Afreximbank in the Era of the AfCFTA

- DOI

- 10.2991/jat.k.211208.002How to use a DOI?

- Keywords

- AfCFTA; Afreximbank; industrialisation; intra-African trade; trade finance

- Abstract

The African Export-Import Bank (Afreximbank) was established in 1993 as a crisis management institution on the heels of the Latin American debt crisis of the 1980s. It has since grown into Africa’s foremost regional integration bank, and is playing a critical role in supporting the implementation of the African Continental Free Trade Area (AfCFTA). In addition to raising resources dedicated to the expansion of intra-African trade and the diversification of sources of growth, Afreximbank has bolstered its trade facilitation programmes and drawn on digitalisation to build an integrated payments system to assuage liquidity constraints and sustainably boost cross-border trade and growth. This paper reviews various innovative measures and facilities deployed by the bank to finance and leverage more resources toward a successful realisation of the AfCFTA.

- Copyright

- © 2021 African Export-Import Bank. Publishing services by Atlantis Press International B.V.

- Open Access

- This is an open access article distributed under the CC BY-NC 4.0 license (http://creativecommons.org/licenses/by-nc/4.0/).

1. INTRODUCTION

The African Continental Free Trade Area (AfCFTA), which entered into force earlier this year, has been touted as a game-changer for its potential to defragment the regional economy and boost intra-African trade and productivity (Fofack, 2018; IMF, 2019). Empirical studies using Computable General Equilibrium (CGE) models indicate that the AfCFTA could boost intra-African exports by more than 20% within a decade of its implementation, and that manufacturing will log the largest gains (IMF, 2019; World Bank, 2020; Songwe et al., 2021; Fofack et al., 2021).

In addition to increasing market efficiency and reducing the cost of doing business—as firms take advantage of rising economies of scale to spread the risk of investing in smaller markets across the continent—the AfCFTA could ease investment flows and shift the composition and direction of Foreign Direct Investment (FDI) to accelerate economic transformation and set the region on a long-run growth trajectory. For instance, many multinationals in the automotive industry have recently established new manufacturing centres or injected patient capital to support the expansion of processing capacities in Africa, which augurs well for the shift in the composition of FDI (WEF, 2021).1

Realising these advancements hinges on overcoming several constraints, not least the financing of continental trade integration reform in a region where huge trade and infrastructure financing gaps have undermined the process of structural transformation and the expansion of cross-border trade (IMF, 2019; Fofack, 2020; Oramah, 2021). In addition to making up for potential losses in tariff revenues, AfCFTA member countries face other costs during the adoption of such reforms, including the need to front-load investments in public infrastructure to boost productivity and support the diversification of sources of growth and trade, as well as developing new and upgrading existing production facilities (Signé and van der Ven, 2019).

The African Export-Import Bank (Afreximbank) was established to play the role of Africa’s Exim Bank to promote and finance extra- and intra-African trade. Since its creation in 1993, Afreximbank has championed the process of economic integration, directly financing the growth of intra-African trade, investing in trade facilitation, expanding trade-enabling infrastructure, and developing technological ecosystems to vault decades-old barriers to intra-African trade and investments. The bank actively supports the implementation of the AfCFTA under its Fifth Strategic Plan, dubbed Impact 2021—Africa Transformed. Recently, Afreximbank has deepened and expanded its support for intra-African trade and is set to raise more than US$40 billion over the next 5 years to facilitate the AfCFTA’s adoption and implementation. This paper reviews the bank’s major initiatives under that resource envelope and outlines the role it will play during the critical opening phase of the AfCFTA.

The remainder of this essay is structured as follows. Section 2 provides an overview of Afreximbank’s mandate, with an emphasis on the promotion of regional integration and financing intra-African trade. Section 3 discusses its different facilities and innovative programmes to support the AfCFTA’s implementation. Drawing on lessons from other regions, Section 4 reviews the role that Development Finance Institutions (DFIs) have played in the process of diversifying sources of growth and exports to deepen regional integration. The last section concludes.

2. OVERVIEW OF AFREXIMBANK’S MANDATE AND ECONOMIC INTEGRATION IN AFRICA

Over the last three decades, Afreximbank—which was established in response to the debt crisis of the early 1980s—has become one of the continent’s most systemically relevant multilateral financial institutions, working directly with member countries, private sector operators, and regional institutions to diversify exports and deepen economic integration.

One of the direct and immediate consequences of that debt crisis was the collapse of commodity prices and the concomitant rise in the ‘twin deficits’ (fiscal and current accounts). Africa, where primary commodities and natural resource exports represented the main sources of fiscal revenue and foreign exchange earnings, was particularly affected. African trade, which had been expanding over the previous decades, decelerated in the 1980s, reflecting both the depth of the debt crisis and the sustained pressure of a balance of payments in a region where most nations remained heavily dependent on commodities (UNCTAD, 2021).2 Similarly, per capita GDP, which had increased in the previous decades, stagnated throughout the 1980s, setting the stage for what some have called the ‘lost decade’ (Artadi and Sala-i-Martin, 2003; Stiglitz, 2017).3

Pro-cyclical moves by international banks and other financial institutions—which withdrew from Africa’s trade financing landscape in droves because of perceived high risk in the region—exacerbated the crisis, undermining African trade and the process of economic recovery. So too did the implementation of contractionary fiscal measures adopted by governments in response to the rising twin deficits (Rodrik, 2006; Fofack, 2014). Besides financing and liquidity constraints, another aggravator of the crisis was the structure of African trade. While a more balanced pattern of trade elsewhere in the world mitigated the impact of negative shocks from spinning out into sustained balance-of-payment crises, the extroverted nature of African trade magnified the impact of these adverse shocks in the region (Brixiova et al., 2015; Fofack, 2020).4

As enshrined in its charter, Afreximbank’s formation was informed by these dual development challenges—trade financing gaps exacerbated by excessive reliance on international financial institutions, and the skewed distribution of African trade toward extra-African activity (Oramah and Abou-Lehaf, 1998).5 The contours of that mandate are summarised in Article II of Afreximbank’s charter. According to that article, the bank was established to facilitate, promote, and finance extra- and intra-African trade. To achieve these goals, it was mandated to carry out several key functions, including, but not limited to the following:

- (i)

to extend direct credit to eligible African exporters, in any appropriate form, by means of providing pre- and post-shipment finance;

- (ii)

to extend indirect short- and, where appropriate, medium-term credit to African exporters and importers of African goods, through intermediary banks and other African financial institutions;

