Prospects and Challenges for Supply Chain Trade under the Africa Continental Free Trade Area☆

, Anna Twum2,

, Anna Twum2, - DOI

- 10.2991/jat.k.210105.001How to use a DOI?

- Keywords

- Africa; trade; global value chains; supply chain trade

- Abstract

African countries are negotiating the African Continental Free Trade Area with the aim to spearhead global value chain (GVC) trade among African countries as a driver for robust economic growth. This paper evaluates the participation of Sub-Saharan African Regional Economic Communities (RECs) in GVC-related trade over the period 1990–2015 using measures of backward, forward, regional, and non-regional GVC participation. We find that participation of African RECs in GVC trade (regional and non-regional) has increased but still lags behind comparator groups. Overall, African RECs have participated mostly in non-regional value chains, and along forward rather than backward activities. This is in contrast to comparator groups where supply chain trade has veered toward regional value chains (RVCs). For African RECs, only between 0.5% and 3% of total gross exports are related to RVCs compared to the RVC participation rates for the Association of Southeast Asian Nations (ASEAN) and the Southern Common Market (MERCOSUR): 17.2% and 4.6%, respectively. Controlling for per capita income, we find, using a sample of 149 countries over the period 1995–2015, that overall GVC participation is negatively associated with tariffs on imports and exports of intermediates as well as on trade costs. Backward GVC participation is also positively associated with the number of mobile phone subscribers, a proxy for digital connectivity. These correlations are supportive of policies that would lower trade barriers across the board.

- Copyright

- © 2021 African Export-Import Bank. Publishing services by Atlantis Press International B.V.

- Open Access

- This is an open access article distributed under the CC BY-NC 4.0 license (http://creativecommons.org/licenses/by-nc/4.0/).

1. INTRODUCTION

A key objective of the African Continental Free Trade Area (AfCFTA) is to develop regional value chains (RVCs) to help grow and diversify the manufacturing sector, an objective taking a new urgency under the Coronavirus Disease (COVID) pandemic where the future of supply chain trade remains uncertain. Participation in global value chain (GVC) trade depends heavily on low trade costs that, in turn, depend on low tariff and non-tariff trade barriers. Currently, the average tariff on intermediates across African countries is about 10%, about twice the rate for other developing regions (AEO, 2018; Figure 3.11). In the East African Community (EAC), arguably Africa’s most integrated Regional Economic Community (REC), an agreement has been reached to move from a three-band tariff structure to a four-band tariff structure.1 The objective of this revision at the EAC level—and of the move toward free trade at the AfCFTA level—is to boost supply chain trade (regional and non-regional) value chain trade at the REC and continental levels.

Against this backdrop, the paper evaluates Sub-Saharan African (SSA) participation in GVC trade at the level of four major SSA RECs: the EAC, the Economic Community of West African States (ECOWAS), the Southern African Development Community (SADC), and the Common Market for Eastern and Southern Africa (COMESA). First we track changes in GVC trade over the period 1990–2015 using a database of trade in value-added following the methodology described by Borin and Mancini (2019) constructed from Inter-Country Input–Output (ICIO) tables.2 Results for SSA RECs are compared with two comparators: the Association of Southeast Asian Nations (ASEAN), and the Southern Common Market (MERCOSUR).

The dataset used in this paper was first analyzed in the recently published World Development Report 2020: Global value chains: Trading for Development. To the best of our knowledge, our paper is the first systematic and comparative presentation of the evolution of GVC trade in SSA using the novel dataset from Borin and Mancini (2019).

We report estimates of GVC trade in Sections 2 and 3 and show that African RECs have participated in the worldwide trends of a rising share of trade in value-added (relative to gross trade), although this participation has been mostly forward rather than backward participation as well as more non-regional rather than regional. As an example, compared with other Regional Trading Arrangements (RTAs) and RECs, the EAC has the lowest RVC participation rate among comparator groups (the EAC participation rate is about 1.7%, whereas the highest, in ASEAN, stands at 17.2%). This indicates that less than 2% of total exports from the EAC region are related to regional (EAC) value chains.

Section 4 reports panel regressions for three GVC measures (overall GVC participation, backward and forward shares of GVC-related trade) for a sample of 149 countries over the period 1995–2015. The objective of this section is to see if the data reveal distinct correlation patterns for policy-related trade costs (tariffs, connectivity) and nondirectly policy-related [market size, Foreign Direct Investment (FDI), manufacturing share] factors. Furthermore, we present results for the SSA region to understand how these relationships play out for SSA countries and how these differ from the relationships observed at the global level.

Section 5 concludes. An online supplementary annex includes additional graphs and econometric specifications. Further details on our findings are available in the discussion paper version.

2. AFRICA’S PARTICIPATION IN GVC TRADE

2.1. Overall GVC Participation

Participation in supply chain trade is captured by the GVC participation rate (GVCs), which is the share of country s exports that either makes use of value-added imported from another country or is exported to another country for further processing expressed as a share of gross exports. The participation rate is the sum of the backward (GVCbs) and the forward (GVCfs) participation rates:

Backward GVC participation (GVCbs) measures the share of country s’ exports that include value-added previously imported from abroad. For example, if Rwanda imports maize from Uganda for the production of fortified foods for export, then Rwanda is said to be engaging in backward GVC participation.

Forward GVC participation (GVCfs), the other component of GVC participation, measures the share of a country’s exports that are used by an importing country to produce for export. In the example of fortified foods exports, Uganda is engaging in forward or downward GVC participation because its exports are used as intermediates by Rwanda for the production of its fortified food exports.

Global value chain participation can also be viewed as a combination of RVC participation and non-RVC participation:

Regional value chain participation, which we focus on in this paper, is defined as the share of gross exports that cross at least two borders within the same defined region, A (e.g., EAC, SADC, ASEAN). In this setting, backward participation shares for RVC trade measure the regional import content of exports from a member of region A and forward participation shares measure the value-added in A directly exported to a member of region A then reexported.3

To measure GVC participation, we leverage the global ICIO tables using a new dataset from Borin and Mancini (2019). The database covers the period 1990–2015 for 189 countries and 26 sectors and is the largest country coverage available with estimates that are globally comparable.4 Many papers in the GVC literature use the EORA database to estimate the value-added embedded in a country’s exports because of a larger country and sector coverage.5 Section 1 in our Online Supplementary document provides more detail into the estimation of these different GVC measures.

