41) | 0.003 | −30 (−43) | 0.01 |

| Beer | 0 | 27.0 | 0 (−2) | 29.3 | 0 (−9) | 28.1 | 0 (−15) | 33.1 | 16 (−6) | 39.6 |

| Wine | 0 | 1.6 | 0 (−2) | 1.1 | 0 (−9) | 0.6 | 0 (−15) | 0.6 | 0 (−19) | 0.7 |

| Tax rate changes of the total alcohol market** | 0 | −12 (−13.6) | 10 (−0.2) | 20 (1.7) | 28 (3.4) | |||||

Inflation-adjusted tax rate changes are presented in the parentheses.

Average tax changes of the total alcohol market each year were calculated by summing all category tax rate changes weighted by each category’s market share of pure alcohol for that same year. Data are calculated by the authors based on data from the Excise Department of Thailand.

Percentage changes in inflation-adjusted taxation rates of eight beverage categories compared to the taxation rates in 2001. Source: Excise Department of Thailand.

2.2. Statistical analysis

Regression analyses (taking into account the complex survey designs and the correlation between observations from the same survey) were used to examine the association between inflation-adjusted taxation rate changes and the prevalence of lifetime drinking among youth, with the period effect modeled via proxy variables. Regressions were performed by means of a general linear model-like regression with a quasi-Poisson distribution function and a log link function to measure the prevalence of lifetime drinking. The quasi-Poisson regression allows for the calculation of prevalence ratios when the dependent variable of the regression is coded either 0 or 1 and the data collected are from a cross-sectional survey [19]. Furthermore, for surveys where the main descriptive measure is prevalence, the prevalence ratio is more appropriate and more intuitive when compared with an odds ratio [20]. Previous studies in Thailand found that male gender, age groups of 20–24 and 25–44 years, not being married, living in Bangkok, and living in a rural area, were predictors of hazardous, harmful and dependent drinking [14]; the level of education attained predicted current drinking status and problematic drinking patterns [13]. Additionally, economic growth in LMICs has been found to be associated with per capita alcohol consumption [21]. Accordingly, the regression analyses were adjusted for age, birth cohort, and for several demographic variables (gender, age, marital status, education, and region of the country [North, East, South, Central, and Bangkok]).

More detailed analyses were also performed by sex and by age using the age categories of 15–17, 18–19, and 20–24 years. For sub-population comparisons, the conservative Bonferroni correction was used. R version 3.1.1 and the R statistical package survey [22] were used for data management and analysis.

2.3. Ethical considerations

Approval for this study by the Research Ethics Boards of the Centre for Addiction and Mental Health and the University of Toronto was waived, as this study only involved the analysis of secondary data.

2.4. Role of the funding sources

The funders of the study had no role in study design, data collection, data analysis, data interpretation, or writing of the report. Additionally, the funding sources had no role in approval of the final article. All authors had access to all data used in the study, and all authors approved the final version of the article.