- (iii)

to promote and finance intra-African trade;

- (iv)

to promote and finance exports of non-traditional African goods and services;

- (v)

to provide finance to export-generative African imports, with preference given to imports of African origin, including imports of equipment, spare parts, and raw materials, as deemed appropriate by the bank;

- (vi)

to promote and finance South–South trade (trade between developing economies in the Global South) between African nations and other countries;

- (vii)

to act as intermediary between African exporters and African and non-African importers through the issuance of Letters of Credit (LCs), guarantees, and other trade documents in support of export–import transactions;

- (viii)

to promote the development within Africa of a market for bankers’ acceptances and other trade documents;

- (ix)

to promote and provide insurance and guarantee services covering commercial and non-commercial risks associated with African exports;

- (x)

to provide support to payment arrangements aimed at expanding the international trade of African states;

- (xi)

to carry out market research and provide any auxiliary services aimed at expanding the international trade of African countries and boosting African exports;

- (xii)

to carry out banking operations and borrow funds; and

- (xiii)

to undertake any other activities and provide other services which it may deem to be incidental or conducive to the attainment of its purpose, as determined by the General Meeting of Shareholders of the Bank.6

Successfully implementing the AfCFTA, which aims among others things to boost intra-African trade, will help Afreximbank to deliver on its institutional mandate—a mandate that emphasises the promotion and financing of intra-African trade. The Action Plan for Boosting Intra-African Trade (BIAT), which informed the free trade area’s design, aims specifically at deepening Africa’s market integration and significantly increasing the volume of cross-border trade. At the same time, the diversification of sources of growth associated with the implementation of the AfCFTA will lift the supply-side constraints and boost the production of manufactured goods to further accelerate the expansion of intra-African trade (Songwe et al., 2021).

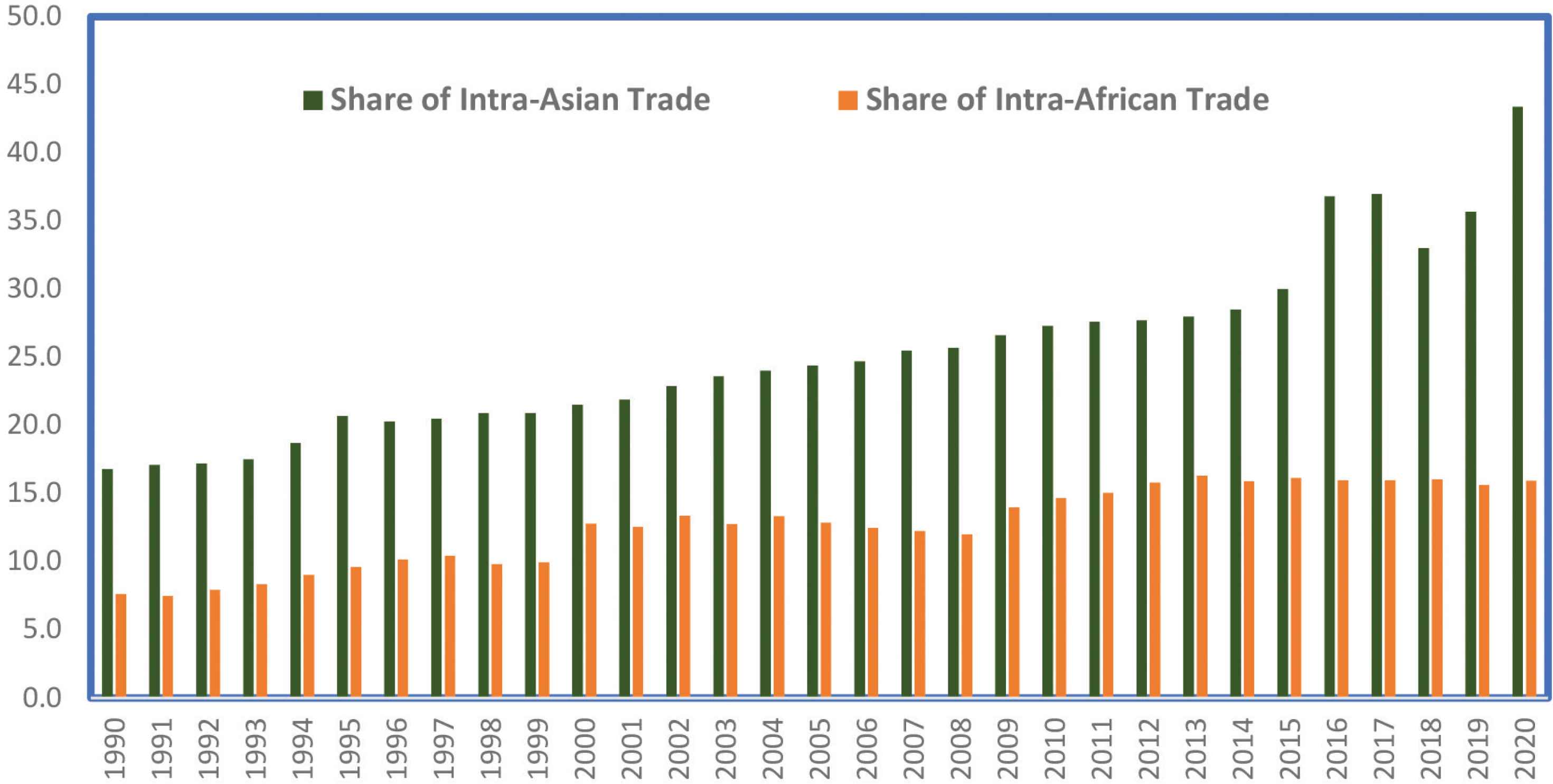

In the early 1990s when Afreximbank was established, intra-African trade accounted for less than 10% of total African trade (Figure 1). Despite the relative increase of that share to around 16%, Africa still compares unfavourably against other regions—72% in Europe and 52% in Asia—leaving plenty of room for growth during the AfCFTA’s realisation. The BIAT Action Plan and the AfCFTA, which jointly offer a comprehensive framework for industrialisation and economic development, are part of broader initiatives under the African Union Agenda 2063 (WEF, 2021).

Long-term trends of intraregional trade as a share of total trade. Sources: IMF Direction of Trade Statistics and Afreximbank Research.