2.2. Supply Chains: Regional (RVC) versus Non-regional (GVC) and by Type (Backward vs. Forward)

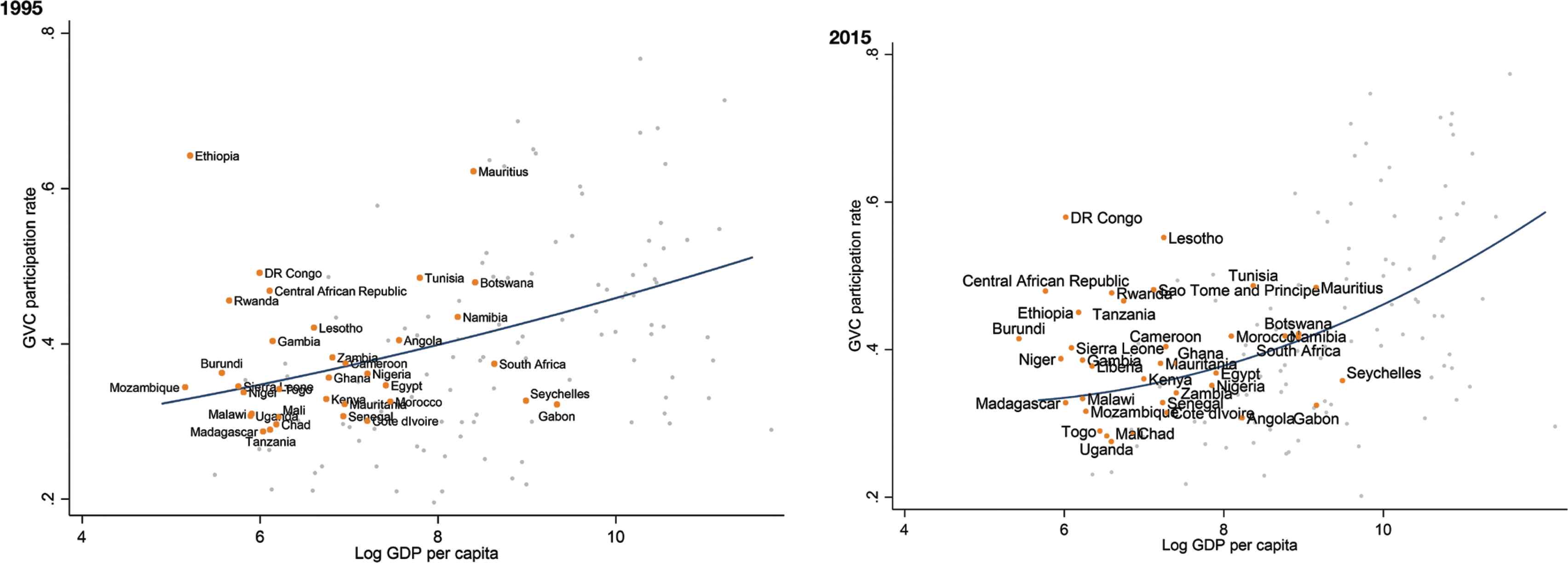

The EORA database is the most comprehensive data for GVC analysis in terms of country coverage and time span. As a preliminary check on the data, Figure 1 plots GVC participation against per capita income in the data for the beginning and end of a period. The figure shows a reduction in per capita income spread across the sample over the period. In 1990, Lesotho and Mauritius had suspiciously high GVC participation rates. Aslam et al. (2017) compare estimates of GVC participation from the EORA database with those obtained from the Organisation for Economic Co-operation and Development (OECD)–World Trade Organization trade in value added database covering OECD countries. Their comparisons reported in Tables 7–13 at 5-year intervals over the period 1995–2010 show a reasonably close fit between estimates from the two databases. Therefore we accept the data as is in this paper.

Global value chain (GVC) participation versus per capita income African countries.

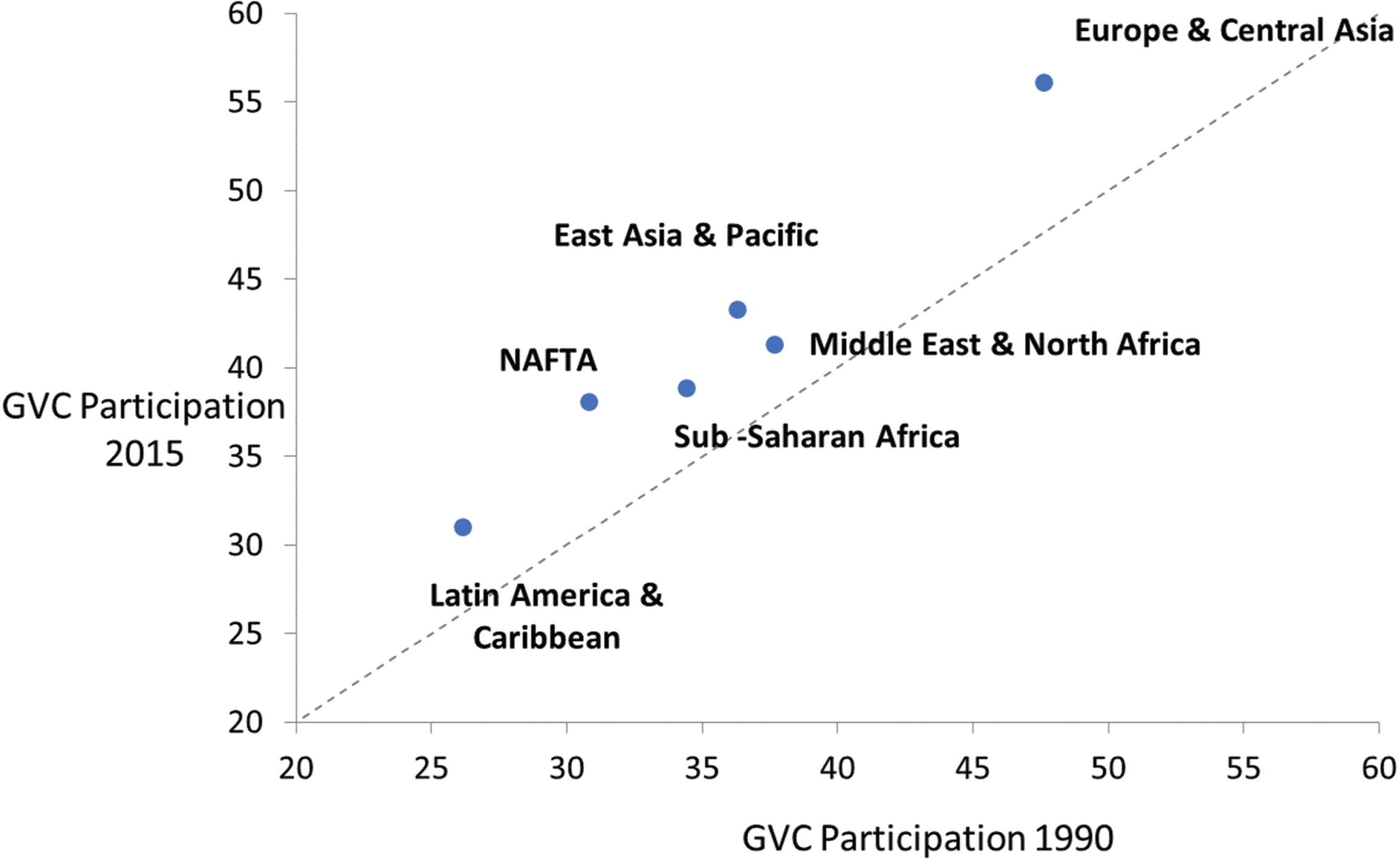

Globally, in spite of the recent decline in overall GVC participation since 2011 (World Bank, 2020), all regions have increased GVC participation over the period 1990–2015 (in Figure 2, all points are above the 45° line). The Europe and Central Asia region leads with about close to double the GVC participation rate of Latin America and the Caribbean. Along with North American Free Trade Agreement (NAFTA), Europe and Central Asia is the region that registered the largest increase in participation. SSA has a relatively high participation rate, nearly as high as the Middle East and North Africa (MENA) region in spite of being geographically further away from Europe.

Global value chain (GVC) participation by major geographic regions. Source: Authors calculation using GVC database from Borin and Mancini (2015, 2019). Note: See Annex A for full countries in regional groups. Points above 45° indicate an increase in GVC participation.