3. Results

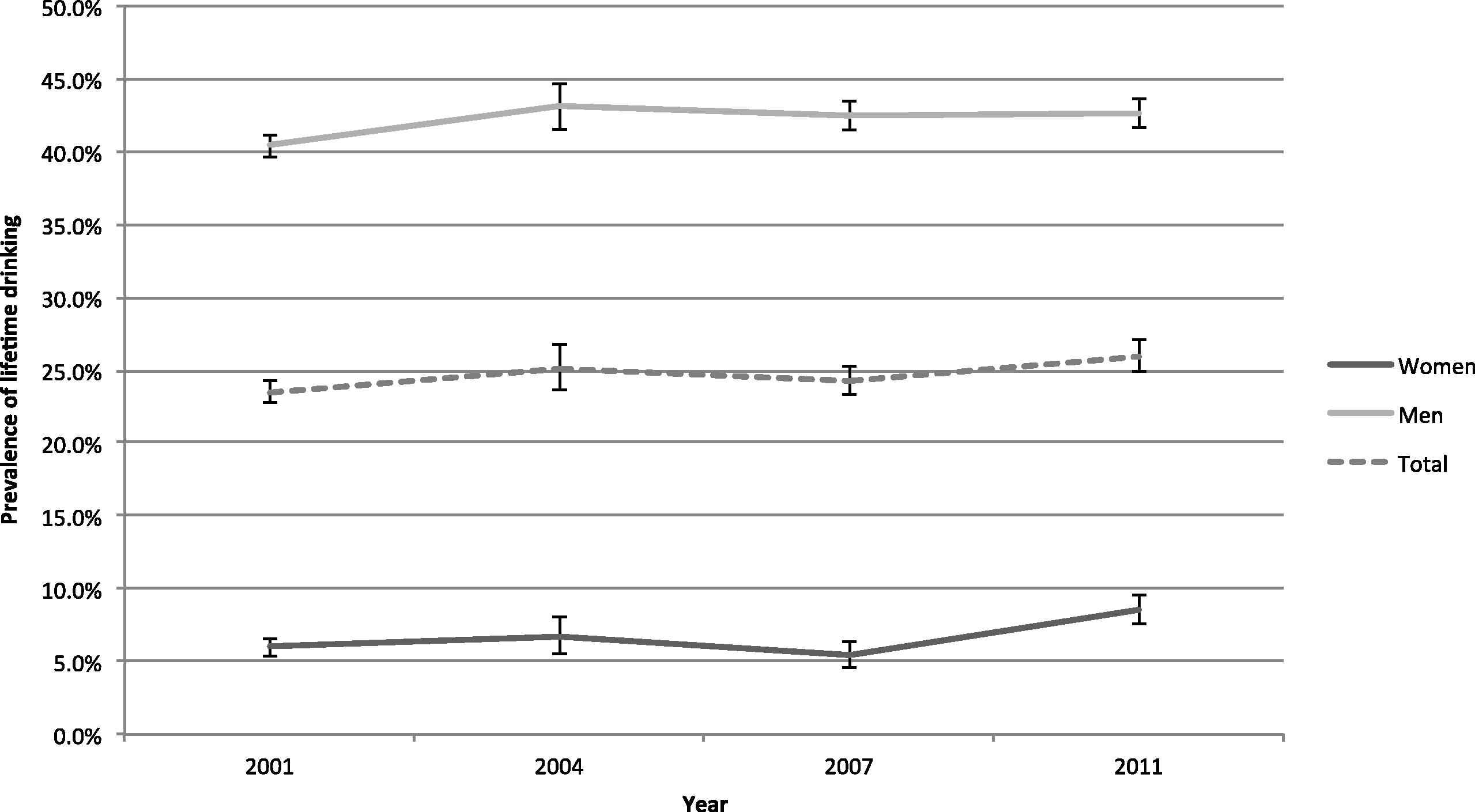

The characteristics of the survey samples from Thailand for 2001, 2004, 2007 and 2011 are outlined in the Web Appendix 2. The prevalence of lifetime drinking stratified by sex from 2001 to 2011 among Thai youth is outlined in Fig. 1. In 2001, the prevalence of lifetime drinking in Thailand in the age group under consideration was 23.5% (95% Confidence Interval [CI]: 22.7–24.2%), while in 2011 the prevalence of lifetime drinking was 26.0% (95% CI: 24.9–27.0%). The increase in lifetime drinking from 2001 to 2011 was significant for females (p < 0.001), but not for males (p = 0.077); however, after adjusting for age, the increase in the prevalence of lifetime drinkers was significant for both sexes (females p < 0.001; males p = 0.007). Therefore, a change in the age structure in Thailand may be responsible for the non-significant increase in lifetime drinking among males. Furthermore, the prevalence of lifetime drinking at all time points was much greater among Thai male youth than it was among Thai female youth.

Prevalence of lifetime drinking and 95% confidence intervals among Thai youth 15–24 years of age.