To further support this mandate, Afreximbank made intra-African trade the point of the spear of its most recent five-year strategic plan, which commenced in 2017.7 Under that strategy, the bank intended to bring about a major shift in the composition of its portfolio, raising intra-African trade funding to around 25% of the total by 2020, from 7.4% in 2015, and increasing intra-African trade financing to US$20 billion (Oramah, 2021). Even before the end of that 5-year period, Afreximbank exceeded these targets, with intra-African trade accounting for about 30% of its portfolio halfway through 2021. Since its inception in 1993, the bank has approved more than US$97.7 billion in furtherance of its mandate.

Diversifying the sources of growth to produce more manufactured goods, which falls under the second pillar of the bank’s strategy, will stimulate trade among African countries. Promoting and financing exports of non-traditional African goods and services will accelerate the diversification of sources of growth, as well as reduce the correlation between commodity prices and growth, which has been the bane of African economies for decades (Fofack, 2015, 2021). It will also boost intra-African trade, which manufactured goods dominate (Songwe et al., 2021).8

Provided the rules of origin that afford preferential market access under the AfCFTA do not impose prohibitive costs, they will hasten the diversification of sources of growth, acting as an institutional and industrial accelerator to promote local value addition (UNCTAD, 2019; Fofack, 2020). Afreximbank is currently supporting the industrialisation process through several initiatives and financing facilities. These include financing the expansion of the network of trade-enabling manufacturing to boost productivity and crowd-in private investment. There is also the development of Industrial Parks (IPs) and Special Economic Zones (SEZs), which helped facilitate Asia’s export-led growth model, as an exemplar worth studying and emulating (Rodrik, 2016; Stiglitz, 2017) as well as the development of regional value chains (De Backer et al., 2018). Afreximbank has invested more than US$1.7 billion in supporting the growth of Regional Value Chains (RVCs) to accelerate the process of industrialisation (Oramah, 2021).

Moreover, diversification is buoyed by the bank’s Small- and Medium-sized Enterprise (SME) strategy and its incubation facility. For decades, SMEs have been the backbone of Africa’s economy, accounting for around 80–90% of all formal companies in Africa and providing nearly 80% of total employment in the region (Runde et al., 2021). Their role will become even more important during the AfCFTA’s implementation, especially with the internationalisation of production sharing (UNCTAD, 2013; De Backer et al., 2018) associated with the rise of Global Value Chains (GVCs), a major catalyst for accelerating the growth of SMEs and their transition toward large and multinational corporations, which have been the leading drivers of global trade, as argued by Mold (2021).

Afreximbank supports the growth of African SMEs through its Trade Finance Intermediary model, which distributed more than US$1.6 billion among these entities in 2020. It is expected to ramp up its assistance under its new SME Strategy. The bank’s Fund for Export Development in Africa, which supports the development of African corporations through equity participation and the regionalisation of SMEs, will further catalyse growth, enabling smaller companies to exploit increasing economies of scale associated with the AfCFTA to sustain their growth over time.

Owing to its multiple interventions, Afreximbank has helped member countries better absorb adverse exogenous shocks. Through its investment in the diversification of sources of growth, it supports the AfCFTA’s adoption to boost intra-African trade and will eventually mitigate the region’s exposure to global volatility. More than a crisis management institution, Afreximbank has emerged as the key regional integration bank. Its success and that of the AfCFTA are intertwined and will enhance growth resilience across Africa. Concurrently, the realignment of its strategy will enable Afreximbank to better support the AfCFTA’s execution and enrich its development impact.

3. FINANCING THE IMPLEMENTATION OF THE AfCFTA: THE ROLE OF AFREXIMBANK

Although the AfCFTA’s growth and development potentials are significant, realising these depends on mobilising sufficient resources to alleviate the forces that constrain continental trade integration reform. These restraints are wide-ranging and include both physical and economic infrastructure, supply-side issues undermining the diversification of sources of growth and trade, and a fragmented payment, clearing, and settlement infrastructure.

While a full estimate of the total financing requirements for an effective implementation of the AfCFTA is still in the works at the continental level, preliminary assessments derived from individual nations’ plans suggest the outlay will be very sizeable, especially considering the scale of financing gaps associated with the chronic deficit of trade-enabling infrastructure. AfroChampions, in partnership with the African Union, has outlined an implementation framework under which infrastructure financing requirements exceed US$1.7 trillion (AfroChampions, 2020).9

While no single organisation can mobilise all of the resources necessary for a successful adoption of the AfCFTA, Afreximbank has emerged as one of the leading financial institutions backing the continental trade integration reform. Under its most recent 5-year strategy, the bank has dramatically raised its financing toward the promotion of intra-African trade and is on course to double that amount to more than US$40 billion over the next 5 years (Oramah, 2021). It supports the AfCFTA through direct financing and by employing its convening power to leverage more resources. At the same time, the bank draws on technology and financial innovation to reduce the transaction costs associated with cross-border trade and excessive reliance on foreign currencies in the financing of intra-Africa trade.

This section reviews the bank’s major initiatives designed to support the AfCFTA’s implementation. It focuses on five key programmes and facilities with significant potential for expanding cross-border trade and deepening regional integration.

The first is the direct financing of intra-African trade. Boosting intra-African trade is the impetus behind Afreximbank’s 5-year strategic plan, reflecting the importance of cross-border trade for economic transformation and macroeconomic stability. Around the world, intraregional trade has emerged as an efficient absorber of adverse shocks, mitigating the impact of global volatility and external shocks (Brixiova et al., 2015; Fofack, 2020). The emphasis on intra-African trade also reflects the potential for industrialisation to deepen integration, as well as the scale of trade financing gaps.

According to the latest Trade Finance Survey jointly carried out by Afreximbank and the African Development Bank, bank-intermediated trade finance devoted to financing intra-African trade has remained consistently low across the region (AfDB, 2020). Even though trade finance continues to be low-risk for commercial banks, the share of bank-intermediated trade finance devoted to intra-African trade has accounted for less than 20% of their trade finance portfolios on average. Year after year, investors and traders have cited these finance shortages as a major constraint to trade expansion.

To address the financing gap in the intra-African trade landscape, Afreximbank has dramatically expanded its interventions, deploying more resources toward intra-Africa trade, and ramping up its correspondent banking services. It has also established a special division, the Intra-African Trade Initiative (IATI), to champion intraregional exchange. As a result, the bank’s financing of intra-African trade has increased significantly over the last four and a half years, to US$20 billion on a revolving basis, and that figure is on course to double over the next five years as it seeks to close the annual trade financing gap in Africa estimated by the International Chamber of Commerce at US$110–US$120 billion.

