The industrialisation challenge for Africa: Towards a commodities based industrialisation path

- DOI

- 10.1016/j.joat.2014.10.001How to use a DOI?

- Keywords

- African economies; Commodities; Exports; Industrialisation; Linkages

- Abstract

Since the turn of the millennium many African economies have been reintegrated into the world economy on a positive note and experienced substantial economic growth. This growth has primarily been concentrated in commodity exports. The central question facing African economies is how to use economic growth to foster industrialisation and thereby facilitate general development. This paper discusses the extent to which developing backward and forward linkages to the commodity sectors can contribute to its industrialisation project, in light of the past de-industrialisation process and recent trends in global commodity markets. It then reviews the theoretical criticism to resource-based industrialisation and proposes elements for a commodities based industrialisation strategy, including an analysis of the benefits of such strategy for Africa, and the factors contributing to its success.

- Copyright

- © 2014 Afreximbank. Production and hosting by Elsevier B.V. All rights reserved.

- Open Access

- This is an open access article under the CC BY-NC license (http://creativecommons.org/licences/by-nc/4.0/).

1. Introduction

Since the late 1990s, Africa has experienced positive economic growth due to improved macroeconomic management, higher domestic demand, and principally, higher commodity prices. Africa’s central question is how to take advantage of this commodity boom and shift capital, labour and entrepreneurship away from subsistence agriculture and informal employment into the industrial sector. This paper focuses on whether developing backward and forward linkages to the commodity sectors can contribute to its industrialisation project.

2. Linkage development as a window of opportunity for Africa’s industrialisation

Notwithstanding increasing contributions to GDP from manufacturing, financial, telecom and tourism sectors, Africa’s economic growth has been mainly driven by primary commodity exports. Table 1 shows average indices of export product concentration and diversification for selected regions. The export product concentration index (or sectoral Hirschman index) measures the degree of export concentration within a country. The average index for Africa, excluding South Africa, was 0.51 in 2011. In comparison, the average indexes for Asia and Latin America were 0.12 and 0.13, respectively. The export diversification index measures the extent to which the structure of trade of a particular country differs from the world average. This index helps us to overcome a potential problem of the concentration index, that it is more susceptible to commodity price variations. All African countries have a diversification index equal to 0.5 or higher. For almost a third of them, the diversification index is higher than 0.80. This is strikingly higher than Asia (0.24) and Latin America (0.34). Not only export concentration is high in Africa, but it had also increased compared to 1995. During the same period, the diversification indexes of Asia and Latin America, including the LDCs group, have improved. The extent of export concentration is high not only at sectoral level, but also at product level. The top three products represent more than 50% of total merchandise exports for half of the continent. In 8 countries, one single product accounts for more than 70% of total exports. Such export concentration on primary commodities reflects the dependence of African economies on natural resources and the weakness of Africa’s industrial sector.

| Export concentration index | Export diversification index | |||

|---|---|---|---|---|

| 1995 | 2011 | 1995 | 2011 | |

| Developing economies: Africa | 0.24 | 0.43 | 0.55 | 0.55 |

| Africa excluding South Africa | 0.34 | 0.51 | 0.67 | 0.62 |

| Developing economies: America | 0.09 | 0.13 | 0.36 | 0.34 |

| Developing economies: Asia | 0.09 | 0.12 | 0.32 | 0.24 |

| LDCs: Asia | 0.24 | 0.23 | 0.75 | 0.69 |

| Low-income developing economies | 0.14 | 0.25 | 0.57 | 0.47 |

| Major exporters of primary commodities excluding fuels: developing America | 0.14 | 0.18 | 0.61 | 0.64 |

Source: UNCTADStats, accessed in July 2012.

Comparative trade indexes, by region (1995, 2011).

Thus far higher GDP growth rates have not proportionately impacted on poverty reduction. This was because growth failed to translate into commensurate job creation and social progress. Indeed, sub-Saharan Africa, particularly in Central and East Africa, has shown the lowest growth-poverty elasticity in the world (Fosu, 2011). The mineral and oil sectors are capital intensive hence have lower employment linkages than the manufacturing sector. Moreover the potential benefits accruing from higher revenues have often not materialised because of low tax regimes, tax evasion and financial mismanagement.

Africa needs to provide job opportunities to millions of young people. Only a massive industrialisation effort will enable Africa to eradicate poverty and achieve sustainable development. At the same time, this will facilitate dynamic processes of technological innovation, skills development, knowledge-intensification and capital accumulation. Linkage development to commodity sectors can open important opportunities in this respect.

By developing backward and forward linkages to the commodity sector, countries can maximise direct and indirect employment creation effects. Upstream and downstream manufacturing and service sectors offer market opportunities to small and large sized businesses, and mostly skilled and semi-skilled labour. Moreover, in the soft commodity sectors, resource-processing industries can stimulate raw material supply, which creates further employment in the agricultural sector.

By integrating forward linkages, African countries can expect to accrue higher export revenues and foreign exchange earnings. Global value chains (GVCs) refer to the different value-added links, composed of many activities, required to bring a product from conception and design to its delivery to the final consumer and, finally, to its disposal (Kaplinsky and Morris, 2001). GVCs are composed of various stages characterised by varying levels of value addition and, crucially, by different entry barriers. Higher entry barriers, usually created by skills, R&D and technology, allow countries and firms to capture high rents, because there are fewer competitors. Rents are high in activities associated with design, marketing and distribution. Provided their resource-processing industries are internationally competitive and effectively integrated into GVCs, exporting countries can potentially move into higher rent value chain links (Kaplinsky and Morris, 2001; Gereffi et al, 2005).

Industrial development opens up opportunities for positive externalities that are difficult to quantify. African countries can promote a diversification of technological capabilities and of their skills base by developing backward linkage supply firms to the commodity sectors and resource-processing industries. The variety of technological capabilities and skills fostered in linkages also opens up opportunities for lateral migration into other sectors. However, policy makers need to carefully assess the competencies developed within a sector because some have more potential than others for horizontal linkages (Hidalgo et al., 2007). For example, engineering services and manufacturing competencies have a general applicability across a wide variety of sectors. Investment into building broad “engineering skills” is therefore crucial.

Moreover, because the natural resource sector often requires the development of infrastructure to extract and transport the commodities, the potential for linkages is enhanced. This tends to happen more often with high volume mineral resources which usually require roads and rail. As these are developed it becomes easier to develop supplier and resource-processing activities, which in turn increase the economies of scope for further infrastructure development. This positive externality however is rarer in the case of commodities such as oil, gold and diamonds, which promote enclave-type infrastructure (Perkins and Robbins, 2011).