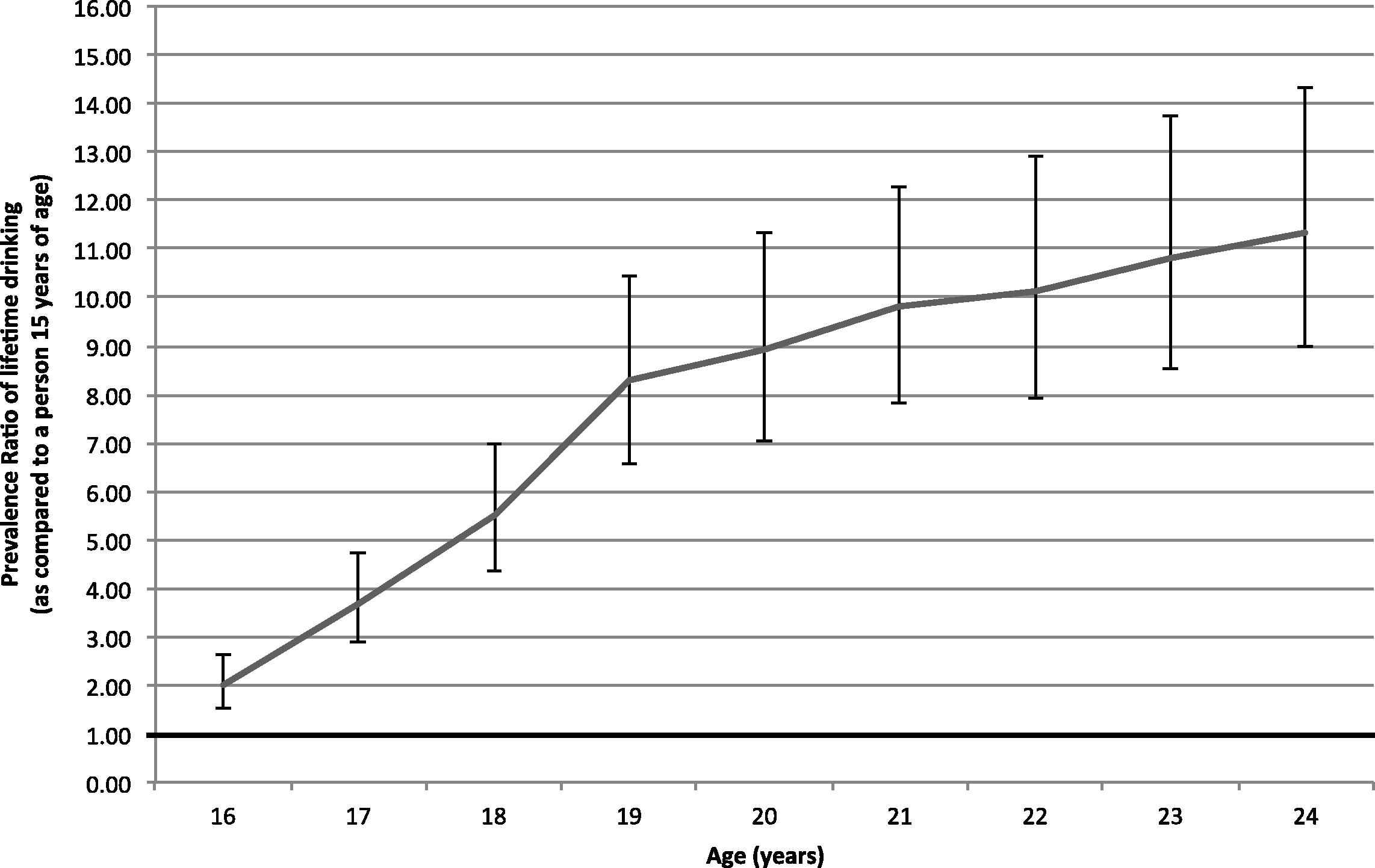

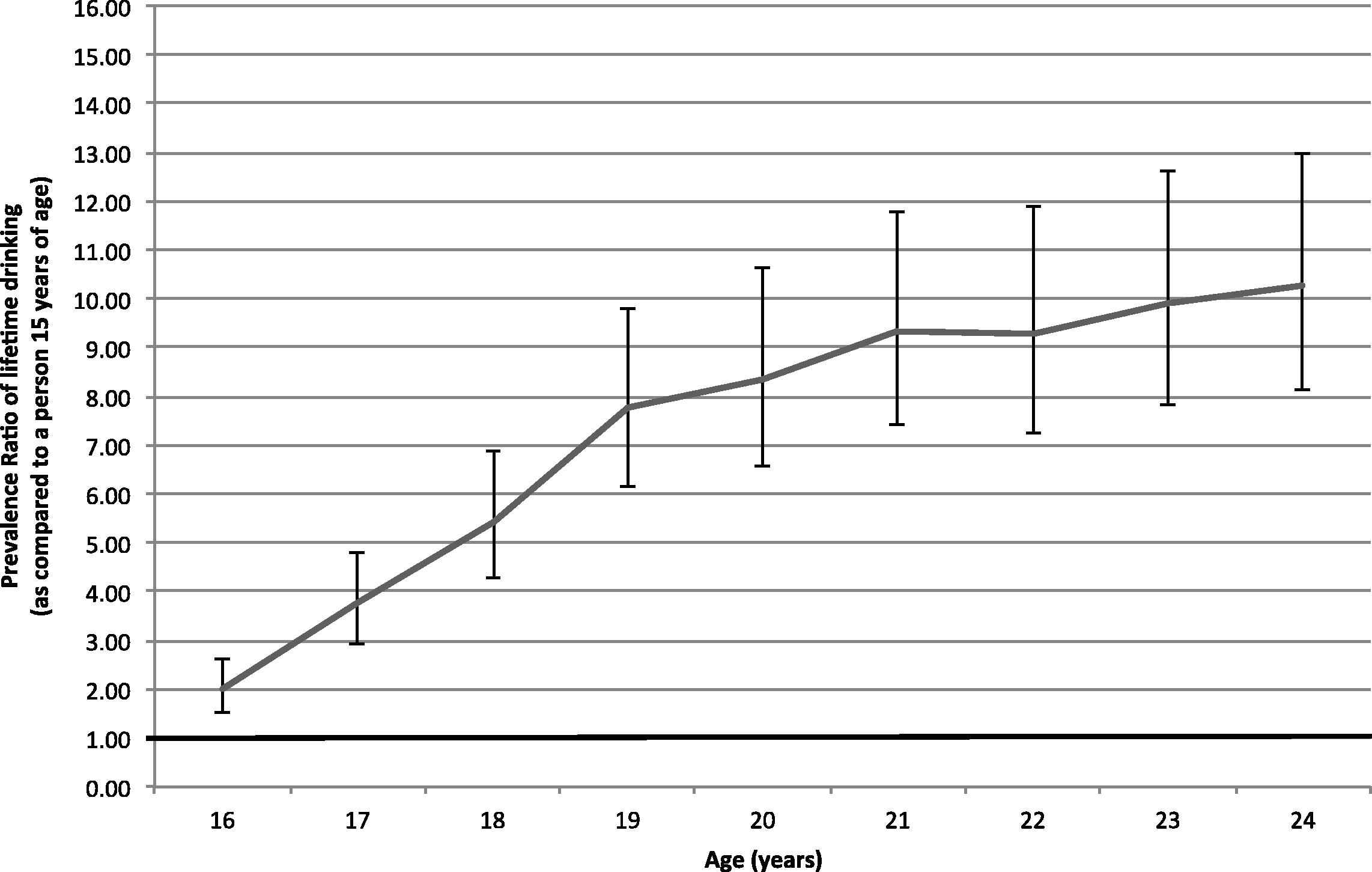

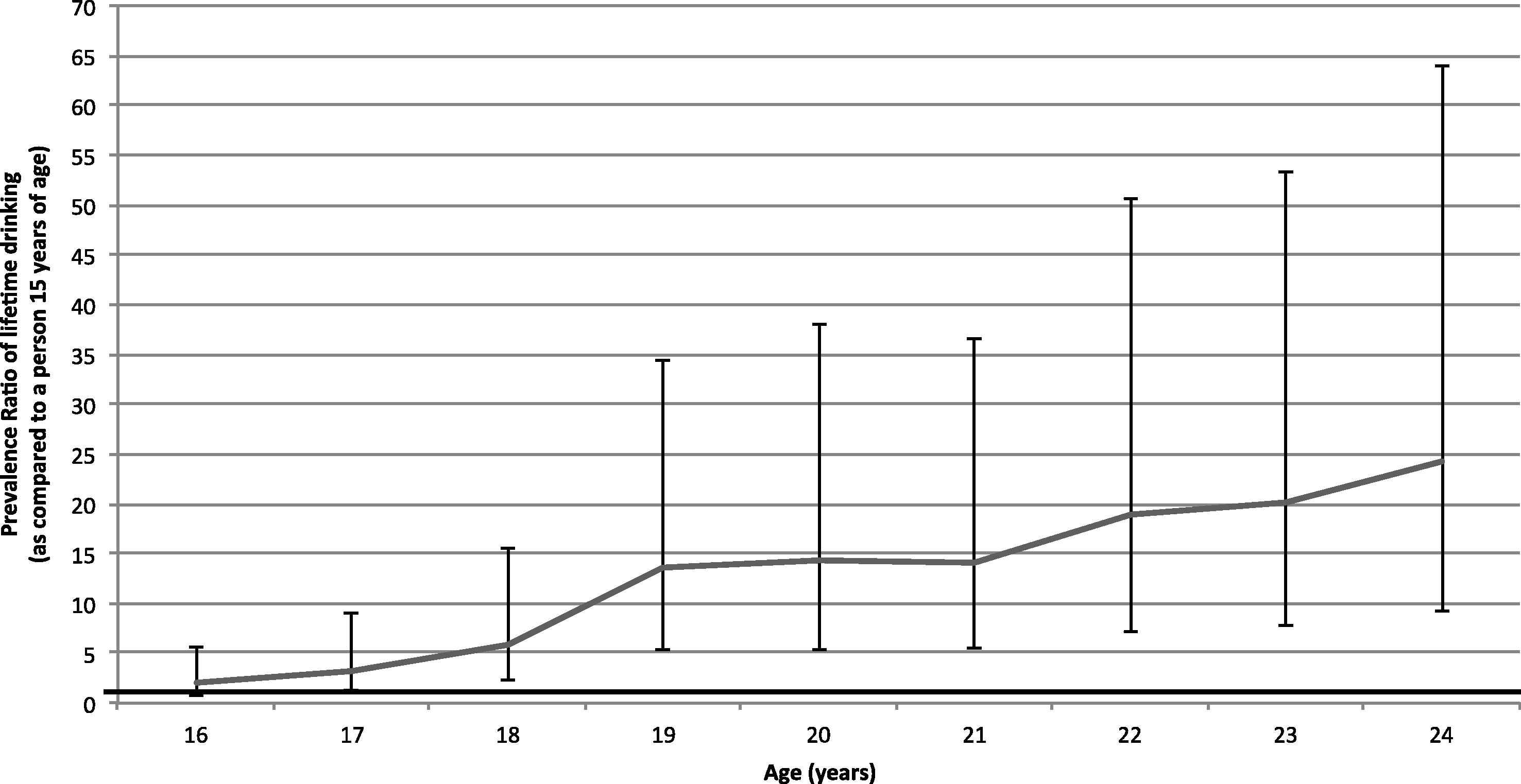

The prevalence of lifetime drinkers in Thailand shows a significant association with age after adjustment for birth cohort, alcohol excise taxation, and demographic variables (see Figs. 2a–2c). For the total sample, as well as for males and females separately, the prevalence of lifetime abstention significantly increased by year after the age of 15, with a steep increase in the prevalence from 15 to 19 years of age, after which the increase is not as marked but still significant. For example, the prevalence ratio of lifetime drinking among people 19 years of age compared with people 15 years of age is 8.27 (95% CI: 6.56–10.42), while the prevalence ratio of lifetime drinking among people 24 years of age compared with those 15 years of age is 11.34 (95% CI 8.99–14.30). The increase in the prevalence ratio of lifetime drinking for those 24 years of age as compared to those 15 years of age was higher among females compared with males, indicating that females tend to initiate drinking in Thailand at an older age than do males.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai youth 16–24 years of age as compared to a person 15 years of age, adjusted for birth cohort, alcohol taxation and demographic variables.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai males 16–24 years of age as compared to a male 15 years of age, adjusted for birth cohort, alcohol taxation and demographic variables.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai females 16–24 years of age as compared to a female 15 years of age, adjusted for birth cohort, alcohol taxation and demographic variables.