The resources deployed by Afreximbank also support African SMEs, which are expected to play a key role in the diversification of sources of growth and the expansion of intraregional trade. This will prove especially beneficial as African corporate entities spread the risk of investing in smaller markets and take advantage of the rules of origin underpinning the free trade area to expand processing capacities and align domestic production and demand (Fofack, 2020). Table 1 provides a summary of key initiatives undertaken by the bank toward the implementation of the AfCFTA.

| Strategic initiative | Objectives and expected impact | Afreximbank’s direct support |

|---|---|---|

| Pan-African Payment and Settlement System | To facilitate payments for cross-border trade in African currencies, thereby significantly reducing the foreign currency content and costs of intra-African trade. | Afreximbank is backing the clearing of cross-border payments with a US$3 billion facility. |

| African Collaborative Transit Guarantee Scheme | The scheme provides a single technology-enabled transit guarantee that will facilitate seamless movements of goods across multiple borders, and significantly reduce the costs of transit bonds as well as the time to export/import, to enhance the competitiveness of intra-African exports. | The scheme is backed by Afreximbank’s US$1 billion facility. |

| AfCFTA Adjustment Facility | To offset and deal with the potential adverse consequences of fiscal losses that may ensue due to the implementation of the AfCFTA. It will enable African countries and their private sectors to make smooth adjustments to the AfCFTA. | Afreximbank has committed an initial US$1billion to the fund and will engage development partners to raise the fund to US$8 billion. |

| Customer Due Diligence Repository Platform (also called the MANSA Platform) | The centralised platform will ease the costs of conducting know-your-customer checks for African corporates to boost foreign direct investment inflows and trade. | Fully developed and funded by Afreximbank. |

| Trade Information Portal (TIP) and Trade Regulation Portal (TRP) | The TIP and TRP will improve the quality and availability of information, specifically access to country-specific trade and investment regulations in a harmonised system, to enhance efficiency and reduce the costs of trading within the continent. | Fully developed and sponsored by Afreximbank. |

| Africa Quality Assurance Centre (AQAC) | AQAC will offer testing, certification, and inspection to ensure that African products are manufactured to international standards. | Fully developed and sponsored by Afreximbank. |

| Fund for Export Development in Africa | The fund is expected to address the equity and long-term funding gap and attract FDI into Africa to accelerate the process of structural transformation and the diversification of exports. | Afreximbank has invested nearly US$400 million of the initial fund size of US$1 billion. |

| Afreximbank Intra-African Trade Fair | Creates one physical platform for African businesses and countries to showcase their goods, forge and nurture business relationships with other African entities, and find potential investors. | Fully funded by Afreximbank and sponsored by the AU Commission and AfCFTA Secretariat. |

| Intra-African Trade Finance | Aims to build on the US$20 billion that Afreximbank disbursed during the last four and a half years (on a revolving basis) to raise its financing of intra-African trade to US$40 billion and further accelerate the growth of intra-African trade. | Afreximbank will directly provide financing of US$40 billion for intra-African trade. |

| Afreximbank African Automotive Support Facility | Aims to draw partnerships and direct financing to drive the attainment of the automotive strategy and expand industry-led regional value chains to sustain the growth of Africa’s contribution to global motor vehicle production. | Afreximbank has committed US$1 billion to support the emergence of a viable automotive industry in Africa. |

Summary of Afreximbank’s key AfCFTA-enabling initiatives and potential impact

In 2020, Afreximbank, through its 73 financial interventions, supported almost 50,000 SMEs. Moreover, the financing deployed in support of SME growth is expected to amplify the AfCFTA’s development impact. It will stimulate existing and give rise to new RVCs that are more competitive and resilient, further sustaining SME growth and the process of sustainable, structural transformation.

Afreximbank has been building strategic partnerships with national and international institutions to address the trade financing needs of its clients and member countries. The Afreximbank Trade Facilitation Programme (AFTRAF) supports African banks and financial institutions that are contending with the large-scale withdrawal of international banks from correspondent banking relationships as part of de-risking to avoid stringent compliance and regulatory requirements (Erbenova et al., 2016; Oramah, 2017). Since its launch in 2018, AFTRAF has on-boarded over 480 African banks spread across 51 African states. The aim is to grow the number of banks approved to at least 500, accounting for more than 90% of total assets of commercial banks on the continent.10

Afreximbank Trade Facilitation Programme supports African importers to conduct more trade transactions with their international counterparties using documentary credit. Under AFTRAF, Afreximbank offers new uncommitted short-term revolving trade finance facilities, which are used interchangeably among key essential products, including trade confirmation guarantees, LC confirmation and discounting, and irrevocable reimbursement undertaking. Through direct financing, the bank has significantly raised its commitment to the diversification of exports and expansion of intra-African trade and will play an even more important role during the AfCFTA’s realisation, especially after the realignment of its strategy.

The second major initiative is the African Collaborative Transit Guarantee Scheme (AACTGS). Financing extended by Afreximbank in support of the AfCFTA’s implementation also aims to address transport frictions that impede and add expenses to trade on the continent. The average cost of freight as a percentage of value of imports is around 11.4% for Africa, versus 6.8% for developing countries (UNCTAD, 2015).11 Transit costs pile up alongside transaction costs, especially when transit bonds are required at every border.12 These costs impact both the growth of intra-African trade and the industrialisation process.

In response to these challenges, Afreximbank developed the AACTGS, a transit scheme to facilitate the movement of goods within and between Regional Economic Communities (RECs) under the AfCFTA and with third countries using a single technology-enabled transit bond. There are numerous critical interventions under the scheme, including but not limited to the direct issuance of guarantees to large clients, counterparty transit guarantees to local institutions, the automation of transit procedures, cargo tracking, the interconnectivity of customs systems, and one-stop borders posts.

Earlier this year, Afreximbank signed the instruments of accession to the Inter-Surety Agreement for the implementation of the Common Market for Eastern and Southern Africa (COMESA) Regional Customs Transit Guarantee Bond Agreement.13 That instrument paved the way for the enactment of the US$1 billion Continental Transit Guarantee Scheme, of which around US$200 million is earmarked for COMESA. The bank has also engaged the Economic Community of West African States and is working with the African Union and AfCFTA Secretariat to implement the scheme.