Linkage development also creates the opportunity to maximise positive externalities derived from clusters. When supplier and resource-processing industries are located close to the extraction location, there are agglomeration effects. Efficiency gains for firms located in clusters include gaining access to a pool of specialised labour, and to a specialised network of suppliers. This is particularly important for Africa. By promoting specialised supply networks, buyers accrue advantages in terms of cutting costs, reducing stocks, shortening delivery times, and increasing their flexibly to adjust to new products. The efficiency gains of clusters increase when firms actively cooperate to increase mutual efficiencies. This can take place when firms cooperate to establish training institutes or business organisations, or when they engage in vertical suppliers–buyers cooperation. Clusters also allow governments to catalyse industrial policies, creating economies of scale for investment in skills, technologies, R&D and infrastructure.

3. Commodity price boom and new imperatives for industrialisation

Whilst globalisation has provided industrialisation opportunities to Asia and Latin America, in the 1980s and 1990s Africa suffered the most severe process of deindustrialisation in the developing world (Lall and Wangwe, 1998). The Structural Adjustment Programmes implemented in the 1980s and 1990s largely achieved macro-economic stability but did not enable African countries to adopt export-oriented policies designed to enhance firm capabilities, which was exactly what the Asian countries were doing in the new era of globalisation.

Africa’s marginalisation in manufacturing GVCs is evidenced by its trade patterns. Global trade flows have been increasingly characterised by intra-industry trade in intermediate goods. This is a reflection of trade between lead firms and their suppliers around the world. Whilst Africa’s degree of export orientation and import penetration is high, imports are largely composed of final consumer goods and exports of raw materials. Imports of capital equipment and many intermediaries are primarily destined for commodity extraction.

Some African countries managed to develop manufacturing activities on the back of the US and EU preferential trade access, but these have mostly been limited in scope and size (Kaplinsky and Morris, 2008; Staritz, 2011). Even in their domestic markets, African manufacturers, mainly concentrating on light consumer goods and agro-processing activities, are increasingly under pressure from China’s export competitiveness. Generally speaking Africa’s industrialisation process has been clearly weak and inconsistent — evident from Table 2 which presents the share of manufacturing value added to GDP at the country level. Between 1980 and 2009, this share contracted by about 60% in Chad, DRC, Rwanda; by about 50% in Zambia; by a third in Kenya, Malawi, and South Africa.

| 1970 | 1980 | 1990 | 2000 | 2005 | 2009 | |

|---|---|---|---|---|---|---|

| Algeria | 17.2 | 10.6 | 11.4 | 7.5 | 5.9 | 6.1 |

| Angola | 5.0 | 2.9 | 3.5 | 6.1 | ||

| Benin | 8.0 | 7.8 | 8.8 | 7.5 | ||

| Botswana | 5.1 | 5.1 | 4.5 | 3.7 | 4.2 | |

| Burkina Faso | 17.1 | 15.2 | 15.2 | 16.2 | 14.6 | |

| Burundi | 7.3 | 7.4 | 12.9 | 8.7 | 8.8 | |

| Cameroon | 10.2 | 9.6 | 14.5 | 20.8 | 17.7 | |

| Cape Verde | 8.2 | 9.3 | 7.6 | 6.7 | ||

| Central African Republic | 6.8 | 7.2 | 11.3 | 7.0 | 7.4 | |

| Chad | 11.1 | 14.4 | 8.9 | 5.3 | ||

| Comoros | 3.9 | 4.2 | 4.5 | 4.4 | 4.3 | |

| Congo, Dem. Rep. | 15.2 | 11.3 | 4.8 | 6.6 | 5.5 | |

| Congo, Rep. | 7.5 | 8.3 | 3.5 | 4.0 | 4.5 | |

| Cote d’Ivoire | 10.3 | 12.8 | 20.9 | 21.7 | 19.3 | 18.0 |

| Djibouti | 3.6 | 2.6 | 2.6 | |||

| Egypt, Arab Rep. | 12.2 | 17.8 | 19.4 | 17.0 | 16.0 | |

| Equatorial Guinea | 1.4 | 6.2 | 18.2 | |||

| Eritrea | 11.2 | 6.8 | 5.6 | |||

| Ethiopia | 4.8 | 5.5 | 4.8 | 4.0 | ||

| Gabon | 6.8 | 4.6 | 5.6 | 3.7 | 4.1 | 4.3 |

| Gambia, The | 3.3 | 5.6 | 6.6 | 5.4 | 5.0 | 5.0 |

| Ghana | 13.2 | 8.1 | 9.8 | 10.1 | 9.5 | 6.9 |

| Guinea | 4.6 | 4.0 | 4.1 | 5.3 | ||

| Guinea-Bissau | 21.2 | 8.4 | 10.5 | |||

| Kenya | 12.0 | 12.8 | 11.7 | 11.6 | 11.8 | 8.7 |

| Lesotho | 4.7 | 8.4 | 14.6 | 14.0 | 20.5 | 17.0 |

| Liberia | 4.0 | 7.7 | 9.5 | 12.4 | ||

| Libya | 4.7 | |||||

| Madagascar | 11.2 | 12.2 | 14.0 | 14.1 | ||

| Malawi | 13.7 | 19.5 | 12.9 | 9.2 | 10.0 | |

| Mali | 7.9 | 6.5 | 8.5 | 3.8 | 3.2 | |

| Mauritania | 10.3 | 9.0 | 5.0 | 4.1 | ||

| Mauritius | 15.8 | 24.4 | 23.5 | 19.8 | 19.4 | |

| Morocco | 16.9 | 19.0 | 17.5 | 16.3 | 15.9 | |

| Mozambique | 10.2 | 12.2 | 15.5 | 13.6 | ||

| Namibia | 9.2 | 13.8 | 12.8 | 13.6 | 14.7 | |

| Niger | 4.6 | 3.7 | 6.6 | 6.8 | ||

| Nigeria | 2.8 | |||||

| Rwanda | 3.6 | 15.3 | 18.3 | 7.0 | 7.0 | 6.4 |

| Sao Tome and Principe | 6.4 | |||||

| Senegal | 13.5 | 15.3 | 14.7 | 15.2 | 12.7 | |

| Seychelles | 7.4 | 10.1 | 19.2 | 13.1 | 11.8 | |

| Sierra Leone | 6.3 | 5.3 | 4.6 | 3.5 | ||

| Somalia | 9.3 | 4.7 | 4.6 | |||

| South Africa | 22.8 | 21.6 | 23.6 | 19.0 | 18.5 | 15.1 |

| Sudan | 7.8 | 7.5 | 8.7 | 8.6 | 6.9 | 6.8 |

| Swaziland | 12.5 | 20.9 | 36.8 | 39.5 | 40.0 | 44.4 |

| Tanzania | 9.3 | 9.4 | 8.7 | 9.5 | ||

| Togo | 10.0 | 7.8 | 9.9 | 8.4 | 10.1 | |

| Tunisia | 8.4 | 11.8 | 16.9 | 18.2 | 17.1 | 16.5 |

| Uganda | 9.2 | 4.3 | 5.7 | 7.6 | 7.5 | 8.0 |

Source: African development indicators, accessed in June 2012.