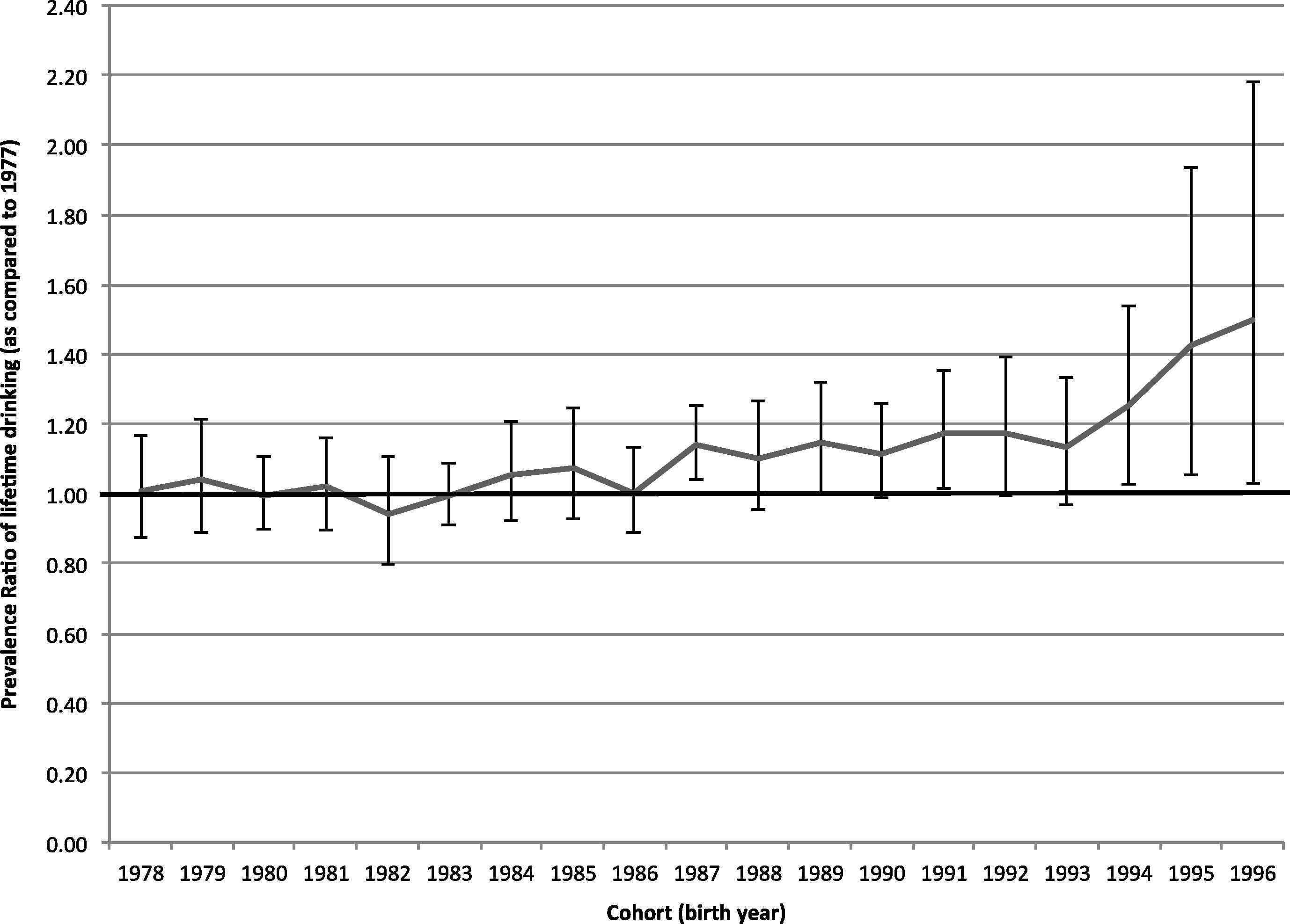

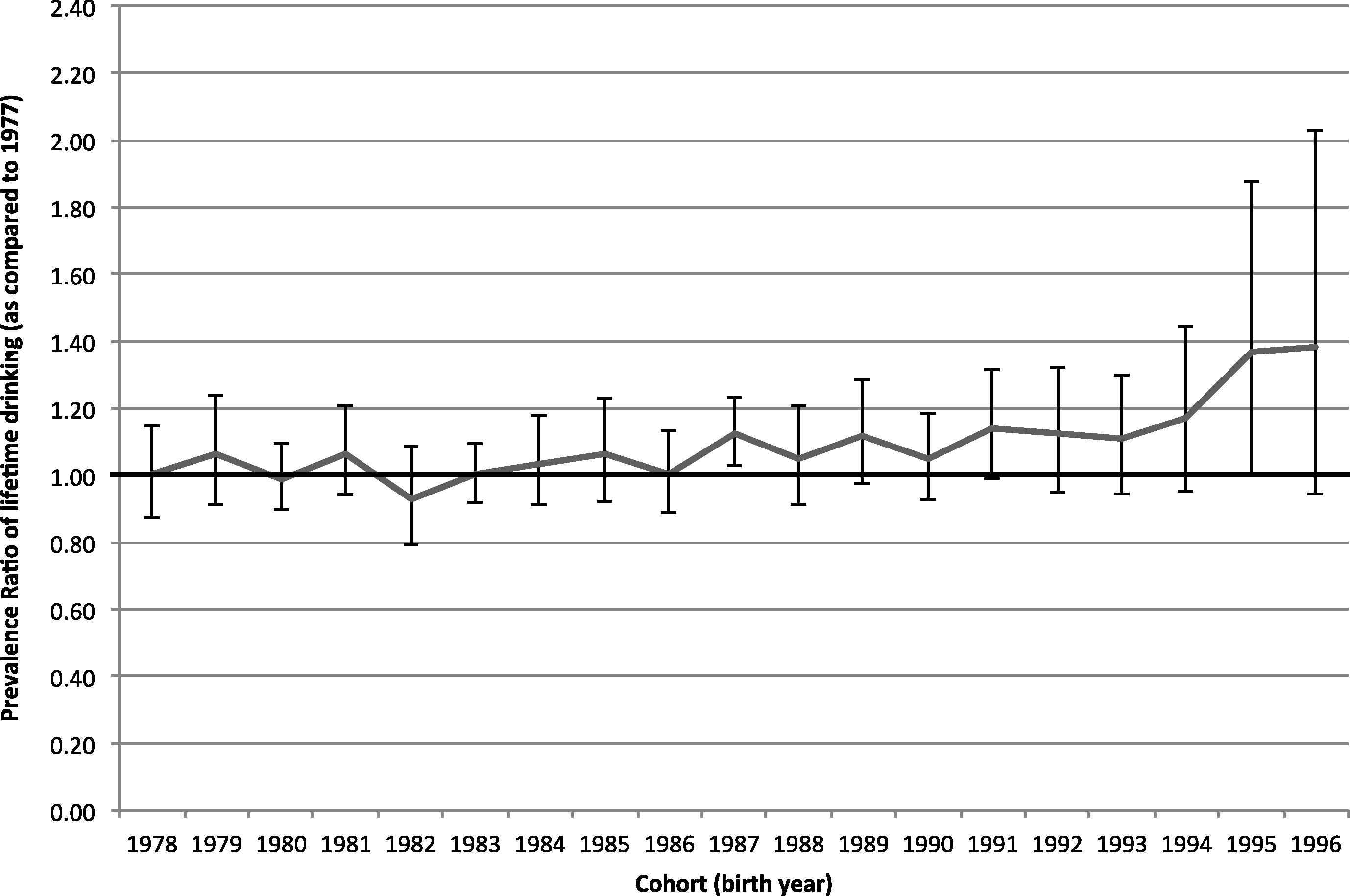

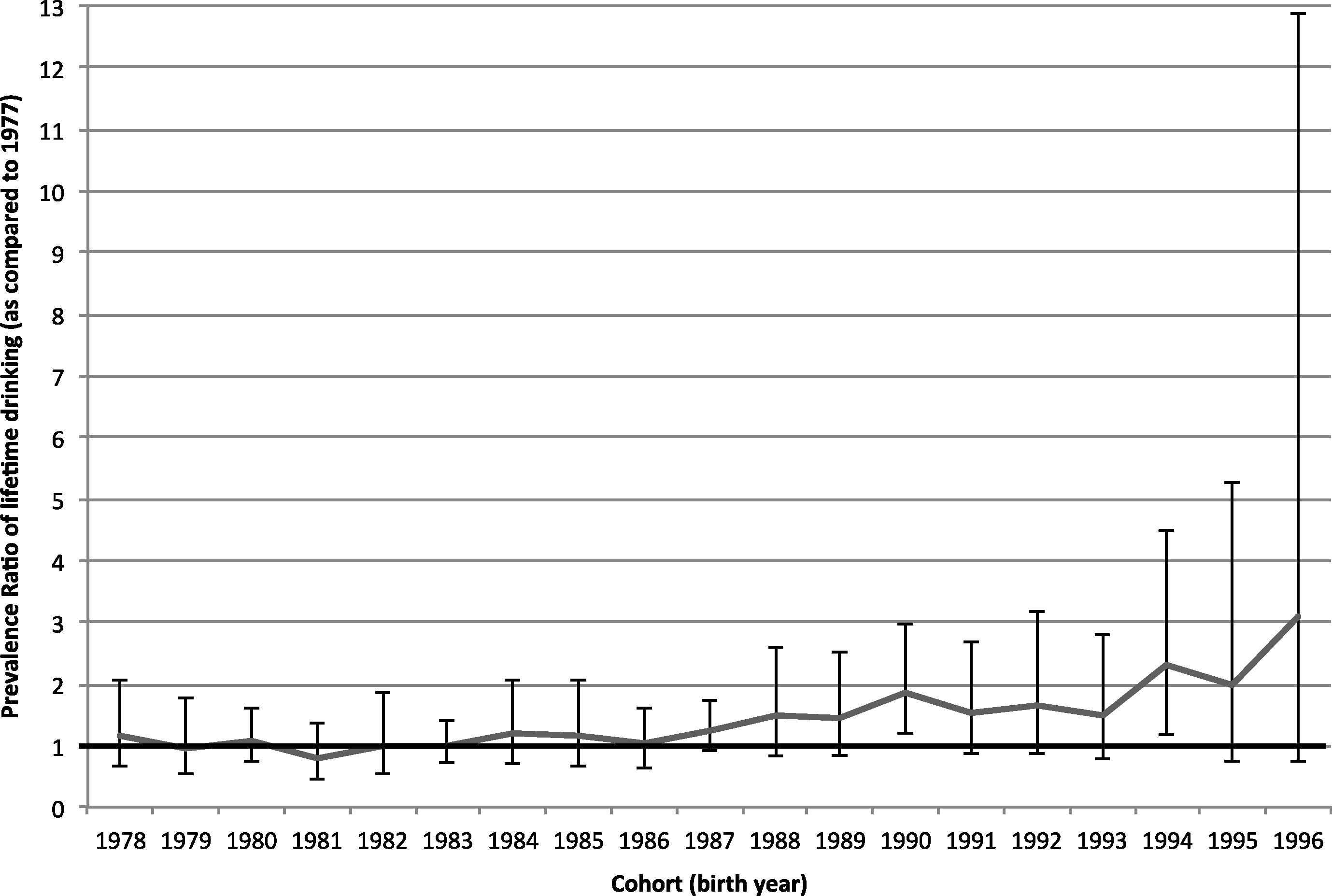

The birth cohort (measured by birth year) shows a clear association with the prevalence of lifetime drinking, while controlling for age, alcohol excise taxation and demographic variables (see Figs. 3a–3c). Among the total sample, the prevalence of lifetime drinking is stable until the 1987 birth cohort, when a significant increase in the prevalence of lifetime drinking can be observed (prevalence ratio of 1.14 [95% CI: 1.04–1.25] for those born in 1987 compared with those born in 1977), after which a slight but significant (p < 0.001) increase can be observed in the prevalence of lifetime drinkers. Similarly, among males and females separately, the prevalence of lifetime drinking is stable until the 1987 birth cohort when a significant increase can be observed.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai youth 15–24 years of age by birth cohort as compared to the 1977 birth cohort, adjusted for age, alcohol taxation and demographic variables.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai males 15–24 years of age by birth cohort as compared to the 1977 birth cohort, adjusted for age, alcohol taxation and demographic variables.

Prevalence ratio of lifetime drinking and 95% confidence intervals for Thai females 15–24 years of age by birth cohort as compared to the 1977 birth cohort, adjusted for age, alcohol taxation and demographic variables.