The third major initiative that is likely to accelerate the AfCFTA’s implementation is the Pan-African Payment & Settlement System (PAPSS). PAPSS is jointly supported by Afreximbank, the AfCFTA Secretariat, and the African Union Commission (AUC), as well as by African central banks. PAPSS is a digital financial market infrastructure established for the purpose of expanding Africa’s trade and commerce and enabling the economic and financial integration of the continent. The system was approved by African heads of state during the African Union Extra-Ordinary Summit held in Niamey, Niger, in 2019. It is designed to underpin the seamless operation of the AfCFTA in payment services and provide a mechanism for processing, clearing, and settling Intra-African trade and commerce payments in national currencies, minimising the foreign currency component of intra-African trade. It represents the continent’s response to some of the greatest challenges to intraregional trade, notably the liquidity constraints associated with excessive reliance on foreign currencies for intraregional trade.14

By facilitating trade and other economic activity among African countries, most notably through an interoperable, efficient, risk-controlled, and low-cost payment and settlement system, PAPSS has emerged as a robust alternative to the existing correspondent banking payment model in Africa, which has posed multiple significant challenges in executing intra-African payment services, including exorbitant costs, payment delays, operational inefficiencies, limited transparency, and high barriers to change. It is set to fundamentally transform Africa’s fragmented payment and settlement infrastructure, leading to a financially integrated continent and the key driver of the vital financial flows underpinning the AfCFTA.

Pan-African Payment & Settlement System will reduce transaction costs in intraregional trade, with potential reductions in other direct and transaction costs in excess of US$5 billion annually. It will reduce recurrent hard currency liquidity shortages across Africa that have undermined the financing of intra-African trade. Moreover, the operationalization of PAPSS will formalise some elements of currently unrecorded and informal cross-border trade and ultimately boost overall intra-African trade (Afreximbank, 2020).

The fourth major initiative that will enhance the AfCFTA’s adoption by providing short-term financial incentives to governments and private sector operators is the AfCFTA Adjustment Facility. While empirical evidence shows that the free trade area’s long-term benefits are momentous and outweigh the potential losses associated with necessary reform, short-term adjustment costs are equally important (Saygili et al., 2018; Fofack, 2020). These costs are varied and include private adjustment costs through labour and capital markets, as well as public sector adjustment costs through fiscal channels. Preliminary estimates show that tariff liberalisation associated with the AfCFTA could result in a decline in fiscal revenue of around US$12.2 billion across the region (Songwe et al., 2021).15

While the elimination of tariffs will affect countries differently, the ones most vulnerable to fiscal adjustment shocks are also those with high intraregional trade intensity (Fofack, 2020). Across the continent, these include smaller and medium-sized economies that are lightly import-dependent. Considering past experiences of the implementation of free trade area agreements, there is a growing concern that the much higher fiscal incidence in vulnerable countries may undermine their commitment to participate fully in regional trading under the AfCFTA.

The US$8 billion adjustment facility, which Afreximbank is arranging in collaboration with the AfCFTA Secretariat and African Union Commission, will allay these concerns and enhance the effective implementation of the free trade area (Oramah, 2021). Specifically, by enabling countries to adjust in an orderly manner to sudden tariff revenue losses, the facility will enhance the participation of the maximum number of nations, and further increase opportunities associated with greater economies of scale. Simultaneously, and through its support for the private sector, it will help alleviate the supply-side constraints that have undermined the diversification of sources of growth and the expansion of intra-African trade, deepening regional integration.

The fifth initiative to boost intra-African trade and deepen regional integration is the Intra-African Trade Fair (IATF). To close the trade information gap, Afreximbank launched the inaugural IATF in Cairo, Egypt, in 2018 in partnership with the African Union Commission.16 The fair convened more than 1000 exhibitors and provided the opportunity to strengthen links between producers, buyers, and sellers throughout Africa. It enabled manufacturers, international banks, major multilateral institutions, and corporate partners to share trade, investment, and market information.

Olusegun Obasanjo, IATF 2018 Advisory Council Chairman and former president of Nigeria, captured the historic nature of the event and its impact in fostering trade ties throughout the region, the African diaspora, and the world. As he said, ‘The trade fair will contribute towards the implementation of the AfCFTA, which will play a vital role in transforming businesses, economies, and prosperity across the continent.’

By facilitating the dissemination of investment and market information, the trade fair offers a platform for exhibitors to showcase their goods and services, engage in Business-to-Business (B2B) and Business-to-Government (B2G) exchanges, and strike deals. Through B2B and B2G meetings, sovereign and corporate entities shared prospects during the fair. Government representatives showcased key export strengths and scouted for suppliers, buyers, and investors, helping generate US$32.6 billion in deals.

Intra-African Trade Fair 2018 provided a valuable opportunity for key stakeholders to address trade and market information gaps by showcasing the range of industries, products, and services available across Africa. Industrial and manufacturing companies made up more than 60% of exhibitors and attracted more than half of the US$32.6 billion worth of deals closed during the fair. These companies are driving value addition in heavy industry, manufacturing, agribusiness, and pharmaceuticals, among many other sectors, and will play a key role in the AfCFTA’s implementation and development of RVCs.

That base is poised to take advantage of growth opportunities and economies of scale offered by the free trade area, and future fairs will continue to boost their balance sheets to sustain their growth trajectory. The IATF is scheduled to be held every two years, with the second edition—having been delayed by the Covid-19 outbreak—scheduled for November 2021 in Durban, South Africa.

The sixth major initiative is the Afreximbank African Automotive Support Facility (AAASF) to drive the attainment of the automotive strategy and industry-led regional value chains. The automotive industry provides the opportunity to boost industrial output and deepen the process of economic integration through the development of vibrant regional value chains on a continent that has almost all the raw materials needed to manufacture and operate motor vehicles (Deloitte, 2020; WEF, 2021). In addition to mitigating leakages on a continent where excessive reliance on vehicle imports has been a major drain of foreign exchange, the development of the automotive industry will catalyse industrialisation and support the expansion of other strategic sectors and industries, such as iron and steel, aluminium, plastic, glass, carpeting, textiles, computer chips and electronics, and rubber, among others.

Despite the tremendous growth potential enjoyed by the region, including in the abundance of raw materials needed to run the industry and the growing demand for cars in the context of a rising middle class, Africa’s contribution to the global motor vehicle production has remained dismally low, at about 1%, compared to 57% in Asia, 22% in Europe, and 20% in the Americas (Deloitte, 2020; OICA, 2020). The AfCFTA provides the opportunity to develop rules of origin and automotive policies that will allow the continent to set up a viable automotive sector and the creation of a ‘single automotive market’ to drive productivity growth and competitiveness.