Africa’s manufacturing value added, by country (% of GDP, selected years).

Africa’s re-integration in world trade, therefore, has not promoted the structural transformation of economies towards industrial development. The gap with other developing countries is not only large, but also cumulative and path-dependent (Lall, 2004). Building on a competitive and dynamic industrial base, countries in Asia and to a lesser extent Latin America are moving at faster speed to higher technology and knowledge intensive sectors. This coupled with an underdeveloped industrial base makes it increasingly difficult for Africa to catch up.

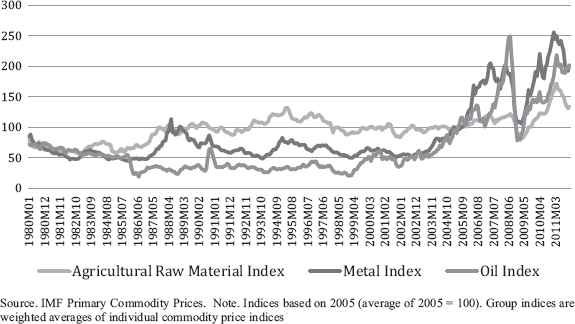

Historically, Africa’s dependence on primary commodity exports and lack of structural transformation was seen in the context of declining or static commodity prices — with the exception of oil. In this scenario, developing countries found it relatively straightforward to adopt policy recommendations that advocated a diversification away from the natural resource sector in pursuance of industrialisation. Fig. 1 shows that from 2003 onwards, except for a short-lived drop from late 2008 to early 2009, all commodity group prices rose substantially. Prices for the metals group did particularly well, before and after the crisis. Whilst there are doubts on whether that long term prices will remain as high as in the 2000s, there is broad consensus that they will not return to 1990s levels. Africa’s industrialisation strategy has now to be formulated in the context of this new trajectory of commodity prices.

Commodity price index, Jan 1980–Jan 2012. Source. IMF Primary Commodity Prices. Note. Indices based on 2005 (average of 2005 = 100). Group indices are weighted averages of individual commodity price indices.

The key driver of the commodity price boom is China (Farooki and Kaplinsky, 2012). Whilst commodity exports are increasingly directed at China and other Asian countries, Asia is also becoming a key source of FDI in Africa’s natural resource sectors (Kaplinsky and Morris, 2012). Africa is a major investment destination for Chinese State-owned Enterprises, and increasingly private sector firms, in search of markets and natural resources. Up until 2005, natural resources were the second most important sector for Chinese FDI stock (Table 3). Since then, even larger FDI flows targeted the service sector and extractive industries (Cheng and Ma, 2010). Natural resources also have attracted large investment from Indian, mainly private investors (Pal, 2008; Pradhan, 2008). Whilst small in global terms, China’s and India’s world FDI is fast-growing. Between 2000 and 2010, India’s FDI flows grew on average by 26.6% per year, China’s FDI flows by 91.7%.

| Sector/industry | Number of projects | Investment value (million, US$) |

|---|---|---|

| Agriculture | 22 | 48 |

| Resource extraction | 44 | 188 |

| Manufacturing | 230 | 316 |

| Services | 200 | 125 |

| Others | 3 | 6 |

| Total | 499 | 683 |

Source. Adapted from UNCTAD, 2007. Note. Based on approved investment projects.

Sectoral distribution of China’s FDI stock in Africa (1979–2005).

The commodity price boom has implications for Africa’s industrialisation strategy. Given the size of China and India’s economies, and the fact that they are in the early stage of their structural transformation processes, resource demand and positive commodity price trends are likely to continue in the long term (Farooki and Kaplinsky, 2012). Africa has major resource endowments — for a large number of minerals, Africa has the largest reserves of any region, frequently in excess of half of the global total (Table 4). However, what is evident is that Africa’s share of global production falls far short of its share of global reserves.

| Mineral | Production | Reserves |

|---|---|---|

| Platinum group metals | 54 | 60+ |

| Gold | 20 | 42 |

| Chromium | 40 | 44 |

| Manganese | 28 | 82 |

| Vanadium | 51 | 95 |

| Cobalt | 18 | 55+ |

| Diamonds | 78 | 88 |

| Aluminium | 4 | 45 |

Source: African Development Bank (2008).

Africa’s share of global production and reserves (%).

The success of rapidly growing emerging economies (particularly China) has led some policymakers in Africa to argue for emulating the Asian industrial strategy. This comprised a mix of protectionism and export promotion, and was successful in integrating and upgrading Asian light manufacturers in GVCs. Some Asian countries’ success expanded beyond garments, toys and footwear, and concerned capital and technology intensive sectors such as the automotive industry. However, in the context of the financial crisis, Asian (and especially Chinese) global competition, and the economic slowdown in developed economies, this route is difficult to emulate. The very rapid growth of the newly industrialised economies based on encouraging manufactured consumer goods exports has produced a structural transformation of global trade militating against others emulating this export-oriented growth path. A number of SSA countries have developed substantial clothing export industries, but these have encountered a major constraint in further expansion into developed economies’ end markets because of increased Chinese and South East Asian competition (Kaplinsky and Morris, 2008; Staritz, 2011). Thus rather than following the classic manufacturing industrialisation route Africa may have to pursue a more complex set of diversified industrialisation paths.

Given the diversity of resource endowment, social and economic background, and geographical location found in Africa, there is no ‘one size fits all’ industrialisation strategy. On the contrary, there are various potential strategies: development of a modern service economy (tourism, IT, transport), low and medium technology manufacturing development in countries endowed with large domestic markets, and resource-based industrialisation in countries rich in natural resources. Indeed, each country is likely to have a multifaceted approach to industrialisation and pursue more than one strategy. What links them all is the necessity for African governments to take action to overcome market failure.