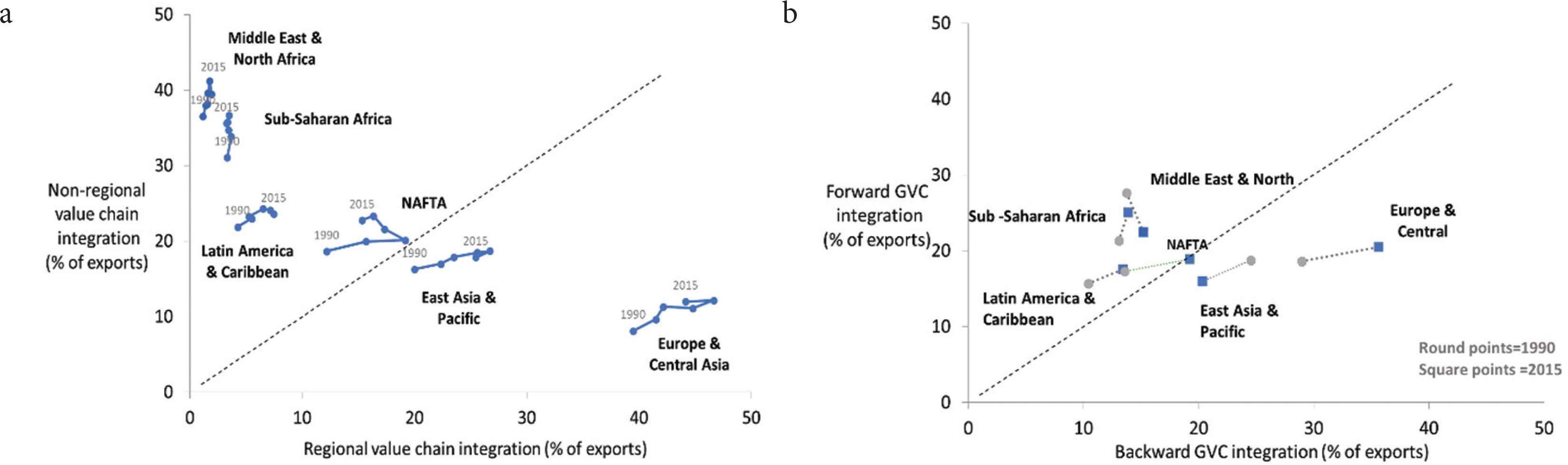

Because of transaction costs associated with border crossings along with other geopolitical and economic factors, GVCs usually develop along geographically proximate production chains, and often these value chains are regional. We take a look at RVC participation by region between 1990 and 2015. East Asia and Europe and Central Asia emerge as two regions with strong RVCs. Following a first period of RVC growth, North America has shifted toward linkages outside of its region with strong connections to China and East Asia productions chains (Figure 3a).

Decomposition of global value chain (GVC) participation by major geographic regions (a) and by type (b). Source: Authors calculations using GVC database from Borin and Mancini (2015, 2019). Breakdown of regional and non-regional value chain participation provided by Borin and Mancini using a novel extension of dataset available on request. Note: Points above the 45° indicate an increase in GVC participation.

We observe three distinct patterns of supply chain trade in Figure 3a. First is the very low growth of regional supply chain trade for SSA and MENA. Second is the divergent experience between MENA and SSA compared to other regions: most GVC trade is non-regional, that is, it takes place outside of the defined regional blocs. These patterns may reflect a weak governance and regulatory environment that hamper the development of RVCs (North America displays a pattern in which supply chain trade developed around NAFTA during the 1990s, then a switch starting about 2000 toward non-regional supply chains). Third is the strong focus on RVCs for East Asia and Pacific and Europe and Central Asia, both already emerging hubs in the 1990s.

This shift toward regional supply chains—dubbed the “Asia factory” by Baldwin and Forslid (2014)—reflects several forces at work. First is strong agglomeration economies (external economies and the development of specific skills in the workforce). Second is widespread trade facilitation policies, characterized by Vezina (2014) as a “race-to-the bottom” tariff cutting in the region to attract Japanese FDI. Other trade facilitation measures include simple and transparent rules of origin to facilitate cross-border trade in the region (Cadot et al., 2007). Third is the importance of strong institutions, as was the case for the Asia and Pacific region. Dollar and Kidder (2017) show in a cross section that much of the uneven participation in GVCs across countries and regions is related to indicators of the quality of institutions at the national level.6

In 2015, only 3.5% of total SSA exports were connected to supply chain trade within the SSA region. This stands in contrast to the 25.5% RVC integration for East Asia and the Pacific—almost eight times the integration of SSA. By contrast, SSA is more integrated into non-regional GVCs (35.6% of exports in 2015) than all regions except MENA. Europe and Central Asia is the most integrated region into RVCs followed by East Asia and the Pacific.

Figure 3b measures whether participation in supply chains is mostly backward (high shares of imported intermediates in gross exports) or downstream (mostly selling intermediates for further processing). Two stylized patterns emerge. East Asia and Pacific and Europe and Central Asia moved toward greater intraregional trade in parts and components where, in the language of Baldwin and Forslid (2014), the “factory economies” were both makers and buyers of components and parts. For this to be possible, intraregional trade must not be interrupted along the production chain. The downstream pattern is one in which exports are intermediates destined for further processing outside the region, thereby obviating having to rely on a smooth coordination across regional partners.

Of all the geographic regions, in 2015, SSA had the highest forward GVC participation rate of about 25% of total exports, a share that has grown by about 4% points since 1990. SSA’s forward GVC participation rate is higher than that of East Asia and the Pacific (18.8%) and Europe and Central Asia (20.5%) (Figure 3b). By contrast, the backward GVC participation rate for SSA has grown by less than 1% point since 1990 and stands at about half the share of its forward GVC participation (Figure 3b). A large share of SSA’s GVC integration consists of forward GVC integration: a relatively larger share of SSA’s GVC exports is used by the importing countries to produce final goods for export. This is to be expected as SSA countries are heavily reliant on the export of raw materials—40% of exports in 2018 (AEO, 2018); these raw materials are exported to other countries for the production of higher value-added final goods.

3. A CLOSER LOOK AT SUPPLY CHAINS ACROSS AFRICAN RECs AND BY STRATEGIC SECTORS

Much of past regional integration in Africa took place around the eight RECs recognized by the Africa Union. These RECs have been important engines of trade for the continent and will continue to be important even as African countries move toward more continental integration. Thus, it would be useful to understand how GVC participation has evolved across these different RECs, against the backdrop of differences in economic and policy contexts. We are unaware of any studies that attempt to present systematic comparisons of GVC participation across the different African RECs using Borin and Mancini (2019) data.

In the following section, we start with descriptive measures of overall GVC participation across four main African RECs (ECOWAS, SADC, COMESA, and the EAC), two comparator FTAs (ASEAN and MERCOSUR) and two major trade-dependent economies: China and India.