Afreximbank is supporting these efforts under its automotive strategy, which is underpinned by three pillars: namely, fostering the emergence of RVC hubs on value-added manufacturing created through joint ventures between global original equipment manufacturers, component suppliers, and local partners; providing financing to industry players and consumers; and supporting the setting of the right automotive policies and capacity-building programmes. The bank has identified several strategic partners and is working with them to support the implementation of its strategy for the development of the automotive industry on the continent. These partners include the African Association of Automotive Manufacturers (AAAM), the AUC, the AfCFTA Secretariat, United Nations Economic Commission for Africa (UNECA), the African Organisation for Standardization (ARSO), and Deloitte.

In collaboration with AAAM and the AfCFTA Secretariat, Afreximbank is undertaking a study on automotive regional value chains to provide guidance on how AfCFTA member countries could collaborate to develop regional value chains. The study will be extended to all African countries in 2022. The bank is also working with the AUC, the AfCFTA Secretariat, AAAM, and UNECA to develop a continental automotive strategy that will provide a clear roadmap for the development of the automotive sector within the continent. Furthermore, Afreximbank is working with ARSO to develop a continental framework for the harmonization of 43 automotive standards to facilitate the development of a viable automotive industry in Africa.

The bank is also supporting the development of the automotive industry through direct financing. It has set aside US$1 billion under the AAASF. The facility is accessible to qualifying requests for developing projects in the auto value chain. The bank has also established a Project Preparation Facility window that supports countries and corporations to prepare projects in the automotive industry and bring them to bankability. Still, Afreximbank is availing project financing for the development of industrial parks for the automotive industry as well as for setting up specific manufacturing units. Finally, the bank is providing trade finance facilities for importing and exporting components, including completely knocked down kits.

In addition to the big-ticket facilities outlined above, Afreximbank is financing and supporting the AfCFTA’s realisation through other strategic initiatives, including those under the African Trade Gateway (ATG) and the development of economic infrastructure. The ATG is an ecosystem of inter-related digital platforms—namely, PAPSS, the Trade Information Portal and Trade Regulation Portal to improve the quality and availability of information and the identification of regional supply chains, and the Customer Due Diligence and Repository Platform (also called the MANSA Platform) to ease the costs of conducting know-your-customer checks for African corporates. Another is the Africa Quality Assurance Centre (AQAC), which offers testing, certification, and inspections to ensure that African products are manufactured to international standards.

Another element of Afreximbank’s financing scheme for intra-African trade is the financing support for value addition and industrialisation. These are essential to ensuring that the greatest benefit from the AfCFTA accrues to the continent in terms of industrial transformation, jobs, and wealth creation. In this regard, Afreximbank is expanding investments into trade-enabling infrastructure and the expansion of economic infrastructure such as SEZs and IPs. SEZs and IPs are key incentives to catalyse investment and boost industrial production in the face of infrastructure constraints. They provide the path to effective integration into the global economy and have substantially lowered barriers in terms of the time and cost of importing and exporting.17 Already, evidence shows that stoppages related to electricity outages are much less frequent for companies in Kenya’s SEZs than for those operating elsewhere in the country (UNCTAD, 2019). They served their purpose markedly well in major export-oriented economies in Asia and are expected to further catalyse industrialisation in Africa and accelerate the diversification of sources of growth to boost extra- and intraregional trade (WEF, 2021).

4. DFIs AND REGIONAL INTEGRATION

The role played by Afreximbank in the AfCFTA’s implementation, and more generally in the transformation of African economies, is likely to increase over time. This would reflect its dual mandate (development and profit-making as a financially sound institution) and the role that similar DFIs play in other parts of the world. The interventions of DFIs have been particularly prominent in the following:

- •

financing long-term investment to support structural transformation;

- •

extending countercyclical financing to soften economic blows during downturns and expand prosperity during upturns;

- •

developing and deepening financial markets, for example by pioneering new financial instruments such as local-currency and GDP-linked bonds;

- •

extending credit lines to commercial banks and direct lending to SMEs; and

- •

financing public goods, such as large physical and economic infrastructure crucial for productivity growth and economic transformation.18

To project the impact that DFIs can have on Africa, it is helpful to examine their influence in other parts of the world. For instance, DFIs have played a key part in the transformation of Asian economies. They provided patient finance for long-term capital development projects that are not funded by private commercial banks (Griffith-Jones, 2016). Their support for SMEs and the development of RVCs has created durable firm-to-firm relationships, deepening the process of trade integration over time. Despite its diversity, Asia has emerged as one of the most economically integrated regions in the world, and it has benefited mightily from growing intraregional trade, accounting for more than 52% of its total trade, up from about 15% in the 1990s.

One public development bank that has been especially effective is the China Development Bank (CDB), the largest such institution in the world and the key financier of China’s five-year strategic plans (Griffith-Jones, 2016; Griffith-Jones and Ocampo, 2019). Over the last two decades, CDB has provided the capital and investment for China—absent, in the beginning, a modern banking system and only small stock and bond markets—to catch up with the largest economies in the world (Sanderson and Forsythe, 2013).19

Other development banks have played similar roles elsewhere, including the European Investment Bank (EIB), the Brazilian Development Bank (BNDES), and Germany’s KfW. In addition to financing SMEs, start-ups, and players in the industrial production and manufacturing sectors, KfW fosters innovation by drawing on its financial wherewithal to leverage investment in new industries with strong growth potential. By dramatically raising its funding of green investment, it has catalysed the process of energy transition in Europe. The EIB is playing a similar role at a larger scale. Through its partnerships with Afreximbank, both institutions are fast-tracking the transition toward energy-efficient growth models in Africa (Griffith-Jones and Carreras, 2021).

One area where DFIs have been especially active this century is countercyclical financing. The increasing scope and frequency of countercyclical support comes down to two factors—first, the shortening of business cycles, as globalisation quickens the transmission of shocks; and second, the pro-cyclical nature of financing extended by commercial banks. These private institutions tend to over-lend in boom times and restrict credit during and immediately after crises, which limits the working capital and long-term finance that is crucial for investment (Griffith-Jones, 2016; Fofack, 2020).