For African countries endowed with natural resources, the recent developments in commodity markets present an added opportunity to promote industrialisation and knowledge intensification processes around backward and forward linkages to the commodity sectors. We draw on the framework of linkage development conceptualised some decades ago by one of the pioneers of development economics, Albert Hirschman (1981). He characterised successful economic growth as an incremental (but not necessarily slow) unfolding of linkages between related economic activities and proposed three major types of linkages from the commodity sector.

- •

Fiscal linkages: The resource rents which the government is able to harvest from the commodity sectors in the form of corporate taxes, royalties and income taxes can be used to promote industrial development in sectors unrelated to commodities.

- •

Consumption linkages: The demand for the output of other sectors arising from the incomes earned in the commodity sector has the potential to provide a major spur to industrial production as all incomes (whether salaries, wages or profits) earned in the resource sector are spent on products and services.

- •

Production linkages: These are both forward (processing commodities) and backward (producing inputs to be utilised in commodity production). Hirschman argued that production linkages paved a path for industrial diversification, because he characterised the industrial development process “… as essentially the record of how one thing leads to another” (emphasis added) (1981:75). Hirschman was however sceptical that the commodity sector would enable countries to develop significant production linkages.

4. Criticism of resource based industrialisation revisited

Resource-based industrialisation strategies are subject to three main types of criticism: a) resource-based industrialisation is as difficult as any other industrialisation path; b) commodity sectors are not likely to promote linkages and externalities: and, c) resource-based industries do not match Africa’s factor endowments.

The first criticism argues that resource-based industries encounter the same obstacles faced by any industry. Proximity of a commodity often does not in itself confer sufficient cost advantages to enable an African country to develop competitive resource-based industries. Other factors, such as infrastructure, human capital, access to capital and skills may be more important in determining final cost competitiveness (Owens and Woods, 1997). However, the experience of resource-rich Venezuela, Argentina, Malaysia and Thailand suggests that the export success of resource-based industries was not so much the result of high level of initial skills and capital, but rather economic policies fostering their accumulation. Resource-based industries developed on initially low skills and capital levels, by mobilising domestic entrepreneurship and implementing effective industrial policies (Londero and Teitel, 1996; Reinhardt, 2000).

These experiences should address concerns that investing resource rents to develop linkages may simply lead to a dissipation of resource rents. Indeed, in many resource based GVCs, rents accrue mostly at the extraction stage. However, because such rents have not been utilised to create broader-based and more dynamic growth trajectories, linkage development strategies remain imperative. If resources were invested effectively and on the basis of a well-focused strategy, as elaborated in the concluding section, this strategy would enable African countries to seize one of few opportunities for industrial development open to them. As discussed below, export-led light manufacturing based industrialisation is becoming increasingly difficult in this respect hence investment in this type of policies may fail. On the other hand, allocating resource rents to social development without an industrial policy has in the past resulted in increased numbers of skilled youth unable to find jobs.

The second criticism is that commodity sectors have an enclave nature, offering limited opportunities for backward or forward linkages with weak positive externalities (Hirschman, 1958, 1981; Singer, 1950). Moreover extractive industries are capital intensive, providing few employment and skills development opportunities. They tend to require less supplier linkages than the manufacturing sector, which implies that technological externalities are lower and incentives for investment in supplier industries are weaker. However the historical experience of many resource-rich countries shows that commodity sectors foster productivity growth, technological innovation, forward and backward linkages, provided they are supported by good institutions and investment in human capital and knowledge (de Ferranti et al., 2002). In Sweden and Finland the development of sophisticated processing industries was mainly the result of investments in skills and research from public and private institutions (Blomström and Kokko, 2007). In addition successful backward linkage industries developed for specialised machinery, engineering products, transport services and equipment. Similarly, the US industrialisation was propelled by resource abundance (Wright, 1990; Wright and Czelusta, 2004). Commodity sectors have promoted technologically sophisticated upstream industries in ‘new’ resource rich countries (Australia, Norway, Scotland). With the right policies and under the right conditions, commodity production can have a positive impact on technological deepening, manufacturing and service upstream/downstream activities, and ultimately growth.

The final criticism is that Africa’s industrial policies should rather be designed for sector intensive in unskilled labour, i.e. light manufacturing, rather than the resource processing industries that are generally capital or skills intensive (Roemer, 1979). This argument is increasingly challenged by the emerging dynamics of GVCs (Kaplinsky and Morris, 2001). Africa’s manufacturing sector has to compete with low-cost exports from Asia, where firms have better access to infrastructure, financial and human capital. This is confirmed by an analysis of unit price trends of imported manufactured products into the EU (1988–2002). These can be assumed to be largely reflective of global unit prices. The first part of Table 5 shows that around a quarter of products exported by low income countries and almost a third of products exported by China faced declining price trends. By contrast, only 7.8% of products exported by high income countries faced declining prices. The second part of Table 5 shows that the declining price trend affected labour/resource intensive sectors and low skills/technology sectors, which are precisely the ones in which Africa competes with China and other low income countries.

| By region | |

|---|---|

| Low income | 25.6 |

| China | 29.7 |

| Lower-middle income | 18.3 |

| Upper-middle income | 17.2 |

| High income | 8.5 |

| By sector | |||

|---|---|---|---|

| UNCTAD classification | Lall classification | ||

| Labour/resource intensive | 69 | Resource based | 61 |

| Low skill/tech/capital intensive | 67 | Low technology | 71 |

| Medium skill/tech/capital intensive | 64 | Medium technology | 59 |

| High skill/tech/capital intensive | 59 | High technology | 51 |

Source: adapted from Kaplinsky and Santos-Paulino (2006).

Products characterised by negative unit price trends based on an analysis of EU imports in the period 1988–2002 (percentage).

The question therefore is not whether Africa can industrialise by “ignoring” its commodities, but rather how the latter can be used to promote linkage development, value addition, new service industries, and technological capabilities.