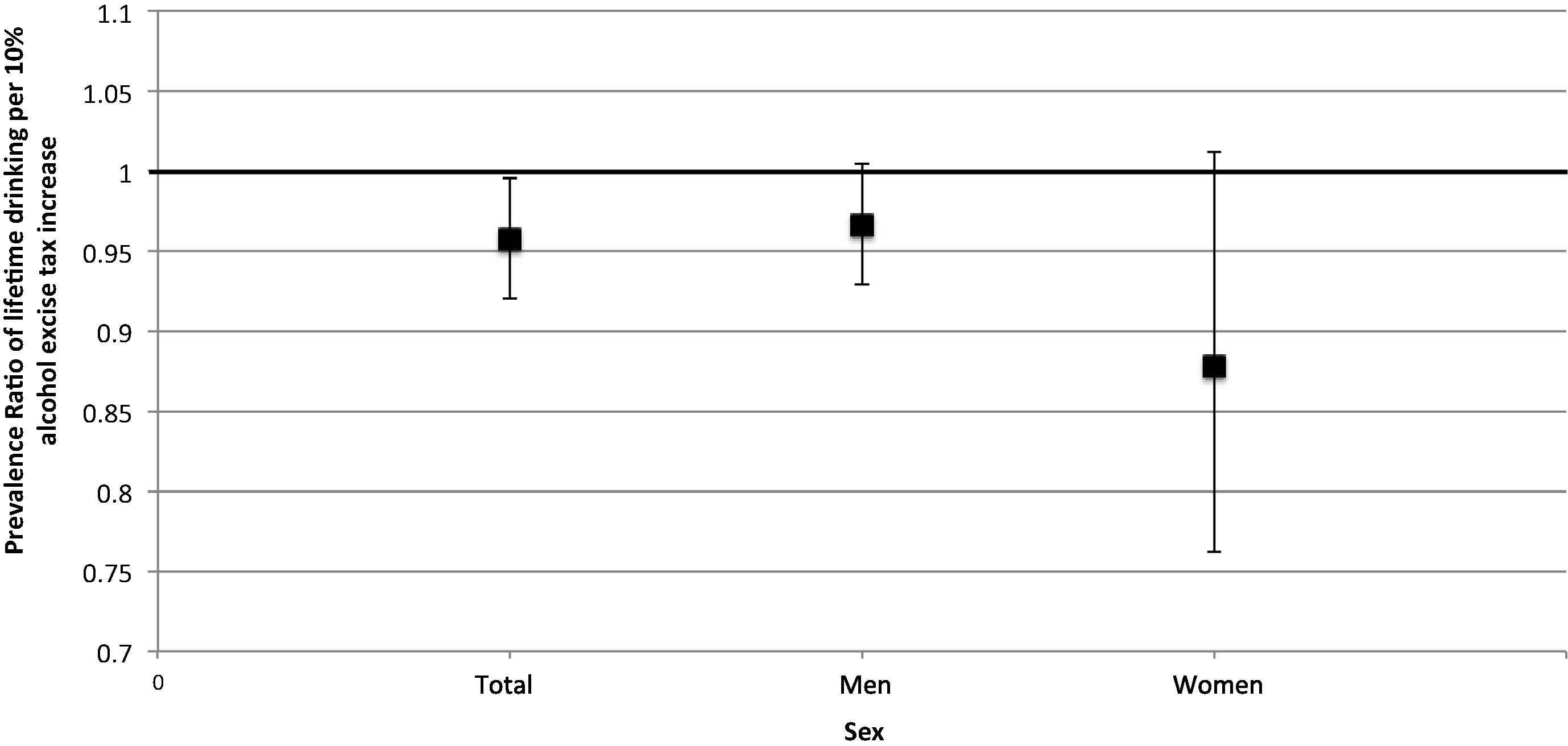

Fig. 4 outlines the association between average inflation-adjusted alcohol excise taxation rate increases and the prevalence of lifetime drinking among Thai youth. It was observed that after adjusting for covariates, an average alcohol excise tax rate increase of 10% was significantly associated with a 4.3% (95% CI: 0.3–8.0%) reduction in the prevalence of lifetime drinking. When this association was analyzed for males and females separately, a non-significant effect size reduction of 3.4% for male youth (p = 0.087) and 13.1% reduction for female youth (p = 0.073) was reported. Further adjustment for age also led to non-significant reductions associated with taxation increases.

Prevalence ratio of lifetime drinking and 95% confidence intervals per an inflation-adjusted 10% increase in alcohol excise taxation (as compared to the alcohol excise tax in 2001) among Thai youth 15–24 years of age, adjusted for age, birth cohort and demographic variables.

4. Discussion

4.1. Results and their significance in light of other research

The social, economic and health burdens caused by alcohol consumption are an increasingly large problem in LMICs, and Thailand is no exception [3]. Recorded per capita consumption of alcohol has increased in Thailand from 0.26 L in 1961 to 6.16 L in 2010, with per capita consumption expected to continue to increase in the future [3]. Furthermore, this study observed an increase in drinking initiation among more recent birth cohorts. Thus, it is imperative for Thailand and similar countries to institute effective policies aimed at reducing the burdens caused by the harmful consumption of alcohol and at preventing drinking initiation among youth.

Through the analysis of data from four large-scale cross-sectional population surveys, with a combined sample size of 87,176 people, this study was the first to observe that alcohol excise taxation increases are significantly associated with decreases in drinking initiation in LMICs, with a 10% increase in the inflation-adjusted tax rate associated with a 4.3% reduction in lifetime drinking prevalence. Thus, alcohol excise taxation increases may present an effective strategy to reduce the burdens caused by alcohol in the long term.

Excise taxation works by increasing alcohol prices, and previous data confirm that this is the case in Thailand [16]. Based on the Center for Alcohol Studies’ data, which were collected from one of the largest supermarket companies in Thailand, the price of the most popular brand of inexpensive whisky increased by 38% between 2004 and 2007 (the tax rate of whisky increased in 2005), while the price only increased by 4% between 2007 and 2011 (no taxation increases occurred during this time). Additionally, between 2004 and 2007 (no beer excise taxation increases occurred during this time), the price of beer in Thailand increased by 3%, while prices increased by 32% from 2007 to 2011 (the excise taxation rate of beer increased in 2009).

The prevalence of lifetime drinkers among Thai youth increased over the study period, from 23.5% in 2001 to 26.0% in 2011 (an 11% increase), while during that same time period Thailand’s GDP (PPP) per capita increased 43.9% from $6500 to $9500 international dollars [23]. The relatively slight increase in the prevalence of lifetime drinkers is less than would be expected given the increase in Thailand’s GDP (PPP) and given the relationship between economic wealth and the prevalence of drinking [16]. Thus, excise taxation should be considered as a measure to control the increasing drinking prevalence in other LMICs. This study also found that the prevalence of lifetime drinkers among Thai youth was low compared with most HICs [3], with about two thirds of the Thai population abstaining at age 24.

It is of interest to note that Thailand’s recorded adult per capita consumption has been relatively stable from 2001 to 2010, increasing only slightly from 6.05 to 6.16 L of pure alcohol (a 1.8% increase) [3], while Thailand’s GDP (PPP) per capita increased 43.9% during that same time period [23]. This increase in recorded adult per capita consumption is less than what would be expected given the increase in Thailand’s GDP (PPP) [21]. This observation indirectly corroborates the present study’s findings.

4.2. Limitations

This study was limited by the absence of data for some potential confounding variables. The available national surveys were designed mainly for assessing current alcohol drinking behavioral patterns and not drinking initiation behaviors. Therefore, potential determinants for drinking initiation (such as parental and peer approval and models for drinking, and youths’ involvement in drug use and delinquency) [24] were not included in the survey questionnaires. Furthermore, data on income were absent for 78,194 of the 87,176 respondents, and, thus, this variable was excluded from the analyses. Therefore, residual confounding may impact these results.