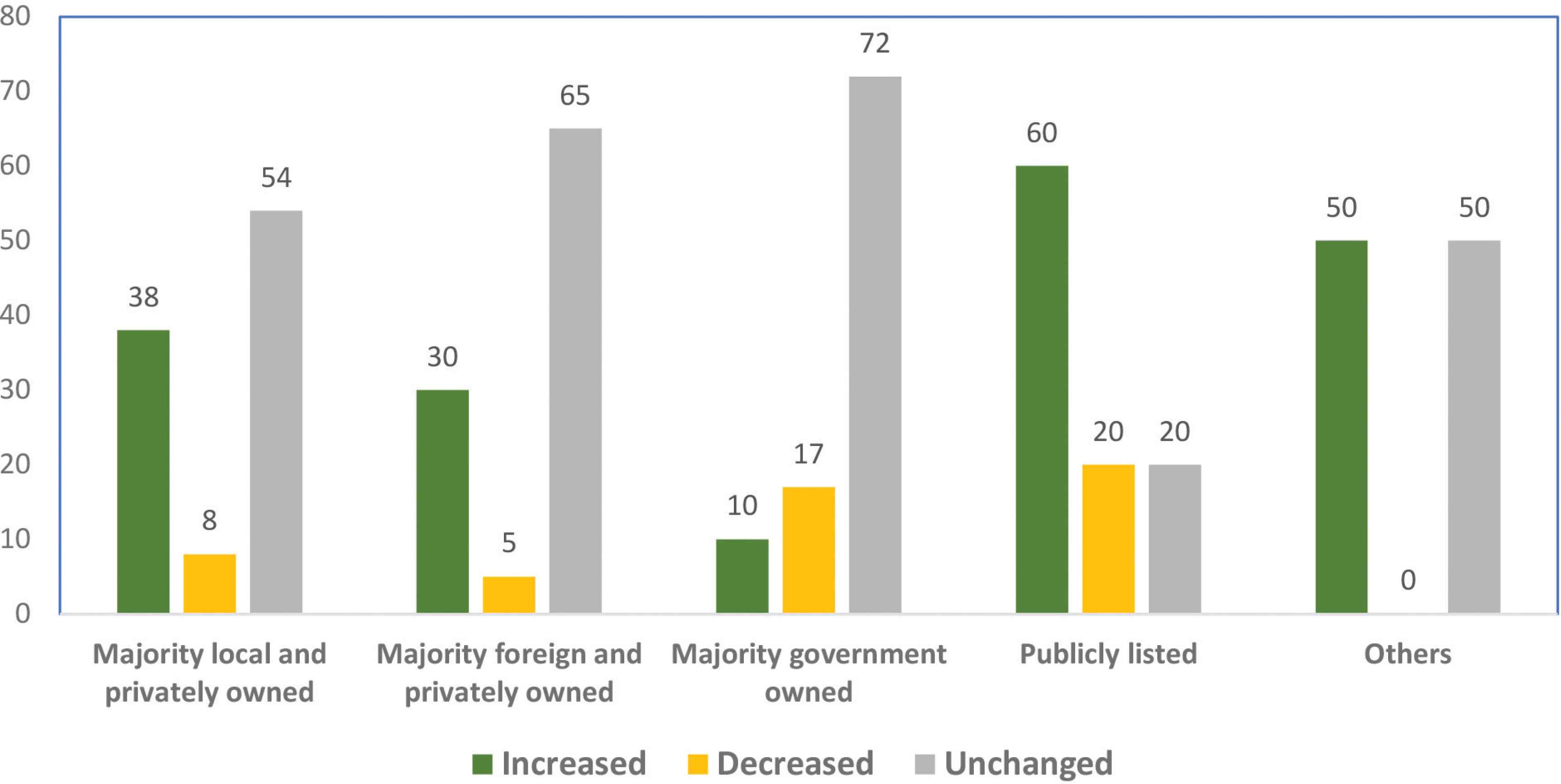

A survey carried out by Afreximbank in partnership with UNECA and the African Development Bank to assess how Covid-19 affected trade finance in Africa showed that private commercial banks (foreign and domestic) cut their financing sharply following the outbreak of the pandemic, citing limited foreign exchange liquidity and decreasing limits with correspondent banks (Afreximbank, 2020). That move dramatically increased their rejection rate of LCs. In contrast, the rejection rate for LCs issued by majority government-owned banks was the lowest (Figure 2).

LC rejection rate—Reported change by type of bank ownership (%). Sources: Afreximbank, AfDB and ECA (2020); Afreximbank Research.

The survey results are consistent with historical and global trends (Micco and Panizza, 2006; Brei and Schlarek, 2013). From an empirical analysis based on an international sample of 1633 banks from 111 countries over the period from 1999 to 2010, Bertay et al. (2012) found that lending by public banks varies less with the economic cycle and rises during times of banking crisis.

Reflecting the increasing awareness of the benefits of countercyclical responses by DFIs during crises and in their aftermath, Afreximbank has emerged as an important crisis management institution. During the last two major economic crises that struck the continent—the end of the commodity super-cycle (2014–2015), and the Covid-19 pandemic—Afreximbank responded boldly. It provided timely countercyclical responses to help member countries better absorb adverse economic shocks, working closely with the private sector to soften the blows and hasten economic recovery.

During the 2015 crisis triggered by the sharp deterioration of commodity terms of trade, Afreximbank disbursed more than US$10 billion on a revolving basis under its Countercyclical Trade Liquidity Facility.20 Responding to the ongoing Covid-19 crisis, it has drawn on its US$3 billion Pandemic Trade Impact Mitigation Facility to leverage more than US$5 billion dollars to help African countries deal with the economic fallout and public health effects of the pandemic.21

Across the world, countercyclical support extended by public development banks has quickened the pace of economic recovery, stabilising fiscal policy by curbing expenditures in times of growth acceleration and providing policy space for higher spending or lower taxes in times of crisis (Griffith-Jones, 2016; Griffith-Jones and Ocampo, 2019). Concurrently, their capacity to inject patient capital for long-term public investment has accelerated the diversification of sources of growth and trade.

While it is difficult to quantify precisely the impact of these development banks in a context of increasing challenges of attribution associated with the multiplicity of actors, counterfactuals can be instructive. India, which has data on the dynamics of gross capital formation in the presence of DFIs and in their absence, provides a framework with which to assess the influence of these institutions.

Development banks were major drivers of capital formation in India from the 1970s through to the turn of the century. As a proportion of gross capital formation in the manufacturing sector, their total disbursement rose from 10% in 1970–1971 to 50% in 2000–2001 (Nayyar, 2018). However, after the closure of these banks in the early 2000s, their outstanding loans dropped from 7.4% to 0.8% of GDP between 2000 and 2010. In comparison, that proportion increased from 6.2% to 11.2% in China and from 8.5% to 15.9% in Germany, two countries where these public development banks remained major actors in the process of economic transformation. Consequently, a growing number of policymakers are calling for the revival of public development banks to accelerate the structural transformation of the Indian economy (Nayyar, 2018).22

Within Africa, recent economic downturns would probably have been much longer—and their consequences all the more devastating, as witnessed during the ‘lost decade’ of the 1980s—if Afreximbank had not been there to provide unconditional and timely countercyclical support. Similarly, if the bank had not been around to deliver assistance under the AfCFTA Adjustment Facility to mitigate the short-term fiscal incidence of essential trade integration reform, securing the continental commitment and broad-based support required for greater economies of scale would have been much more difficult.