5. A commodity based industrialisation strategy

As in other industries, the global mining, oil and gas industries have moved away from a high-level of vertical integration towards outsourcing almost every stage in the mining process, (ranging from the provision of capital goods and intermediate inputs such as chemicals to low technology and more basic labour intensive services), to independent firms (Morris et al, 2012). Outsourcing initially targets the lowest cost global supplier, and then, wherever possible, low cost proximate suppliers. Hence increased outsourcing is an opportunity for African countries to increase local content but not a sufficient condition because it could result in increased goods and service imports rather than higher local sourcing. Supplier firms have responded to these opportunities and global mining companies are also actively involved in building capabilities in their suppliers. The desirability of finding efficient local suppliers is particularly attractive in Africa. This is both because transport and logistics are poorly developed and goods brought in from outside may be subject to long and unpredictable delays, and because government policies have often mandated the deepening of local value added. This has been confirmed in a review of 10 country case studies conducted by Morris et al. (2012). When local supplier capabilities are adequate these inputs can be procured domestically and, where possible, close to the point of commodity extraction to save on inventories and transport costs. Large commodity firms have also realised that unless their activities are associated with broader local development, they are likely to face hostility both from governments and local communities. Consequently many companies have signed on to agreements to support local development.

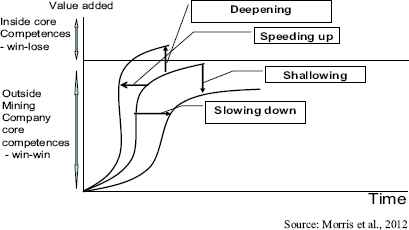

A general model of the trajectory of backward linkage development and the impact of industrial policy on this process has been constructed (Morris et al., 2012) taking account both of the localisation of what was previously imported and the growing trend towards outsourcing by lead commodity firms (Fig. 2). The horizontal axis reflects the passage of time. The vertical axis represents the value added in the provision of inputs into the production of a commodity. The curve shows that, as a general consequence of the outsourcing of non-core competences, there is a market-driven process of linkage development. Initially, the pace of outsourcing is low. With the accretion of technological capacities, the pace of outsourcing speeds up. However as technological and scale requirements become very demanding and the easy hits are exhausted, it tails off. Countries with weak capabilities will be located to the (bottom) of this industry curve and those with strong capabilities to the (top) of the curve.

Different trajectories of linkage development over time. Source: Morris et al., 2012.

There are thus inputs, which the lead commodity producers have no intrinsic interest in maintaining in-house since they do not reflect their core competences, and which they wish to outsource to suppliers in their value chain. So extractive companies may actively want auditing, office provisions and utilities to be provided by outsiders, and in the best of all cases, by reliable and low-cost suppliers based as close to their operations as possible. However there are a range of inputs which are central to the firm’s competitiveness and which it is reluctant to see undertaken by a competitor or outsourced.

Therefore, contrary to the ‘resource curse’ argument, linkage development in the resource sector tends to occur as a natural outcome of market forces, but these “linkage effects need time to unfold” (Hirschman, 1981: 63). The older and more established a particular resource sector, the more likely that local linkages will have developed. Moreover the unfolding of linkages will vary by sector, with the soft commodities at the one extreme and deep sea oil energy commodities at the other (Morris et al, 2012). These linkage relationships are not immutable, both in pace and form. Depending on a variety of determinants they can be altered by purposive state and institutional policy intervention. Hence the curve in Fig. 2, representing different trajectories of linkage (and industrial) development, can be deepened or shallowed, and the process can be speeded up or slowed down as a direct result of effective, ineffective, or indeed the absence of, country specific forms of policy implementation (Morris et al, 2012).

For example, local content policies can move the curve to the left, speeding up the development of backward linkages. This has happened in Angola where increasing levels of basic goods and services to oil extraction are being imported through local firms. The breadth of linkages has increased but not the depth (Teka, 2011, 2012). Local content policies need to be matched by industrial and business development policies as well as high domestic capabilities in order to not only speed linkage development, but also increase the local value added content of such linkages. This is what has been happening in Nigeria, where both the breadth and the depth of local linkages have been successfully affected (Adewuyi and Oyejide, 2012). Weak local content policies and weak industrial policies on the contrary tend to slow down the development of linkages in terms of both the range of supplies sourced locally and local value addition (Fessehaie, 2012). The gold mining value chain in Tanzania is characterised by such dynamics where mines largely rely on imports, and local businesses are not supported in entering the supply chain (Mjimba, 2011). Forward linkage development is subject to similar dynamics. Beneficiation policies adopted by Botswana can move the curve to the left, speeding up and deepening the development of local value addition activities (Mbayi, 2011, 2013). Likewise, Ethiopia’s export taxes combined with local upgrading processes have shifted the composition of the countries exports away from raw hides into intermediate and final leather products (Morris and Fessehaie, 2012).

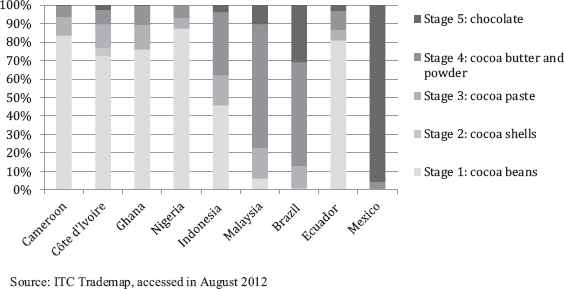

Compared to Africa, various countries in Asia and Latin America have been successful in developing backward and forward linkages to the commodity sector. These are the result of a complex mix of resource endowment, policy, and social, economic and political country-specific characteristics. Fig. 3 compares the value added content of the export profile of selected countries in the global cocoa value chain in 2011. Côte d’Ivoire, Ghana, and Nigeria ranked as, respectively, the world’s largest, second- and third-largest cocoa bean exporters. Cameroon ranked at the sixth place. Their exports profile shows remarkably low levels of value addition; only Côte d’Ivoire and Ghana exported between a fifth and a quarter of their production in semi-processed form. Compared with the two largest Asian cocoa producers, more than 50% of Indonesia’s export value was at the lower and higher end of the semi-processed stages (cocoa paste, butter and powder), and almost all of Malaysia’s export value was at the higher end of the semi-processed stage (cocoa butter and powder). Brazil and Mexico were successful in moving even further up the value chain: one third of Brazil’s and almost all Mexico’s exports consisted of chocolate products.

Cocoa global value chain: Value-added content of selected developing countries’ exports, 2011 (percentage). Source: ITC Trademap, accessed in August 2012.