Secondly, the researchers of this study were prone to the limitations associated with all observational studies, since control is limited, and surveys, especially those measuring alcohol consumption, have inherent biases by design (such as populations which are less likely to participate), leading to an inconsistent under-reporting of alcohol consumption [25]. Subjective measures of drinking [25] also limited the scope of the present study; however, objective measures, such as per capita consumption, corroborated these findings.

Thirdly, the researchers of this study were limited by the amount and quality of survey data available for analyses. The prevalence of lifetime drinking among women is lower than among men, leading to a higher uncertainty in the prevalence estimates and in the effectiveness of excise taxes on changing women’s behavior. In addition, the number of surveys that were available also limits this analysis. For the analyses, no significant differences were observed in the prevalence ratio of lifetime drinking for each inflation-adjusted increase in alcohol excise taxation (as compared with the alcohol excise tax in 2001) among Thai youth, adjusted for age, birth cohort and demographic variables for men and women separately; however, a significant difference was found when examining data for men and women combined. This finding of non-significance is due to the number of observations available for analysis. In the future, when more data are available for Thailand covering a longer period of time, this analysis should be updated, as the power to detect this difference will increase.

Most of the strengths of these analyses originate from the individual observations, and, accordingly, these analyses were not able to control for population-level covariates of alcohol policy. These policies include a Minimum Legal Drinking Age (MLDA) of 18 years of age in force since 2003, a Minimum Legal Purchasing Age (MLPA) of 20 years of age, and a partial control on alcohol advertising in force since 2008 which prohibits the use of the product image, but not the brand image. However, the MLDA has not been enforced at all [26], and the MLPA has been virtually unenforced. With respect to the MLPA, a national mystery shopper survey conducted in 2012 found that 99% of Thai youth younger than 20 years of age were able to successfully purchase alcohol without being asked for identification [26]. Furthermore, according to an alcohol advertisement monitoring project, the total number of alcohol advertisements, which included those using brand images and corporate images, on national televisions and in national newspapers did not decrease during the one year period after enactment of the advertising control measure [27]. The small number of available surveys also limits the age, period, and birth cohort regressions. Since there were only four surveys, the interaction between age and cohort was inaccessible, and thus their effects were modeled independently. Therefore, the results should be interpreted with a degree of caution, as there may be an interaction between age and cohort; however, given the time period covered in this analysis, it is likely that the effect of this interaction would be small.

Finally, the data available concerning the informal alcohol market also limited the present study, which did not examine the effects of the informal alcohol market (see Rehm et al. [28] for a list of unrecorded sources of alcohol), estimated to be 0.7 L of pure alcohol per capita in 2010 and, thus, approximately 10% of the total alcohol market [3]. Given the relatively small size of the unrecorded alcohol market in Thailand, it is unlikely to have a large impact on the findings of this study; however, for excise taxation increases to be effective, governments must be able to effectively combat the informal alcohol market [29]. Furthermore, no specific data were available on the market share for alcoholic beverages that are consumed by youth 15–24 years of age; the market share data used in this analysis represent the entire population’s alcohol consumption.

4.3. Future research

The following recommendations, based on the experience of the present study, are for future research to be conducted to detect associations between alcohol excise taxation and drinking initiation. All potential confounding factors, both individual level factors and population level factors (i.e., policy interventions), should be included in the survey instrument design to avoid residual confounding. Additionally, a long series of surveys would allow improved analyses of the interaction between age, period and cohort effect, and the implementation of cohort studies may encourage a detection of drinking initiation by the observed individuals. Finally, comparative studies between countries using data on each country’s taxation system and taxation rates, lifetime abstainer prevalence, and per capita alcohol consumption that takes into account growth in GDP–PPP would help to clarify the differential effects of taxation and GDP-PPP growth on drinking initiation.

5. Conclusion

Alcohol excise taxation increases in Thailand were associated with the prevention of drinking initiation among Thai youth 15–24 years of age. Thus, increasing alcohol excise taxation, supplementary to other alcohol control policies, could prevent drinking initiation among young people in other countries with a high rate of abstainers.

Conflicts of interest

None declared.

Funding

Financial support for this study was provided to Bundit Sornpaisarn by a Canadian Institutes of Health Research Training Grant in Population Intervention for Chronic Disease Prevention: A Pan Canadian Program (grant #53893) and by the Centre for Addiction and Mental Health, Canada, the Thai Health Promotion Foundation, and the Department of Mental Health, Ministry of Public Health, Thailand. Financial support was provided to jurgen Rehm by the Pan American Health Organization/World Health Organization Collaborating Centre for Mental Health & Addiction, the Centre for Addiction and Mental Health, and by the Ontario Ministry of Health and Long-Term Care, Canada.

Acknowledgements

We thank the National Statistics Office of Thailand for the Alcohol and Tobacco Consumption Behavior Surveys data used in this study. We also thank Michelle Tortolo for formatting the references of the article.

Appendix A. Supplementary data

Supplementary data associated with this article can be found, in the online version, at http://dx.doi.org/10.1016/j.jegh.2015.05.004.

References

Cite this article

TY - JOUR AU - Bundit Sornpaisarn AU - Kevin D. Shield AU - Joanna E. Cohen AU - Robert Schwartz AU - Jürgen Rehm PY - 2015 DA - 2015/06/13 TI - Can pricing deter adolescents and young adults from starting to drink: An analysis of the effect of alcohol taxation on drinking initiation among Thai adolescents and young adults JO - Journal of Epidemiology and Global Health SP - S45 EP - S57 VL - 5 IS - Supplement 1 SN - 2210-6014 UR - https://doi.org/10.1016/j.jegh.2015.05.004 DO - 10.1016/j.jegh.2015.05.004 ID - Sornpaisarn2015 ER -