3.1. Overall GVC Participation, RVC, and Non-RVC Participation for RECs

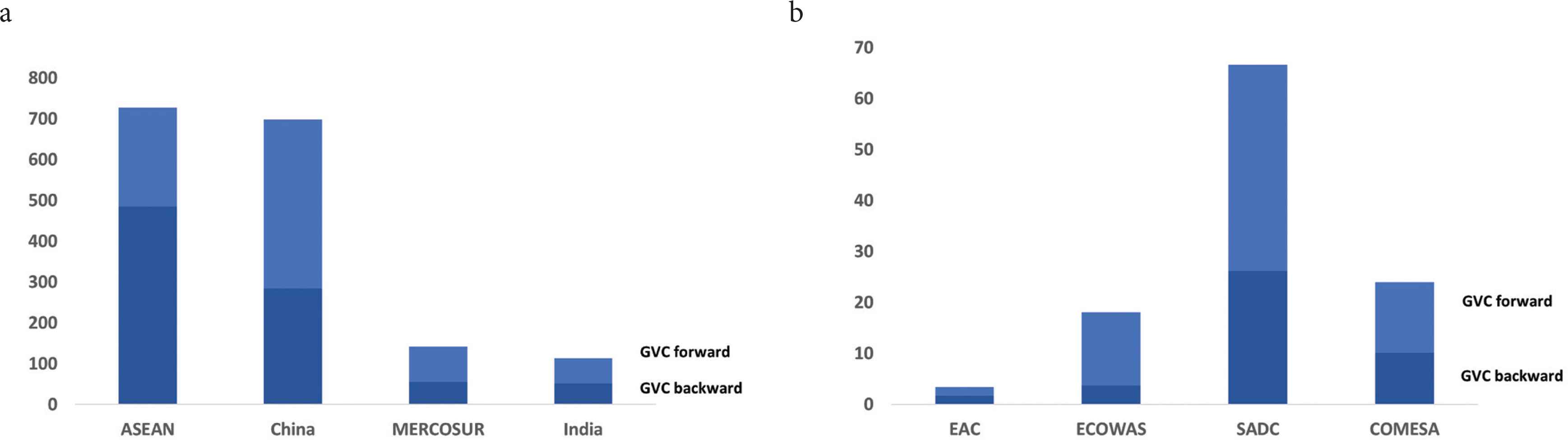

A broad look at GVC-related trade volumes shows that ASEAN and China have about 10 times more GVC-related trade than their closest comparators, India and MERCOSUR. The share of backward GVC related trade is much larger in ASEAN than in China. Among African RECs, only SADC is comparable to MERCOSUR in terms of the volume of GVC-related gross exports, probably reflecting the presence of a large economy in each trading bloc: Brazil in MERCOSUR and South Africa in SADC. Among the four major African RECs, SADC has the highest volume of GVC related exports with the EAC’s GVC trade amounting to about around US$3.5 billion in 2015 (Figure 4).

Global value chain (GVC)-related trade volumes for African Regional Economic Communities (RECs) and comparators, 2015 (US$ billions). (a) Comparators and (b) African RECs. Source: authors’ calculations using GVC database from Borin and Mancini (2015, 2019).

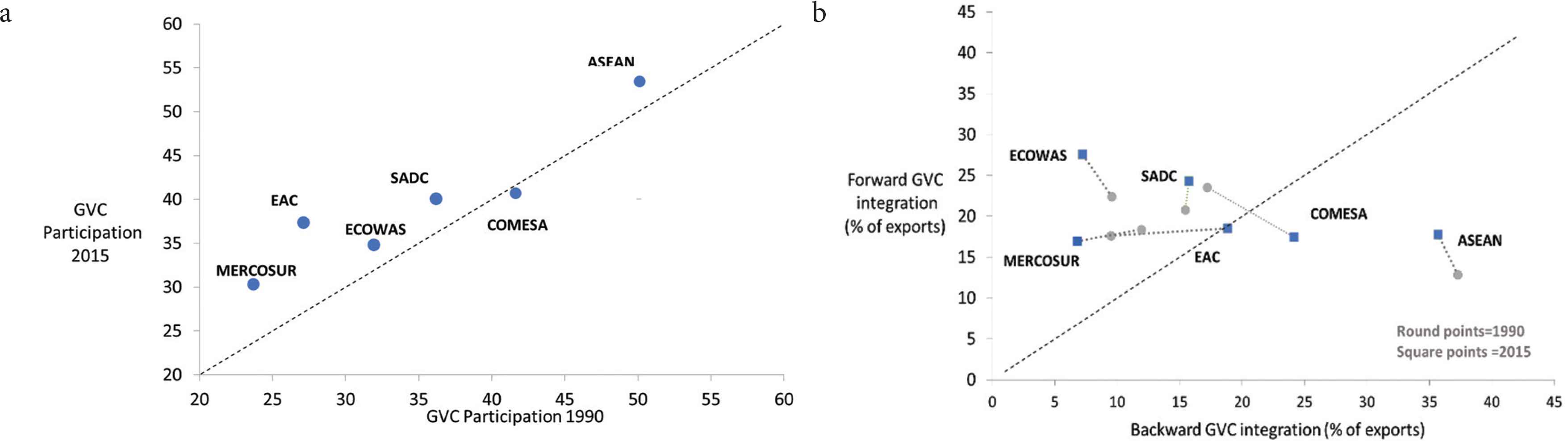

To compare GVC-related trade across RECs of different size, GVC trade should be expressed as a share of each country’s gross exports (i.e., GVC participation measure) to detect whether, as expected, smaller economies participate more intensely in fragmentation of production. In Figure 5a, we see that all four African RECs, despite having lower values of GVC-related trade than MERCOSUR, have more intensity in GVC participation.

Global value chain (GVC) participation for African Regional Economic Communities (RECs) and comparators. (a) GVC participation rate, 1990 and 2015. (b) Backward and forward GVC participation rate, 1990 and 2015. Source: Authors’ calculations using GVC database from Borin and Mancini (2015, 2019)

At the world level, both backward and forward measures of GVC participation increased over the period 1990–2005 then stabilized from 2005 until 2015 (Section 2 in the Online Supplementary file). This trend is a product of two major events: the growth of automation and robotics and the economic crisis of 2009. For African RECs, trends in backward integration have followed world trends, but they have remained about a third below those for other regions and at half the rate for ASEAN—“factory Asia”—whereas forward integration shares have been above average, confirming that Africa continues to export goods toward the top of supply chains.

Figure 5b shows the breakdown of GVC participation rates by forward and backward GVC participation for two periods: 1990 and 2015. We see, for example, that the EAC’s growth in GVC participation is moving toward greater backwardness. By 2015, the contribution of backward and forward participation to GVC participation for the EAC was about the same. This shift toward greater backwardness is compatible with the REC’s relatively open trade regime with the current three-band Common External Tariff (CET) structure does not protect activities producing intermediates sufficiently. However, the shift toward a four-band tariff structure could halt this progression. As expected, ASEAN’s backward GVC participation is much higher than that observed for all the other RECs, a reflection of “factory Asia.”