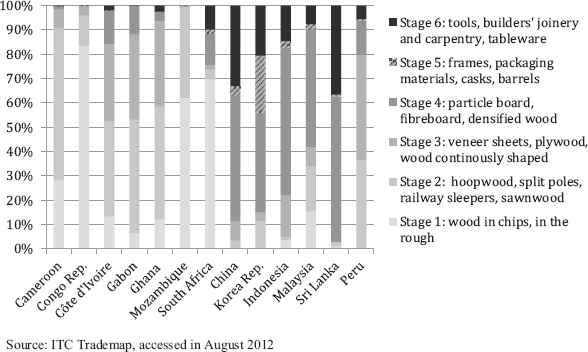

A similar inter-regional pattern can be found in the global timber value chain. Fig. 4 compares the composition of timber exports (excluding furniture) of selected developing countries in 2011. In Cameroon, Republic of Congo, Mozambique and South Africa, three quarters or more of the total export values were in the form of logs or other basic processed forms. Côte d’Ivoire, Gabon and Ghana exported around one third of their production into higher value added form, plywood and veneer sheets. In comparison, major Asian producers exported between 58 and 97% of their timber in advanced processed stages, in particular China, South Korea and Sri Lanka moved into the highest value added stages of the value chain, producing for example frames, tools and tableware.

Timber global value chain: Value-added content of selected developing countries’ exports, 2011 (percentage). Source: ITC Trademap, accessed in August 2012.

Africa’s experience with linkage development has met with modest success (ECA, 2011). In the past this effort focused on state ownership but failed to build market competitiveness. For example, Ghana’s efforts to move into cocoa processing through state ownership performed poorly due to a combination of firm mismanagement and low supply of raw materials (Talbot, 2002). This has been the situation of many resource-rich countries in the 1970s and 1980s, which pursued forward linkage development strategies through strong public participation, tariff protection and high levels of subsidies.

If Africa is to avoid the policy mistakes of the past different strategies for resource-based industrialisation need to be pursued. Firstly, avoid competing simply on the basis of price and rather increase revenues from unprocessed or semi-processed commodities by raising entry barriers to other competitors. This can be done by targeting the high end of the export market through process upgrading and certification (Page, 2012). This strategy can be effective for products such as fresh vegetables and fruits, and speciality products (coffee, cocoa) (Kaplinsky, 2004). These GVCs require efficient services industries (quality control, transport, storage) and technologies. This strategy is being followed by Kenya, Ethiopia and Zambia.

Secondly, develop backward linkages to commodity sectors. Investment in the extractive industries is creating large demand for goods and services. Oil and mining companies prefer to focus on their core business and outsource all non-core activities. Outsourcing is facilitated when undertaken through local, rather than overseas suppliers, because it reduces transaction costs and lead times (Morris et al., 2012). Lead firms have a commercial interest in developing efficient local supply chains. However, this is often not possible because they are not familiar with local suppliers, or because local suppliers cannot meet their market parameters. Whilst with time lead firms will tend to increase outsourcing to competent local suppliers, African countries can intervene strategically to both speed up this process and increase the value added content of the local supply chain.

The third strategy consists of developing natural resource processing industries. Historically these represented on average half of manufacturing activity in lower-middle income countries (Owens and Wood, 1997). Yet Africa’s resource processing industries have performed comparatively poorly, and there has been a deterioration of the technological content of exports from SSA. Between 1995 and 2005, the contribution of primary commodities to SSA’s total export values increased from 61 to 68% (Kaplinsky and Morris, 2008). Conversely, the contribution of resource-based and low-tech industries declined from, respectively, 22% and 6% in 1995, to 16% and 4%. A few factors can facilitate this strategy: lead firms in consuming markets wishing to relocate manufacturing activities, rising fuel costs which may grant weight/volume savings, and growing regional markets.

Finally, whilst much attention has focused on final stages of commodity based GVCs, there is considerable room for African countries to advance into intermediate manufacturing stages in the shorter term: sawn lumber, cellulose, fishmeal, and preserved fruits. These activities are easier to reach than the final stages of beneficiation, and provide opportunities for learning effects, technological capabilities development, economies of scale and positive externalities (Reinhardt, 2000).

6. Factors impacting on a commodity based industrialisation path

The opportunities for linkage development to natural resource sectors are determined by the competitiveness of domestic firms in terms of price, quality, lead times and flexibility. This will define the extent to which they can seize the opportunity to supply commodity lead producers or move into resource processing for the domestic, regional or international markets. Other factors relate to the technical characteristics of the GVCs, the market characteristic and strategies of the lead firms, and the policy framework.

6.1. Technical characteristics of global value chains

GVCs are characterised by different technical characteristics of processing activities. In some commodities, processing has to be carried out shortly after extraction or harvesting in the local economy because the intermediate products are not storable and their essential quality has to be preserved — tea, rubber and palm oil (Roemer, 1979; Talbot, 2002). By contrast, in order to preserve its flavour, coffee roasting and grinding have to be done near the consumption stage. Hence easily storable green coffee beans are the most common form of trading. Forward linkages have been increased in a few producing countries by processing coffee into instant coffee or adopting vacuum packing for roasted coffee, which increases durability but also transportation costs (Kaplinsky, 2004; Morris and Fessehaie, 2012).

Forward integration by commodity producing countries is facilitated when there are many discrete stages of production of storable products within a GVC. Lead firms often find it profitable to outsource the processing of intermediate products to producing countries, whilst retaining control of final manufacturing stages, marketing, and distribution. The chocolate GVC is structured into many stages: harvesting, cocoa bean processing, processing in cocoa butter and paste, and final chocolate manufacturing. The large TNCs have outsourced the intermediate processing stages of the value chain to international trading houses, because this has not infringed on their core business (Talbot, 2002). Hence cocoa processing has been increasingly relocated to cocoa producing countries, including West Africa where these investments have nevertheless not resulted yet in a structural shift in the value added of cocoa exports (Fold, 2002; Kaplinsky, 2004).

The technical characteristics of the value chain also determine the breadth and type of backward linkages. For example, ore extraction is a large-scale activity which requires a broad range of suppliers — ranging from low-skilled, labour-intensive to capital intensive ones. By contrast, sugar production requires a narrower variety and lower value of capital inputs.

The opportunities for linkage development are also shaped by relative factor intensity and varying requirements of firm capabilities. Whilst in general resource processing is capital and skills intensive, mineral processing is more skills and capital intensive than soft commodity processing (Londero and Teitel, 1996). Broadly speaking service-based supply firms are more knowledge intensive and require smaller economies of scale, whilst capital intensive machinery supplies require larger amounts of capital and R&D and have greater economies of scale.

The technological distance between value chain stages determines how firms can move into backward and forward linkages. For example, the capabilities required to process wood into sawnwood, plywood and veneer sheets are different from the ones required for furniture making. In order to undertake this non-linear upgrading, local firms require new capabilities in terms of product design and marketing. Forward and backward integration is facilitated when firms require capabilities similar to their existing ones.