5. CONCLUSION

While the expected gains from the AfCFTA in terms of the structural transformation of African economies and the diversification of exports are significant, realising them turns on overcoming several constraints. None is as critical as financing, which is the key to overcoming most other obstacles, including those related to soft and hard infrastructure in a region where the scale of the infrastructure financing gap is magnified by the chronic deficit of infrastructure across the board.

Afreximbank, whose institutional mandate emphasises regional integration and the promotion of African trade, has risen to these historic development challenges and opportunities created by the continental trade integration reform.

This paper outlined the set of programmes and innovative facilities developed by Afreximbank to support the AfCFTA. In addition to markedly raising its financing allocated toward the promotion of intra-African trade, the bank has also emboldened the Industrialisation and Export Development pillar of its 5-year strategy to address supply-side constraints and expand the production of manufactured goods that dominate intra-African trade. Furthermore, Afreximbank has ramped up its trade facilitation programme and developed a system for integrated payments and settlements to assuage liquidity constraints and mitigate transaction costs to ease cross-border trade during the AfCFTA’s adoption.

On the heels of the impressive growth of financial resources allocated to the expansion of intra-African trade over the last 5 years, Afreximbank has set even higher goals, raising its level of resources allocated for the AfCFTA’s implementation to more than US$50 billion over the next half-decade. The bank—which was established in response to development challenges triggered by Latin America’s debt crisis in the 1980s—has, in essence, become Africa’s foremost regional integration bank. Still, the financing requirements for a successful realisation of the AfCFTA remain sizeable. Broad-based support and commitment from all relevant stakeholders will be critical.

In this regard, the backing provided by Afreximbank could help leverage more resources for a successful enactment of continental trade integration reform, which has the potential to accelerate the diversification of sources of growth and significantly boost intra-African trade to mitigate the region’s exposure to recurrent adverse terms of trade shocks. Working together, Afreximbank, business leaders, and African policymakers can bring lasting and transformative change in a region with boundless potential.

CONFLICTS OF INTEREST

The author declares no conflicts of interest.

ACKNOWLEDGMENT

The author would like to thank the anonymous reviewers for their helpful comments and constructive suggestions on an earlier version of this paper.

Footnotes

Intra-African automotive exports accounted for around 16% of Africa’s total automotive exports to the world in 2019. For more details, see WEF (2021).

According to UNCTAD’s most recent biennial Commodities & Development Report 2021, 45 African countries remain heavily dependent on commodities. That number that has barely changed over the last two decades (UNCTAD, 2021).

While Artadi and Sala-i-Martin referred to the sustained economic contraction witnessed in Africa after that crisis as the ‘lost decade’, Stiglitz referred to it as the ‘lost quarter-century’, reflecting the fact that the contraction likely lasted much longer.

Intraregional trade has been an efficient absorber of adverse global shocks in other parts of the world (Brixiova et al., 2015; Fofack, 2020).

At the time, extra-African trade accounted for more than 92% of total African trade. Simultaneously, the geographical distribution of that trade was heavily skewed, with Europe as the main destination, receiving more than 40% of total African overseas exports.

For a comprehensive overview of Afreximbank’s charter, see https://afr-corp-media-prod.s3-eu-west-1.amazonaws.com/afrexim/African-Export-Import-Bank-Establishment-Agreement.pdf.

Industrialisation and Export Development is the second pillar of the bank’s new strategic plan. For more details, see https://www.afreximbank.com/afreximbank-announces-new-strategic-plan-targeting-90-billion-disbursement-over-five-years/.

The composition of intra-African trade, and specifically the manufactured goods content of intraregional trade, is discussed by Songwe et al. (2021).

For more details, see https://afrochampions.org/assets/doc/Contenus%20Trillion%20Dollar%20Framework/THETRI~1.PDF.

For more details on AFTRAF, see https://www.afreximbank.com/products-services/our-key-services/trade-project-financing/trade-finance-programs/structured-trade-finance/afreximbank-trade-facilitation-programme-aftraf/.

Other studies have also confirmed the prohibitively high transportation costs facing African corporates. For instance, a 2016 study by the Development Bank of Southern Africa put transport costs in Africa at 135% higher than in Europe.

Transit and transaction costs associated with cross-border trade in Africa are magnified by geography. The continent has 16 land-locked countries, implying that goods will have to pass through transit nations before reaching their final destination.

For more details, see https://www.afreximbank.com/afreximbank-partners-with-comesa-to-implement-its-us1billion-continental-transit-guarantee-scheme.

For more details, see https://afcfta.au.int/en/pan-african-payments-and-settlement-system-papss.

For more details, see Songwe et al. (2021).

The AfCFTA Secretariat joined as a collaborative partner upon its creation in 2020.

The United Nations Conference on Trade and Development’s review of SEZs emphasises the strong synergy between integrating global value chains and developing SEZs (UNCTAD, 2019).

For more details on the role of development banks, see https://www.brot-fuer-die-welt.de/fileadmin/mediapool/2_Downloads/Fachinformationen/Analyse/Analyse59-en-Development_banks_and_their_key_roles.pdf (Griffith-Jones, 2016).

Since 1994, CDB has financed infrastructure projects (both economic and physical) to the tune of more than US$2 trillion (Griffith-Jones, 2016).

For more details, see https://www.afreximbank.com/afreximbank-board-backs-programme-to-address-africas-trade-finance-liquidity-shortage-bank-to-deploy-over-3-billion/.

For more details, see https://www.afreximbank.com/afreximbank-announces-3-billion-facility-to-cushion-impact-of-covid-19/.

REFERENCES

Cite this article

TY - JOUR AU - Benedict Oramah PY - 2021 DA - 2021/12/17 TI - Afreximbank in the Era of the AfCFTA JO - Journal of African Trade SP - 24 EP - 35 VL - 8 IS - 2 (Special Issue) SN - 2214-8523 UR - https://doi.org/10.2991/jat.k.211208.002 DO - 10.2991/jat.k.211208.002 ID - Oramah2021 ER -