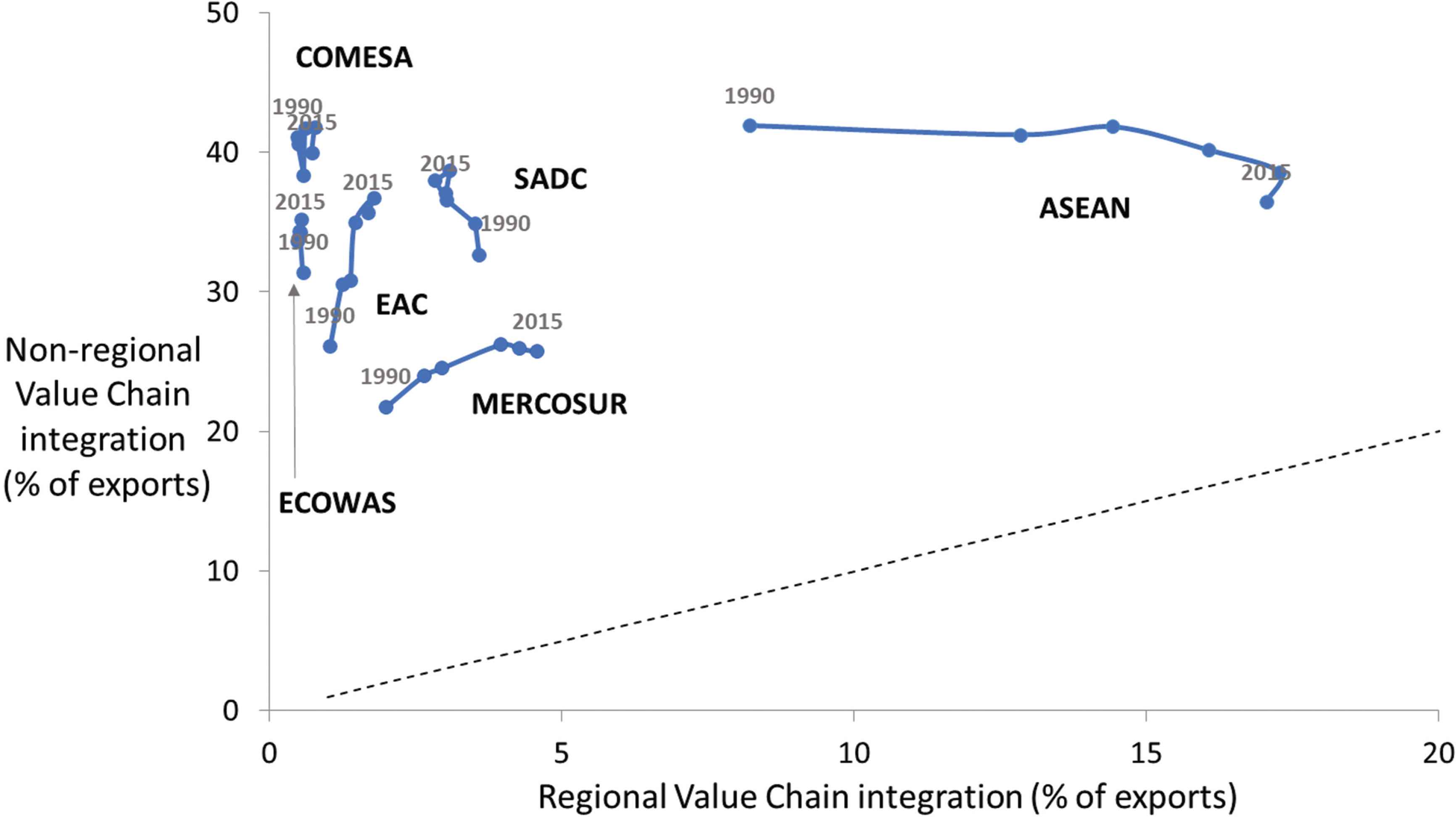

Although GVC trade has increased across FTAs and RECs, we do not observe a similar trend in RVC trade. Figure 6 shows a decomposition of GVC integration by regional and non-regional GVC integration as defined by the geographic definition of the RECs (see Annex). Two patterns stand out. First, African RECs and comparators engage more intensely in non-regional GVC trade than they do in RVC trade (all point above the 45° line for all RTAs). Second, the comparators—MERCOSUR and ASEAN—have had a stronger move toward RVC supply chain trade than African RECs. Indeed, there is a striking absence of RVC growth for all African RECs with RVC participation rates of between 0.5% and 3.2%. Calibrated estimates of bilateral trade costs show that these are substantially higher in SSA than in other regions, and that these costs have not fallen as rapidly as in other regions (de Melo et al., 2020). High bilateral trade costs could be an important contributing factor to the lack of development of RVCs in SSA.

Regional versus non-regional participation in supply chain trade: African Regional Economic Communities (RECs) and comparators. Source: Authors calculations using global value chain (GVC) database from Borin and Mancini (2015, 2019). Note: For each region and for intervals of 5–6 years between 1990 and 2015, the figure plots the share of GVC trade in total GVC trade involving only production partners in the same region (regional GVC integration) against the share of GVC trade involving only partner countries outside the region in total GVC trade (non-regional GVC integration). Regional and non-regional GVC participation measures are computed as weighted averages over the countries in each group. The weights are the share of each country in the corresponding region total trade. Points above the 45° indicate an intensity in non-regional value chains.

3.2. Sectoral GVC Performance at the REC Level

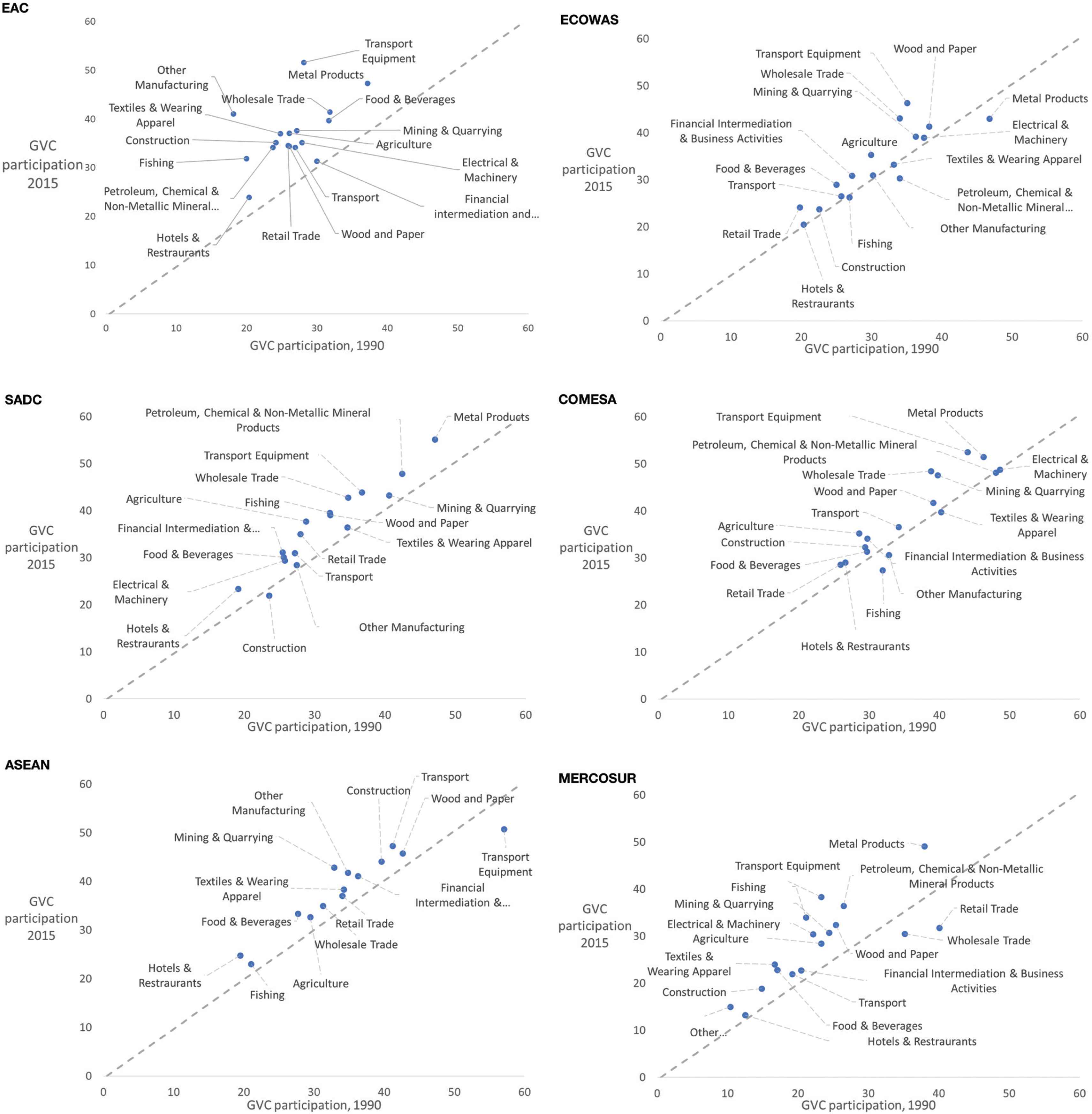

The World Bank’s World Development Report 2020 report finds that a significant share of growth in global GVC participation occurred in select sectors: machinery, electronics, and transportation sectors driven by GVC participation in East Asia, North America, and Western Europe. On average, for the four African RECs, transport, agriculture, and wholesale trade have seen the largest change in GVC participation between 1990 and 2015. Figure 7 details the evolution of GVC participation across 17 sectors spanning agriculture, industry, and services, one of each REC and the two comparators, ASEAN and MERCOSUR.

Global value chain (GVC) participation by Regional Economic Communities (RECs).