In some value chains, processing enables major reductions in weight/volume, which become critical due to rising fuel prices. For example copper refining reduces the weight of ores by two thirds, with significant cuts in shipping costs (Radetzki, 2008). Weights are halved when processing bauxite into aluminia, and again, into aluminia ingots (Roemer, 1979). Important reductions are gained from timber processing into board products.

Lastly, technological change matters for linkages. The timber value chain has witnessed a major transformation with the introduction of flat-pack furniture in the 1990s, which enabled the outsourcing of lower value added activities to low-cost countries (Morris et al., 2012).

6.2. Industry structure and lead firms strategies

Highly concentrated markets and the strategies of lead firms can result in two different trajectories — captive local supplier networks or capturing forward linkages themselves. In the former, these are networks in which suppliers are transactionally dependent on their large buyers who may support local upgrading processes (Gereffi et al., 2005). This type of market structure and supplier networks could be beneficial for Africa’s industrialisation because it would help address weak local supplier capabilities through buyer–supplier cooperation. However highly concentrated markets can also result in lead firms adopting strategies of forward integration. For example, in the cocoa GVC sector, distribution is dominated by a few large international trading houses which moved from grading and sorting into manufacturing of cocoa paste, powder and butter. Their competitiveness accrues from combining economies of scale and scope in technology, and massive logistical capacity (Fold, 2002). Forward integration by dominating firms raises entry barriers for potential competitors in producing countries (Kaplinsky, 2004). This is particularly problematic when the capital and skill requirements would not be prohibitive for local processing firms.

It follows that linkage development strategies have to take into account the local industry structure and the market dominance of lead firms, and institute appropriate policy interventions. Botswana’s beneficiation policy was designed around restricting marketing of raw diamonds and forcing a cooperative relationship with De Beers, which controls significant levels of global production, as well as marketing and distribution channels, to create local marketing, grading, cutting and polishing (Mbayi, 2011, 2013). The critical elements have been a well-articulated beneficiation policy, with clear targets, a combination of export restriction, penalties and fiscal incentives, private and public investment in public goods and skills creation, and effective implementation. In the timber and cassava GVCs, when African and Asian producers shifted their export markets away from Europe into China, they also reduced their processing capabilities. Processing was increasingly relocated to Chinese food processing and furniture industries (Kaplinsky et al., 2010). Gabon used to export veneer sheet and plywood to the EU. After 2004 a significant section of the market shifted to China, which is more interested in large volumes and low cost supplies, leading to a 500% increase in export volumes, but a downgrading to less value-added raw timber products (Terheggen, 2011). Backward linkage development to Zambia’s copper value chain has been shaped by differences between mining companies (Fessehaie and Morris, 2013). From 2008 onwards, Northern mining companies have increasingly rationalised their supply chains, focusing on value-added supply firms and raising entry barriers to new entrants. They cooperate with their local suppliers to upgrade their processes and enhance their competitiveness. The Chinese mining company offers more market opportunities to local suppliers, but there is no cooperation aimed at local upgrading processes.

6.3. Location

Africa’s infrastructure tends to be unevenly distributed and to be designed to link plantations, oil and mining companies to ports rather than facilitate agglomeration of local enterprises. Oil extraction is supported by pipelines, but they have very little positive spillovers. When infrastructure is poor and commodity extraction is based in remote locations, local supply firms face high marketing and distribution barriers, having to either incur high costs to relocate their businesses, or travel to meet buyers, and arrange transport of supply products or services. However through infrastructure development, the resource sector can prompt the development of local suppliers (Perkins and Robbins, 2011; Morris et al., 2012). Roads or railways, when they are a public good and available to different users, have network effects, and are particularly beneficial to backward linkage development because they reduce costs for local suppliers. Geographical agglomeration reduces marketing and networking costs for suppliers or processing firms, as well as favouring technological spillovers and knowledge flows.

6.4. Trade barriers

Tariff escalation occurs when import tariff levels increase according to the level of processing of imported products. As a result, tariff escalation discourages natural resource-rich countries from moving up their value chains. Africa has traditionally exported to the US and Europe under preferential trade agreements. These granted two orders of benefits: there was no or little tariff escalation and there were valuable preference margins (the gap between the MFN rate and the preferential rate) against competing exports from Latin America and Asia. The erosion, and in some cases the re-negotiation on a reciprocal basis, of these trade preferences poses serious challenges to Africa’s processing firms. Their governments need to address tariff escalation in their export markets at bilateral or multilateral level. Other trade measures impacting on the competitiveness of African processing firms include stringent sanitary and phyto-sanitary standards and technical regulations, non-tariff barriers (NTBs) and agricultural subsidies in export countries.

6.5. Government policies

Technological efforts are critical for upgrading, but they are not costless or riskless. In Africa technological efforts largely focus on searching, buying and experimenting with technologies, and adapting them to local scales, inputs, skills and demand conditions. Nevertheless, institutions to support firm technological capabilities have been remarkably under-resourced, with few exceptions. Comparing Asia and Africa, Lall and Pietrobelli (2005) found that Africa per capita imports of equipment (embodied technology) ranged from very low levels (Uganda, US$ 7 per capita in 2002) to relatively higher levels in South Africa (US$ 165). Yet, these were very low in comparison to Korea (US$ 1031.7 per capita), and Thailand (US$ 403.3). On average, SSA capital equipment imports amounted to US$ 8.2 per capita, East Asia’s to US$ 242.1, and Latin America to US$ 197.9. Compared to Asia, SSA attracted significantly lower levels of FDI into manufacturing, and Africa represented a tiny 1.5% of the licence payments for imported technology paid by developing countries as a group. Total R&D, as a percentage of GNP, stood at 0.28%, compared to an average of 0.39% for developing countries, and 0.72% for Asia. Moreover, most R&D in Africa targets agriculture rather than manufacturing or services.

African firms face significant bottlenecks in skills, technological capabilities and access to capital markets. In 2002, the total number of engineers enrolled in SSA was only 12% of the numbers enrolled in Korea. The weakness of Africa’s industrial policies in the past implies low capabilities of local firms to supply internationally competitive TNCs or to be globally competitive in resource processing. Policies to tackle these market failures are critical to enhance firm competitiveness in undertaking supplying and processing activities.