Among the four RECs, EAC has registered the largest growth in GVC participation over the period. For about half of the sectors, GVC participation is clustered around a GVC participation between 30% and 40%. Food and beverages, metal products, transport equipment, and wholesale trade are among the most GVC intense sectors, whereas fishing, hotel, and financial services sit below the cluster of sectors (Figure 7).

Unlike the EAC, sectoral GVC participation in ECOWAS is fairly spread out with less of an increase for the period 1990–2015. In fact, fishing, metal products, and petroleum have seen a decrease in GVC participation rates (although GVC participation in metal products remains high). This might be indicative of a growth in domestic processing and consumption; however, it could also be a result of a decline in the exports of these products. Wood and paper, transport, and wholesale trade have relatively higher GVC participation rates, whereas food and beverages, construction, and hotel services lag behind.

For SADC, all sectors except construction have seen an increase in GVC participation. Notably, metal products are estimated to have a GVC participation rate of more than 50% indicating a strong integration into regional and international GVCs. At the opposite end of the spectrum is food and beverages, with slightly less than 30% GVC participation.

Finally, the textile and fishing sectors for COMESA have not seen much improvement since 1990 together with electrical machinery and petroleum. All other sectors have increased their GVC participation led by metal products and transport equipment.

4. CORRELATES OF GVC PARTICIPATION RATES FOR AFRICAN COUNTRIES

Participation in GVC trade (backward and forward participation) has been associated with nonpolicy and policy factors (OECD, 2013, 2015; Del Prete et al., 2019; World Bank, 2018, 2020). Identified nonpolicy factors include market size, level of development, location (proximity to hubs in Europe, North America, Asia), manufacturing share in gross domestic product (GDP; a high share of manufacturing is associated with strong high backward engagement and low forward engagement), logistics, and trade facilitation. The FDI stock, dependent on past trade policies, is also strongly associated with supply chain trade.

Here we report correlations of policy and nonpolicy variables for the three measures of GVC participation: total GVC participation, backward, and forward after controlling for nonpolicy factors. The same specification is used for the three indicators of GVCs. Because of missing variables over the early period (no estimates of trade costs before 1995), we report estimates for the period 1995–2015. After cleaning, our sample includes 146 countries with a population exceeding 1 million in year 2015.7 Estimates from the double log specification produce elasticity estimates. To represent a period representative of an equilibrium, we take 3-year averages over the sample as recommended by Baier and Bergstrand (2007). Taking the overall GVC-related share as an example, we use the equation shown below:

The variables are (see Annex for data source):

- •

GVCsit, GVC-related trade share from Equation (A1) in Section 1 of the supplementary file

- •

GVCbsit, GVC backward [Equation (A2) in Section 1 of the supplementary file] as a share of gross exports

- •

GVCfsit, GVC forward (Equation A3 in Section 1 of the supplementary file) as a share of gross exports

- •

GDP_pcit, GDP per capita (source: WDI indicators)

- •

MANSHRit, manufacturing share in GDP (source: WDI)

- •

FDI_pcit, FDI stock per capita (source: UNCTADStat)8

- •

TRCOSTit, calibrated trade costs (source: Arvis et al., 2016)9

- •

tarZMit, tariffs on imports and exports of intermediates [source: World Bank World Integrated Solution (WITS)]

- •

MOBSit, number of mobile phone subscribers per 100 inhabitants (source: International Telecommunication Union)

- •

ωi country fixed effect that controls for time-invariant omitted variables

- •

μt time fixed effect controlling for time-related common shocks

The first three regressors capture the time-varying nonpolicy variable and the second three, the policy variables. For the nonpolicy variables, GDP_pcit is the proxy for market size with expected positive coefficient. MANSHRit is expected to carry a positive sign for the backward indicator, but negative for the forward share and the FDI_pcit coefficient is expected to be positive, especially for GVCs.10

The next three variables are proxies to detect the effects of policy variables. Low tariffs, both at home and faced in export markets, should facilitate backward and forward GVC engagement by allowing firms access to cheaper intermediate inputs and capital goods. The fixed effects ωi allows for country-specific intercept and μi controls for common shocks across countries. The identifying restriction is that there are no country-specific time-invariant omitted variables.

Tariff data are taken from the WITS database with tariffs defined as the effectively applied trade weighted tariffs. To keep the focus on supply chain trade, we focus on tariffs on imports and exports of intermediates captured by tarZMit (we also considered tariffs on capital and consumer goods but omitted them because of high correlation with the tariff variable on intermediates). TRCOSTit is the proxy indicator for trade facilitation, available yearly. It includes all factors accounting for differences between the fob and the average of CIF (cost, insurance, freight) prices of partners, and is expected to have a negative sign. Finally, MOBSit captures the ease of offshoring, expected to carry a positive coefficient for backward integration.

The resulting correlations are for an unbalanced sample with about half of nonzero observation (a full sample would include 1184 observations for all countries and 174 for African countries). Because we are only looking to validate a potential role for the policy variables (see full discussion paper), we report cross-sectional ordinary least squares (OLS) estimates with year and country fixed effects after tests for model choice favor a fixed-effects estimation (see Section 3 in Online Supplementary file). Because of the presence of confounding factors in this cross-country setting, the correlations displayed in Tables 1 and 2 are associations that do not identify causal effects.11

| All countries | African countries | |||||||

|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| GVC participation (log) | GVC participation (log) | |||||||

| GDP per capita (log) | −0.00513 [0.033] | −0.0214 [0.034] | −0.0418 [0.033] | −0.0482 [0.036] | 0.157*** [0.051] | 0.124** [0.048] | 0.146** [0.055] | 0.0711 [0.061] |

| Manufacturing share in GDP (log) | 0.0654 [0.052] | 0.0518 [0.049] | −0.0123 [0.050] | −0.0199 [0.051] | 0.0613 [0.054] | 0.127** [0.054] | 0.123 [0.075] | 0.119* [0.065] |

| FDI stock per capita (log) | 0.0825*** [0.025] | 0.0544** [0.026] | 0.0444* [0.025] | 0.0408 [0.027] | −0.0725** [0.033] | −0.0665* [0.034] | −0.0576 [0.041] | −0.0599* [0.034] |

| Tariffs on imports intermediates (log) | −0.118*** [0.034] | −0.115*** [0.033] | −0.0984*** [0.033] | −0.00392 [0.049] | 0.0485 [0.062] | 0.0452 [0.050] | ||

| Calibrated trade costs (log) | −0.388*** [0.14] | −0.377*** [0.14] | 0.225 [0.30] | 0.518 [0.31] | ||||

| Number of mobile phone subscribers per 100 inhabitants (log) | 0.0318 [0.050] | 0.135* [0.068] | ||||||

| Constant | 0.0739 [0.81] | 0.166 [0.54] | 2.323** [1.00] | 2.029** [0.97] | −4.902*** [1.39] | −2.792*** [0.66] | −4.370** [1.86] | −5.485*** [1.71] |

| Number of observations | 648 | 565 | 542 | 479 | 174 | 146 | 143 | 131 |

| Adjusted R-squared | 0.400 | 0.412 | 0.453 | 0.443 | 0.391 | 0.353 | 0.279 | 0.415 |

| Country FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Standard errors in brackets.

p < 0.10,

p < 0.05,

p < 0.01.