7. Conclusions

A commodity based industrialisation strategy for Africa based on linkage development cannot be conducted in abstract or aggregate terms, but must be country- and sector-specific. Although there is no single policy that has proven to be undoubtedly successful in promoting linkages, experience points to the importance of isolating a combination of policies and factors. We highlight a few crucial policy issues (see also Morris et al, 2012; Morris and Fessehaie, 2012).

Policies to promote value addition need to be implemented together with policies to raise productivity and product quality in the natural resource sector. Raising the output of the commodity sector enabled the processing industries to reach adequate economies of scale, and governments to sustain investments in ancillary research and technological upgrading (Reinhardt, 2000). Expansion of the natural resource is thus part of the industrialisation effort.

Large domestic or regional markets can be instrumental in linkage development. In the early stages, processing industries can export final products to developing countries, and intermediate products to Northern countries. Only at later stages, it is possible to export final products to meet the stringent requirements of the Northern markets. There is thus an opportunity at a regional or sub-regional level in Africa for greater market integration. If African countries are able to facilitate such integration this would be equivalent to creating large domestic markets which can assist firms in building their competitiveness in final product manufacturing, distribution and marketing before attempting to penetrate Northern markets.

Domestic firm capabilities facilitate linkage development. This raises the importance of industrialisation policies targeted at domestic firms and building on existing capabilities. However, the role of foreign investors is also important and tends to increase with the success of the industry, as more FDI is attracted in both the supply chain and processing activities.

Interventionist state policies play a critical role. Export restrictions have allowed some countries to increase the value added content of exports. However, effective sectoral policies, which selectively allocated resources and created incentives to shift domestic capital and entrepreneurship to targeted industries, have also been critical. Distortions in export markets via tariff escalation, subsidies and non-tariff measures justify government interventions aimed at levelling the playing field and at negotiating international trade agreements that improve market access for their processing industries.

To conclude, linkage development strategies need to target firm competitiveness and encompass the strategies of lead firms. Firm competitiveness is systemic: it is determined by, among others, access to raw materials, technologies, skills, and marketing channels. The strategies of lead firms are critical in determining which value chain parameters have to be complied with, where various stages of the GVC are localised, and whether there will be assistance to upgrade local firm capabilities. In terms of forward linkages, lead firms can potentially have an interest in relocating lower manufacturing stages of the value chain to producing countries, whilst retaining more remunerative processing and marketing activities in the consuming countries. Backward linkage development is often in the interest of the lead firms, especially if price and standard requirements can be met. In particular, backward linkages to mineral and energy sectors are broad. They are formed by supply links characterised by varying combinations of skills, economies of scale, capital, and technological requirements. They therefore open significant opportunities for local businesses.

The main implication for countries embarking on a commodity based industrialisation path is the need for an industrial policy, formulated and implemented in close collaboration with stake-holders. In the short term, industrial strategies should target the “low hanging fruit”, where domestic capabilities are sufficiently competitively, and these are linkages that provide short term returns to lead commodity firms. This may involve labour intensive sectors where low-wages are a competitive advantage. Or it may also involve sectors with a high degree of natural protection. This natural protection may reflect sectors where there is rapid degradation of the product, where there is extensive processing loss, and where transport-to-value ratios are high. Government interventions may be required to overcome information asymmetry and provide buyers with the necessary information to facilitate matching them with potential suppliers. Or it may require national government and ancillary service provider institutions making available sharply directed support to help local suppliers meet a buyer’s particular market requirement.

Beyond this are linkages where embryonic capabilities exist and where there is some prospect, with reasonable time-bound support, that local producers will blossom and be able to compete with foreign producers. Government intervention may need to target technological capabilities, skill development and access to capital. Lack of sufficient and appropriate skills hamstrings local suppliers in upgrading firm level operational competitiveness, meeting technical requirements, instituting innovation, adopting world class manufacturing practices, and implementing successful supply chain and customer management programmes. The general workforce may have gaps in artisanal skills, basic engineering and maintenance skills, machinist and operator skills etc. Supplier firms are often caught in a classic coordination problem — they cannot get into supply chains until their firms exhibit the necessary skills, technology and management capabilities, but they have great difficulty in acquiring these without being involved in supply chain programmes. Building such capabilities requires coordinated firm and government level programmes to upgrade training facilities to the benefit of lead commodity producers, supplier and processing firms.

The final area to develop local value added activities is high profile linkages that are beyond feasible reach in the short to medium term. Whilst governments should lay down the basis for future competitiveness, they are often under considerable pressure to pursue them as short term objectives hence diverting resources away from targets with higher chance of success.

It is critical that this prioritised industrial policy roadmap be developed as an outcome of a cooperative, on-going and informed interaction between key value chain participants such as dominant lead commodity firms, first tier and some second tier suppliers, customers, relevant research and innovation institutions, professional associations and unions. Government role is one of leadership, not in the sense of directing the participants, but rather being the broker bringing everyone together and ensuring that sectional interests are overcome in favour of the collective good. This process should be underpinned by a joint, strategic vision for industrialisation, and by a roadmap specifying activities, outputs, responsibilities and milestones. This platform is also an opportunity to improve coordination between relevant ministries: a commodity-based industrial strategy necessarily requires inter-departmental coordination between agricultural ministries responsible for soft commodities, mining and oil ministries and ministries of industry.

Local content policies have probably been the single most important policy driver of linkages from the commodity sector. Historically in many cases in Africa, local content policies to promote domestic value added have been conflated with indigenisation policies designed to transfer ownership of linkage firms. However, the need to expand local value added economic activities may require attracting foreign investment, skills, and technologies. The goal of developing domestic entrepreneurship on the other hand may require different instruments which range from access to capital to SME development programmes.

Lead commodity firms have the potential to have a major impact on the development of local (backward and forward) production linkages. However, despite it being in the interests of such firms to procure locally, foster local sourcing and develop local linkages, this is often not seen as part of their core business. Governments should engage proactively with the CEOs of the lead commodity firms to develop voluntary and if required mandatory local linkage strategies. These should be accompanied by adequate reporting mechanisms on the extent and nature of local procurement, and a public–private matching fund to facilitate supply chain development.

References

Cite this article

TY - JOUR AU - Mike Morris AU - Judith Fessehaie PY - 2014 DA - 2014/11/24 TI - The industrialisation challenge for Africa: Towards a commodities based industrialisation path JO - Journal of African Trade SP - 25 EP - 36 VL - 1 IS - 1-2 SN - 2214-8523 UR - https://doi.org/10.1016/j.joat.2014.10.001 DO - 10.1016/j.joat.2014.10.001 ID - Morris2014 ER -