Correlates of overall GVC participation rates: 1995–2015: full country sample and sample of African countries

| (1) | (2) | (3) | (4) | |||||

|---|---|---|---|---|---|---|---|---|

| Backward GVC participation (log) | Forward GVC participation (log) | Backward GVC participation (log) | Forward GVC participation (log) | Backward GVC participation (log) | Forward GVC participation (log) | Backward GVC participation (log) | Forward GVC participation (log) | |

| All countries | ||||||||

| GDP per capita (log) | −0.0890 [0.082] | 0.116** [0.047] | −0.117 [0.10] | 0.116** [0.054] | −0.310*** [0.076] | 0.122** [0.050] | −0.453*** [0.078] | 0.166*** [0.055] |

| Manufacturing share in GDP (log) | 0.316** [0.13] | −0.239*** [0.074] | 0.316** [0.15] | −0.195** [0.078] | 0.317*** [0.12] | −0.302*** [0.077] | 0.218** [0.11] | −0.272*** [0.076] |

| FDI stock per capita (log) | 0.235*** [0.063] | −0.106*** [0.036] | 0.172** [0.079] | −0.0890** [0.041] | 0.198*** [0.057] | −0.114*** [0.038] | 0.174*** [0.057] | −0.125*** [0.040] |

| Tariffs on imports intermediates (log) | – | – | −0.220** [0.10] | 0.0151 [0.053] | −0.388*** [0.076] | 0.0306 [0.051] | −0.295*** [0.071] | 0.00895 [0.050] |

| Calibrated trade costs (log) | – | – | – | – | −0.634* [0.33] | −0.462** [0.22] | −0.577* [0.30] | −0.433** [0.21] |

| Number of mobile phone subscribers per 100 inhabitants (log) | – | – | – | – | – | – | 0.408*** [0.11] | −0.0777 [0.074] |

| Constant | 9.455*** [2.01] | −5.199*** [1.15] | 1.524 [1.65] | −2.917*** [0.86] | 6.026** [2.31] | −0.124 [1.53] | 6.596*** [2.06] | −1.459 [1.45] |

| Number of observations | 648 | 648 | 565 | 565 | 542 | 542 | 479 | 479 |

| Adjusted R-squared | 0.495 | 0.183 | 0.297 | 0.079 | 0.681 | 0.235 | 0.728 | 0.252 |

| Country FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| (5) | (6) | (7) | (8) | |||||

| African countries | ||||||||

| GDP per capita (log) | 0.301 [0.20] | −0.0410 [0.12] | 0.0146 [0.17] | 0.0953 [0.077] | 0.0581 [0.19] | 0.0854 [0.093] | −0.121 [0.22] | 0.0792 [0.12] |

| Manufacturing share in GDP (log) | 0.249 [0.21] | −0.0744 [0.13] | 0.401* [0.19] | −0.0526 [0.085] | 0.458 [0.27] | −0.0670 [0.13] | 0.387 [0.24] | −0.0329 [0.12] |

| FDI stock per capita (log) | −0.0851 [0.13] | −0.0344 [0.079] | 0.00759 [0.12] | −0.0717 [0.054] | −0.00129 [0.14] | −0.0497 [0.069] | −0.0489 [0.12] | −0.0403 [0.064] |

| Tariffs on imports intermediates (log) | – | – | −0.371* [0.18] | 0.345*** [0.078] | −0.347 [0.22] | 0.367*** [0.10] | −0.355* [0.18] | 0.352*** [0.096] |

| Calibrated trade costs (log) | – | – | – | – | 0.215 [1.06] | 0.187 [0.51] | 0.970 [1.12] | 0.192 [0.58] |

| Number of mobile phone subscribers per 100 inhabitants (log) | – | – | – | – | – | – | 0.401 [0.25] | −0.00928 [0.13] |

| Constant | −5.887 [5.45] | −3.215 [3.32] | −3.003 [2.36] | −3.522*** [1.04] | −4.880 [6.57] | −4.446 [3.15] | −7.284 [6.22] | −4.578 [3.25] |

| Number of observations | 174 | 174 | 146 | 146 | 143 | 143 | 131 | 131 |

| Adjusted R-squared | 0.215 | −0.029 | 0.288 | 0.518 | 0.225 | 0.383 | 0.361 | 0.389 |

| Country FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

Standard errors in brackets.

p < 0.10,

p < 0.05,

p < 0.01.

Correlates of backward and forward GVC participation rates: 1995–2015: full country sample and sample of African countries

Table 1 reports regressions for the overall GVC measure. Results in columns 1–4 are for the sample of all countries and estimates for the sample of African countries are reported in columns 5–8. Looking at our sample of all countries and our three “nonpolicy” variables, FDI is the only variable that has expected positive effect on participation for overall GVC participation. Turning to the policy variables, except for the mobile subscription indicator, MOBSit, the estimated coefficients have the expected sign and are stable across specifications: a higher tariff on imports and exports of intermediates, tarZMit, is a brake on GVC participation, usually significant at the 1% level. Higher trade costs, TRCOSTit, also acts as a break on GVC participation.

Restricting estimation to the sample of African countries, we find positive and significant results for the correlation between GDP in columns 5–7, but it turns insignificant after controlling for the number of mobile phone subscribers per 100 inhabitants (column 8). With the full specification in column 8, GVC participation is positively correlated with the manufacturing share in GDP and the mobile subscription indicator. No significance is detected for the indicators on tariffs and trade costs. We also observe a negative correlation between GVC participation and the FDI stock per capita; for the sample of all countries this coefficient was insignificant.

Table 2 reports on the same correlates for the two samples, but this time for backward and forward measures of GVC participation. For the backward integration correlations for the full sample in columns 1–4, as expected, the coefficient for tariffs on intermediates displays consistently a negative sign. Mobile subscription is positively and significantly associated with backward integration supporting the importance of Information and Communication Technology (ICT) for production unbundling.12 Notably, the coefficient is insignificant for the forward integration measure. For the forward integration correlations, the FDI coefficient is unstable and the tariff coefficient loses significance. This is not surprising for developing countries that engage mostly in the downstream part of supply chains where they export mostly raw materials. High trade costs are associated with low participation in forward GVC participation. Not surprisingly, regarding the results for the African sample reported in columns 5–8, correlations are insignificant except for the tariff variable.

We run several robustness checks against the findings of our main regression specification. Section 4 of the online supplementary file reports the results and outlines these robustness checks. We estimate regressions using two 10-year periods between 1995 and 2015. The results are largely the same with stronger significance in the earlier periods for our policy and nonpolicy variables of interest (2006–2015). Adding the services sector share in GDP (strongly correlated with the manufacturing share) does not alter the pattern of results. As in the main text, specifications restricted to the African sample are not significant (see Tables A6 and A7).

We also compared results under balanced and unbalanced data panels. Tables A6 and A7 report results for: (1) a specification that includes services share in GDP as a dependent variable; (2) for specifications using yearly variable estimates versus 3-year averages; (3) for an African only sample using balanced and unbalanced datasets. Findings for all these specification do not point to any significant changes for the results above.

5. CONCLUSION

Reductions in transport and communication costs along with policy measures to facilitate trade have resulted in the fragmentation of production across countries and the growth of connection between firms. This means that African countries can now participate in supply chain trade both “upstream” (importing components/intermediates embodied in exports) and “downstream” (selling components/intermediates that enter into further processing before reaching the consumer). African countries no longer have to develop whole industries from scratch to industrialize.

Indeed, the African Union’s Action plan on boosting intra-African trade, launched in 2013 and the recently launched AfCFTA in May 2019, speaks to the desire of African countries to integrate into supply chain trade using deeper regional integration as a stepping stone. A key objective of the AfCFTA is to develop RVCs at the level of the RECs and also across the communities directly at the continental level.

This paper provides detailed comparisons of GVC and RVC measures over the period 1990–2015 at the aggregate and sector levels at regional and country levels, with comparisons focused on African RECs and two comparator groups, ASEAN and MERCOSUR. In sharp contrast with other RTAs, all growth in supply chain trade for African RECs was at the non-regional level, whereas for East Asia and Pacific and Europe and Central Asia—already emerging hubs in the 1990s—growth was mostly focused along RVCs. This pattern of strong RVC growth, absent across African RECs, reflects several forces at work in other regions World Bank (2020). First are strong agglomeration economies (external economies and the development of specific skills in the work force) boosted by the fall in communication costs in already large markets. Second are widespread trade facilitation policies to attract FDI. Third is the importance of institutions that have high indicator values in those regions.

The decompositions of GVC integration by regional and non-regional GVC components across African RECs uncovered three patterns. First, for all RTAs (SADC, ECOWAS, EAC, COMESA, MERCOSUR, and ASEAN) non-regional GVC dominates RVC. Second, among African RECs, the EAC is second to SADC in RVC integration. However, for both SADC (3% of gross exports) and the EAC (1.7% of gross exports), RVC participation rates are much lower than that of ASEAN (around 17.2% of gross exports). Indeed, non-African trading blocs, MERCOSUR and ASEAN, have significantly increased RVC participation from 1990–2015.

Overall, the estimates in this paper show that there is room to increase overall GVC participation as well as RVC participation across the African continent. Discussion in the paper supplemented by regressions show that the following variables are critical policy levers: (1) tariffs on imports of intermediates; (2) rules of origin as captured by trade costs; and (3) digital connectivity and trade in services.

Fragmentation of production across Africa requires seamless borders. We expand on three obstacles to the development of RVCs, all of which are amenable to policy reform. First is the tariff structure. Second, the barriers to trade in services often embodied in goods trade should be reduced. Third is the simplification of rules of origin. Importantly, as noted by many (see, e.g., Mafurutu, 2020), Electronic Certificates of Origin (e-CoO) are starting to be implemented in SADC and COMESA. If properly implemented, e-CoO will facilitate the movement of essential cargo; it may also serve to reduce the chances of transmission communicable diseases such as COVID-19 through human interface at ports of entry.

CONFLICTS OF INTEREST

The authors declare they have no conflicts of interest.

AUTHORS’ CONTRIBUTION

The authors contributed equally to the article.

ACKNOWLEDGMENTS

We thank Ana Fernandes and Melise Jaud for sharing their classification of GVC participation and Alessandro Borin and Michele Mancini for sharing their methodology and data used to measure value chains. We also thank Hubert Escaith, Richard Newfarmer, Ben Shepherd, Victor Steenbergen two JAT referees and the JAT editors, Augustin Fosu and Andrew Mold for helpful comments. Finally, de Melo thanks the French National Research Agency under program ANR-10-LABX-14-01ANR for additional support. The data that support the findings of this study are available from the corresponding author upon reasonable request. Any views are those of the authors and not those of their respective affiliations.

SUPPLEMENTARY MATERIALS

Supplementary data related to this article can be found at

ANNEX

A. Regional Groupings and Country Lists

Association of Southeast Asian Nations (ASEAN): Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, Vietnam.

Common Market for Eastern and Southern Africa (COMESA): Burundi, Comoros, Democratic Republic of Congo, Egypt, Eritrea, Ethiopia, Kenya, Libya, Madagascar, Malawi, Mauritius, Rwanda, Seychelles, Sudan, Swaziland, Uganda, Zambia, and Zimbabwe.

East African Community (EAC): Burundi, Kenya, Rwanda, Tanzania, Uganda.

Economic Community of West African States (ECOWAS): Benin, Burkina Faso, Cabo Verde, Cote d’Ivoire, Gambia, Ghana, Guinea, Guinea Bissau, Liberia, Mali, Niger, Nigeria, Senegal, Sierra Leone, and Togo.

Southern Common Market (MERCOSUR): Argentina, Brazil, Paraguay, Uruguay, Venezuela.

Southern African Development Community (SADC): Angola, Botswana, Democratic Republic of Congo, Lesotho, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Seychelles, South Africa, Swaziland, Tanzania, Zambia, and Zimbabwe.

Sample of African countries: Angola, Botswana, Burundi, Cameroon, Cabo Verde, Central African Republic, Chad, Cote d’Ivoire, Democratic Republic of Congo, Egypt, Gabon, Gambia, Ghana, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Morocco, Mozambique, Namibia, Niger, Nigeria, Rwanda, Senegal, Sierra Leone, Somalia, South Africa, Swaziland, Tanzania, Togo, Tunisia, Uganda, Zambia.

B. Data Sources

Data on measures of GVC participation come from a database developed by Borin and Mancini (2019). Data on FDI stock per capita are from UNCTAD Stats. GDP per capita, share of manufacturing, and services in GDP comes from the World Bank’s World Development Indicators database. Tariff data on raw materials, intermediates, consumer goods, and capital goods is from the World Bank’s WITS TRAINS database. Estimates of trade costs are from the World Bank’s ESCAP database. Our proxy for digital connectivity—number of mobile phone subscriptions per 100 inhabitants—is from the International Telecommunication Union.

Footnotes

Negotiations are currently ongoing to decide on the rate for the new fourth band under the EAC Common External Tariff system.

Borin and Mancini (2019) “extend the set of possible measures, including a new indicator of GVC-related trade, in order to address a wider range of empirical issues.” The major issue being double-counting of export flows. They also improve on existing GVC measures from previous research.

Melo and Twum (2020) presents the length of the production chain, a measure of the distance from any production stage to final demand (see Figure 1 in the discussion paper for an evolution of complex GVC participation over the period).

Despite its coverage the EORA database can be unreliable for some countries. Annex A2 discusses criteria used to exclude countries from the analysis because of data quality issues in EORA.

Examples include Johnson and Noguera (2012), Wang et al. (2017), Koopman et al. (2014), Borin and Mancini (2015), Los et al. (2016), Nagengast and Stehrer (2016), Johnson (2018), Ye (2018), Los and Timmer (2018), and WDR (2020).

Dollar and Kidder (2017) and WDR (2020) also report evidence from firm-level data. Patterns of revealed comparative advantage in manufacturing for contract-intensive activities have also been shown to be closely related to the quality of domestic institutions. de Melo and Olarreaga (2020) also survey the role of institutions in international trade.

The EORA sample includes 189 countries. Annex A11 of the discussion paper explains the criteria used to reduce the sample to 146 countries.

UNCTAD defines FDI stock as the “value of capital and reserves attributable to a non-resident parent enterprise, plus the net indebtedness of foreign affiliates to parent enterprises” (UNCTAD, 2019).

Computed as the GDP-weighted average of bilateral trade costs from the data in Arvis et al. (2016).

A report by the OECD, found that FDI can increase GVC participation by more than 20% points for some economies meaning increases in FDI could plausibly result in higher Foreign Value-added (FVA) and Indirect Value-added (DVX) values or both.

Similar cross-section estimates are reported in WDR (2020, Box 2.2).

Baldwin and Forslid (2014) develop a tasks, occupations, stages, product framework to show how ICT improvements, here coarsely captured by mobile subscriptions, fosters production unbundling here captured by a positive association of mobile subscriptions with backward integration. The discussion paper version discusses at greater length the importance of ICT in the case of the EAC.

This paper is a revised version of Melo and Twum (2020), which focused on the East African Community and discussed three supportive policies: reducing tariffs on intermediate goods, adopting liberal rules of origin, and policies for greater connectivity. Annex tables and figures mentioned in the text are available online as Supplementary material.

REFERENCES

Cite this article

TY - JOUR AU - Jaime de Melo AU - Anna Twum PY - 2021 DA - 2021/01/25 TI - Prospects and Challenges for Supply Chain Trade under the Africa Continental Free Trade Area☆ JO - Journal of African Trade SP - 49 EP - 61 VL - 8 IS - 2 (Special Issue) SN - 2214-8523 UR - https://doi.org/10.2991/jat.k.210105.001 DO - 10.2991/jat.k.210105.001 ID - deMelo2021 ER -